Let’s say we want to quit working and attain financial freedom—not in decades, but in just a few years. Or heck, maybe less. How do we do it?

One “must-have” is the need to clock out on dividends alone. It’s the only way to retire without being forced to sell stocks into a downturn, shriveling our wealth and income at the same time.

To hit our “dividends-only” retirement goal, then, we’d need a minimum yield of 8% on our $500K. That way we’re assured of banking at least $40,000 in dividends a year. But with inflation still “sticky,” we’d ideally like to do better—pulling in around $50,000 or more.

Sounds like a tall order, I know. But there are plenty of assets out there that could get us there. Here are three to consider.

High-Yield Investment No. 1: A 10% Payer With Strong Dividend (and Price) Upside

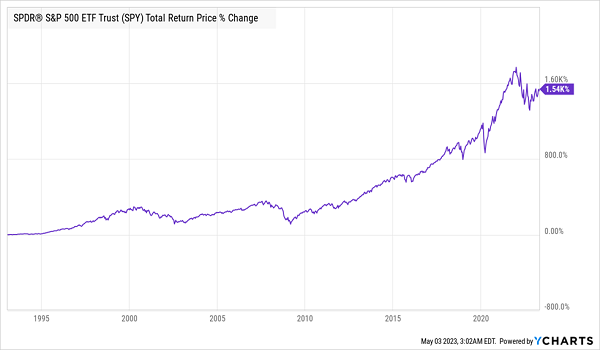

The best place to start is with a base of large-cap American stocks, simply because they’re unbeaten for building long-term wealth. Over the last 30 years, for example, the S&P 500 has posted a 9.7% compounded annualized growth rate (CAGR).

US Stocks Deliver for Decades

In other words, if you’d put $100,000 in stocks 30 years ago, you’d have north of $1.6 million today.

USA! USA!

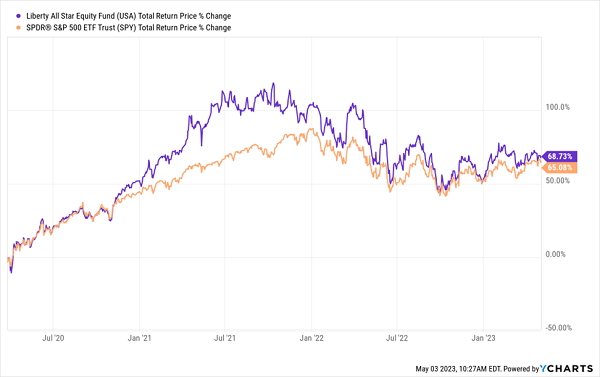

Trouble is, the typical S&P 500 stock yields just 1.7%, so we’d need to invest $3 million to get our $50,000 in yearly income.

Not so when we invest in big-name US stocks through a closed-end fund (CEF) called the Liberty All-Star Equity Fund (USA), payer of a 10% dividend. As you can see above, USA has returned 69% in the three-plus years since the depths of the COVID crash (as tough a proving ground as we’re likely to get), topping the market in the process. Moreover, thanks to its big dividend, USA has delivered most of its return in cash.

Let’s talk more about that payout:

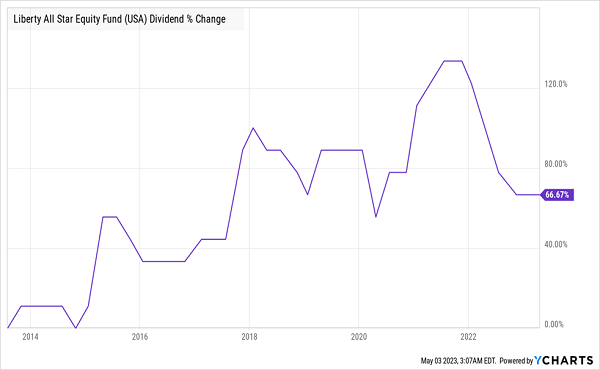

Big Income Stream Gets Bigger

USA has a unique dividend policy under which it will pay 10% of its net asset value (NAV) per year as dividends, in four installments of 2.5% each. That makes the payout less predictable but also gives management flexibility to buy oversold bargains when it spots them. And given that stocks are still well off their late-2021 highs, USA’s payout and portfolio have lots of upside.

Finally, because it’s a CEF, USA can, and often does, trade at a discount to NAV, and right now we can buy for around par—not bad considering that USA has traded at a premium for much of the past year, including a high 9.5% premium last summer.

High-Yield Investment No. 2: A 14.6% Yielder That Invests in Tech the Smart Way

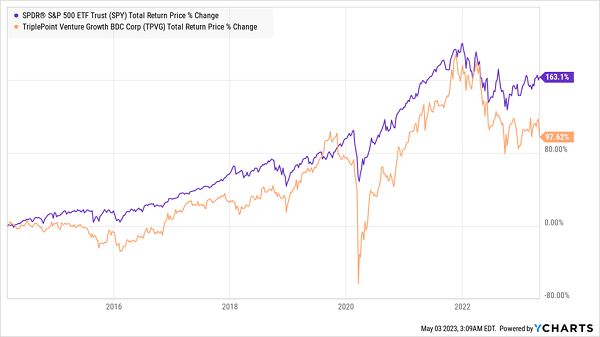

Our next option, the 14.6%-yielding TriplePoint Venture Growth BDC Corporation (TPVG), might cause you to do a bit of a double-take at first. It’s a bank that loans money to tech firms. But this one doesn’t accept deposits, so it’s not vulnerable to a Silicon Valley Bank–style bank run. It also focuses on lending to high-growth, profitable, mature private tech companies.

TPVG Lags the Market, Signaling Our Buying Opportunity

For a long time, TPVG’s returns, as you can see above, trailed the market but regularly bounced up to beat it. And thanks to the 2022 crash and the fact that TPVG has been unfairly swept up in the current banking paranoia, we’ve got another dip to buy now. The capper? This business development corporation (BDC) trades at a 7.7% discount to NAV.

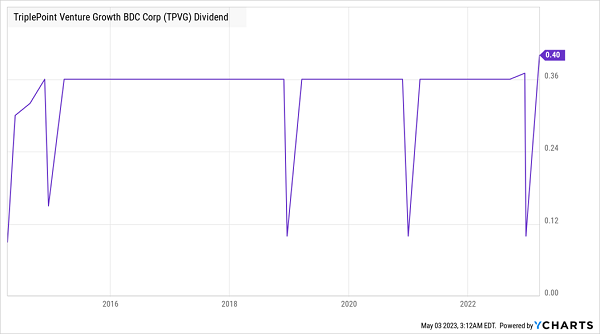

Moreover, TPVG has continued to maintain its dividend-coverage ratio while avoiding significant defaults from creditors. Hence, the firm’s dividend—right in the midst of a banking panic—actually went up (ignore the dips in the chart; they are special dividends on top of the huge regular payout).

TPVG’s Big Payout Rises, Despite Headwinds

How is this possible? Part of the answer is that higher interest rates are boosting the amount of money TPVG is making on its loans. It’s also seeing less competition from other Silicon Valley investors as the sector gets shaken out. Finally, TPVG has avoided tech-sector quagmires, such as crypto. All of this has fueled the BDC’s growth.

High-Yield Investment No. 3: A Low-Volatility Bond Fund With a 6.9% Payout

The BlackRock Taxable Municipal Bond Trust (BBN) holds hundreds of municipal bonds (which are issued by state and local governments to fund infrastructure projects) from across America. Thanks to their government backing, “munis” boast a default rate of less than 0.1%—meaning the risk to BBN’s cash flow is basically nil.

The payout does fluctuate somewhat, though, due to BBN’s managed-distribution policy. As a result, it did cut payouts in 2018, 2019 and 2022. But that was due to the low-interest rate period we were experiencing at that time. These days, higher rates are resulting in newly issued municipal bonds that pay much more than their older counterparts do.

That’s going to translate into higher investment income for BBN. This means its payout cuts are likely in the rear-view, and we’re looking at the prospect of dividend hikes instead. That makes now a good time to buy and “start off” with a 6.9% payout. Any hikes down the line would increase our “yield on cost” as we go.

One final note: unlike many muni-bond funds, BBN’s dividend is taxable. But its 6.9% payout, which is higher than the yields on most tax-free muni-bond funds, more than makes up for this.

A “3-Click” Dividend Portfolio Whose Payouts Match the Average Salary

Add BBN’s 6.9% yield to the payouts on USA and TPVG and you get a 10.5% average yield across these three picks. That means $52,500 in annual income on a $500,000 investment, which works out to $4,375 per month in income.

The average monthly wage in America is about $4,944 per month, so you’re a stone’s throw away from that with this portfolio—even closer when you consider that about $473 per month was spent on commuting in 2019 according to LendingTree, and the cost of getting to and from work would much higher now.

4 Incredible Income Plays Dropping 9%+ Dividends (With 20%+ GAINS Ahead, Too)

These 3 investments are a great start if you’re dipping a toe into the high-yield world. But my 4 favorite dividend payers are a better play—they’re a special group of funds that yield 9% on average and send their payouts your way every single month.

In fact, these 4 diversified income buys are so cheap I’m calling for 20%+ price upside from them in the next 12 months, to go along with their huge 9%+ payouts.

Click here to get the full story on these 4 incredible 9%+ monthly payers, along with a unique opportunity to download a FREE Special Report revealing their names, tickers, current yields and more.

Before you make your next trade, you'll want to hear this.

MarketBeat keeps track of Wall Street's top-rated and best performing research analysts and the stocks they recommend to their clients on a daily basis.

Our team has identified the five stocks that top analysts are quietly whispering to their clients to buy now before the broader market catches on... and none of the big name stocks were on the list.

They believe these five stocks are the five best companies for investors to buy now...

See The Five Stocks Here

Click the link below and we'll send you MarketBeat's list of seven best retirement stocks and why they should be in your portfolio.

Get This Free Report