Is it time to buy the dip on these dividends—which by the way yield between 5.3% and 7.6%?

Yes, the market-at-large has bounced quite a bit. But these payers remain mired in the bargain bin.

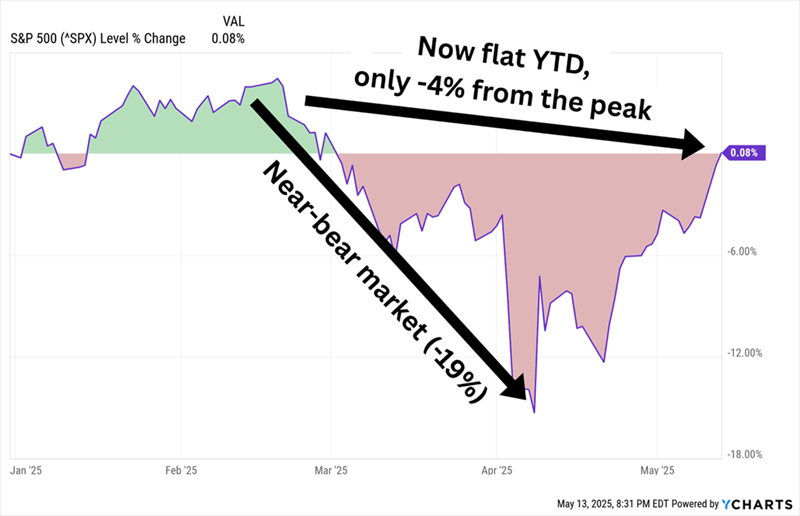

Vanilla investors who only focus on the S&P 500 have serious FOMO. They worry that they missed the pullback. The best buying opportunity, at least in terms of the plain “SPY” ETF owned by most of America, lasted only a week or two:

The S&P 500 Dip Didn’t Last Long

But there are still cheap dividend payers that haven’t rallied alongside the popular names. At least not yet. Let’s discuss five that yield 5.3% or more and are cheap with respect to the following two metrics:

- Price/earnings-to-growth (PEG): PEG measures earnings in relation to expected growth. In short, a PEG of 1 implies a stock is fairly valued. A number over 1 implies it’s overbought, and a number below 1 implies it’s oversold. Every stock I’m looking at has a PEG below 1.

- Forward price-to-cash flow (P/CF): This looks at how a stock is valued compared to its cash flows. Every stock I’m looking at has a forward P/CF that either ranks in the cheapest 20% of the S&P 500 (or would if the stock was in the S&P 500).

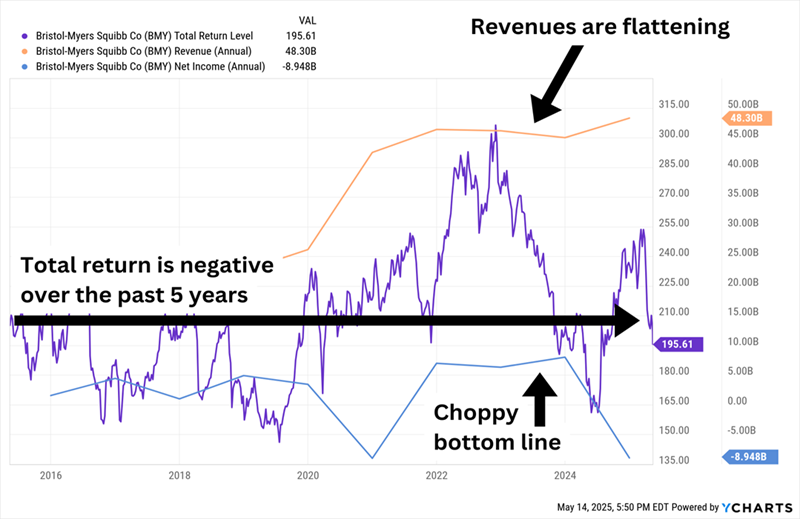

Bristol-Myers Squibb (BMY)

Dividend Yield: 5.6%

Bristol-Myers Squibb (BMY) is one of the more recognizable names in pharmaceuticals: a $90 billion blue chip responsible for blockbusters such as Revlimid and Opdivo (cancer) and Eliquis (anticoagulant). It trades at a screamingly low PEG of 0.12, and at just 7 times cash-flow estimates. It’s also punching above its already competitive weight class with a sturdy yield of 5%-plus.

BMY is cheap for a reason, though. The stock has basically treaded water over the past five years, though it certainly hasn’t done so in a straight line. It’s currently mired in a double-digit decline; yes, health care is generally weak this year, but Squibb is pulling up the rear.

Bristol-Myers Squibb has been mired in profitability concerns for years, sparked by competition eating away at several of its core drugs. A couple for-instances? Revlimid, once BMY’s top drug by sales and still responsible for high-single-digit revenues saw the top line hemorrhage by 44% during the first quarter. Abraxane sales were cut in half; Sprycel revenues dropped by a few points more than that. And generics are expected to further cut into its business over the next few years.

Yes, the Street is looking for a big snapback in profits for 2025, but that’s in large part because 2024 was dreadful. 2025 guidance, if hit, would be a 9% decline (at the midpoint) from its 2023 earnings.

BMY’s dividend is well funded, but its stock price outlook is a bit sketchy at the moment.

BMY: Big Pharma Name, Minor League Results

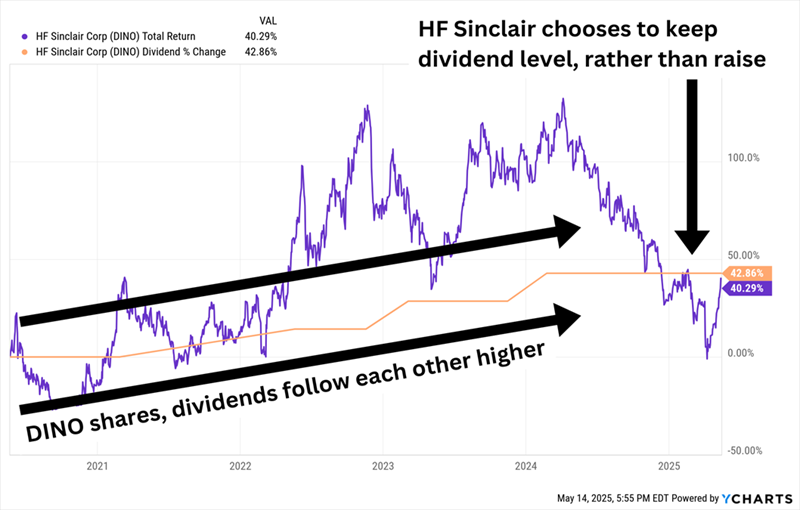

HF Sinclair (DINO)

Dividend Yield: 5.4%

HF Sinclair (DINO) is the product of a 2022 mash-up of HollyFrontier Corp., Holly Energy Partners, and Sinclair Oil. (The ticker name came from the latter’s iconic dinosaur logo.)

The company operates seven refineries in the U.S., as well as production facilities in Canada and the Netherlands. It boasts crude oil processing capacity of 678,000 barrels per day, lubricant production capacity of 34,000 barrels per day, and renewable diesel capacity of 380 million gallons per year. In addition to the HollyFrontier Specialty Products and Sinclair brands, it’s also responsible for Petro-Canada Lubricants, Sonneborn and Red Giant Oil.

DINO shares are fairly cheap on both a P/CF (7.3) and PEG (0.2) basis. We can thank a drop of more than 30% over the past year, even accounting for the stock’s rebound of the past month or so. There’s nothing novel about HF Sinclair’s troubles—they largely reflect weakness across the refining industry, which is the company’s largest segment. Trade policy uncertainty, tariffs, accelerating OPEC+ output, and expected weak global demand for gasoline, diesel, and jet fuel are all conspiring against refiners—conversely, any relief on any of those fronts should boost their fortunes.

Indeed, DINO has outpaced the energy sector and the market higher out of the April lows, up about 40% on a relief trade as the U.S. appears to be lifting its foot off the tariff pedal.

Margin anxiety nonetheless prompted HF Sinclair to pause what had been a budding streak of annual dividend hikes since a little before the corporate merger. As it stands, DINO’s 50-cent quarterly dividend implies it will pay $2 per share this year, but analysts only expect the company to earn $1.58 per share. The pain might be short-lived enough to survive, though, with dividend coverage expected to swell to 180% thanks to a big earnings jump in 2026.

Better Conditions for Refiners Could Revive DINO Dividend-Growth Hopes

AES Corp. (AES)

Dividend Yield: 5.6%

Virginia-based utility AES Corp. (AES) distributes power to some 2.7 million customers through its regulated utility businesses. But this isn’t just an ordinary local utility—it also boasts a renewables business that sells energy to corporate customers and data centers, with operations in 11 states coast to coast, as well as in South America, Europe, Asia, and the Middle East. As a result, it deals in a wide variety of energy, including coal, gas, hydro, wind, solar, and biomass.

AES shares’ low valuation—including a PEG of 0.8 and a forward P/CF of just 5—can largely be chalked up to an erosion in shares, with the stock losing more than half its value since the start of 2023. It has been hyper-aggressive in transitioning to renewables, but financially, that move hasn’t yet paid off, and investors have been further scared off by project delays and high debt.

The renewables business also means AES doesn’t act like a typical utility. While the yield is quite high for a utility, stability isn’t, with the stock trading less defensively and more in line with more cyclical plays.

There is good news here, however. AES has been attempting to cure some of its ails with large asset sales, cost cuts, and pushing back coal retirements, and that could give AES the footing it needs to start building a more consistent growth profile.

Also, the dividend looks mighty secure with plenty of room for continued payout upside, with expected earnings a little more than 3x what AES needs to fund the distribution.

The Dividend Magnet Is Out of Whack. Will It Pull AES Back Higher?

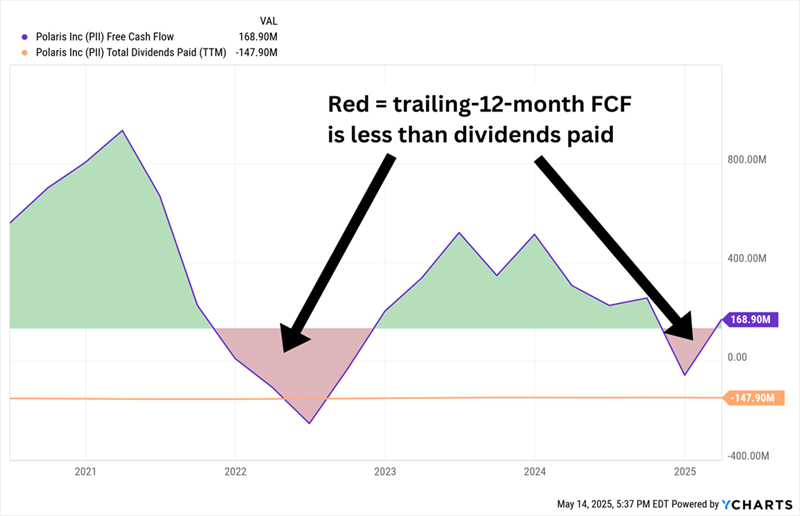

Polaris (PII)

Dividend Yield: 7.0%

Polaris (PII) is pure entertainment—literally. It manufactures ATVs, 4-wheelers, quad bikes, dune buggies, pontoon boats, deck boats, and snowmobiles, plus it’s the name behind Indian Motorcycles and Slingshot open-air roadsters.

However, PII’s stock action over the past year-plus hasn’t been entertaining at all, with the stock down more than 70% from its July 2023 peak, which explains how Polaris’s dividend yield has gone from good to great. The company has spent that time dealing with soft demand spurred by high prices on vehicles and high interest rates, forcing the company to cut back on production. In 2024, revenues dropped by about 20%, while profits cratered by nearly 80%.

The hits have kept on coming in 2025, as tariff uncertainty has withered demand further and forced Polaris to pull its 2025 guidance. Analysts still have their estimates, though, and they’re not great. The Street is expecting a $1.71 per share loss before rebounding to an 8-cent loss in 2026. So, is PII cheap? Well, its PEG is below 0 … but at negative 1.6, that’s nothing to celebrate.

The fact that Polaris has almost 30 years of uninterrupted dividend growth might indicate that it has the financial wherewithal to withstand this weakness. It might—but projections for two years’ worth of negative earnings puts the dividend in at least short-term danger. Even if PII wanted to float it with cash, that’d be a tall ask. It pays roughly $150 million a year in dividends, and it has all of $292 million in cash and investments with $1.6 billion in long-term debt, more than $400 million of which comes due within the next year.

PII’s Dividend: Generous, But Coverage Must Be Closely Watched

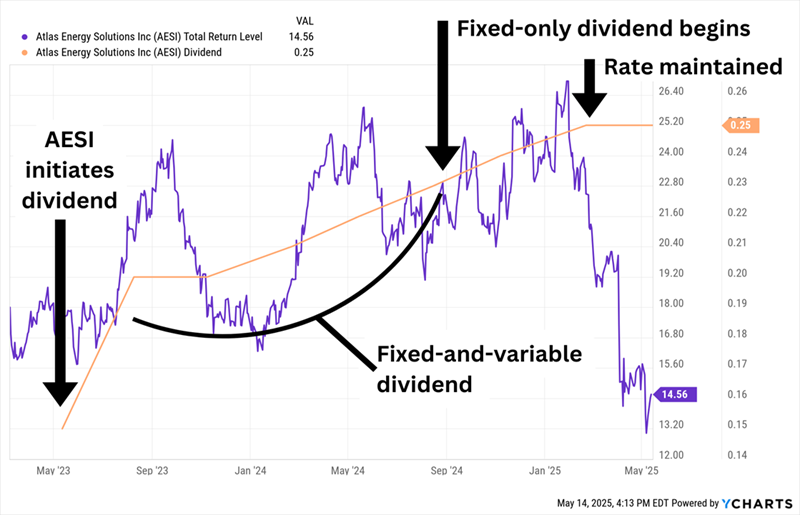

Atlas Energy Solutions (AESI)

Dividend Yield: 7.6%

Atlas Energy Solutions (AESI) is an energy equipment and services company that provides transportation and logistics, storage solutions, and contract labor services to oil and natural gas E&P firms, as well as oilfield services companies, in the Permian Basin of Texas and New Mexico. Most notably, it provides mesh frac sand—a “proppant” that props open the fractures created in the hydraulic fracturing process.

AESI has only been trading since its March 2023 IPO, and it started paying dividends just a couple months after that. And it has been aggressively upping its distributions to shareholders, albeit in an awkward way, as I explained a few months ago.

A Lot of Dividend Drama in Very Little Time

I also said then that:

“What we’re looking for in early February is any further indication that AESI has plans to be a rare quarterly dividend raiser.”

Well, we did get a 4% hike in February, but the company sat still in May, keeping its payout at 25 cents per share. That likely has to do with a downturn in oil prices, which has flattened demand for Permian frac sand and prompted some of Atlas’s customers to defer development products. As a result, the company has delivered two consecutive earnings duds and AESI shares have taken a 40% shellacking. That in turn has dropped AESI to a PEG of 0.2 and a forward P/CF of just 5.5.

For what it’s worth, Atlas has very low-cost assets capable of generating significant cash flows, so the dividend isn’t necessarily in near-term danger—at least not yet. But as it goes in the equipment and services space, AESI needs oil prices to cooperate.

This 11% Dividend Is an URGENT Trump 2.0 Buy

We’re in “wait-and-see” mode on a couple of these names, but we’re not sitting on our hands.

Right now, we’re buying another investment—a closed-end fund (CEF) that ticks off both of our checkboxes in a major way:

- A huge dividend—11%–paid monthly

- A big—and highly unusual—”discount” in disguise!

This isn’t some vanilla index fund. This CEF is actively run by a manager who’s at the top of the bond world. He has been named Fixed Income Manager of the Year by Morningstar, and he has been inducted into the Fixed Income Analysts Society Hall of Fame!

As rates fall and other income options wane, I expect this 11% payer’s discount/dividend combo to be a shiny lure for the mainstream crowd. And we have a shot at “front-running” them today.

Don’t miss this opportunity. Click here and I’ll tell you all about this incredible 11%-paying fund and how to get your FREE Special Report revealing the name, ticker and my detailed research.

Before you make your next trade, you'll want to hear this.

MarketBeat keeps track of Wall Street's top-rated and best performing research analysts and the stocks they recommend to their clients on a daily basis.

Our team has identified the five stocks that top analysts are quietly whispering to their clients to buy now before the broader market catches on... and none of the big name stocks were on the list.

They believe these five stocks are the five best companies for investors to buy now...

See The Five Stocks Here

Discover the 10 Best High-Yield Dividend Stocks for 2025 and secure reliable income in uncertain markets. Download the report now to identify top dividend payers and avoid common yield traps.

Get This Free Report