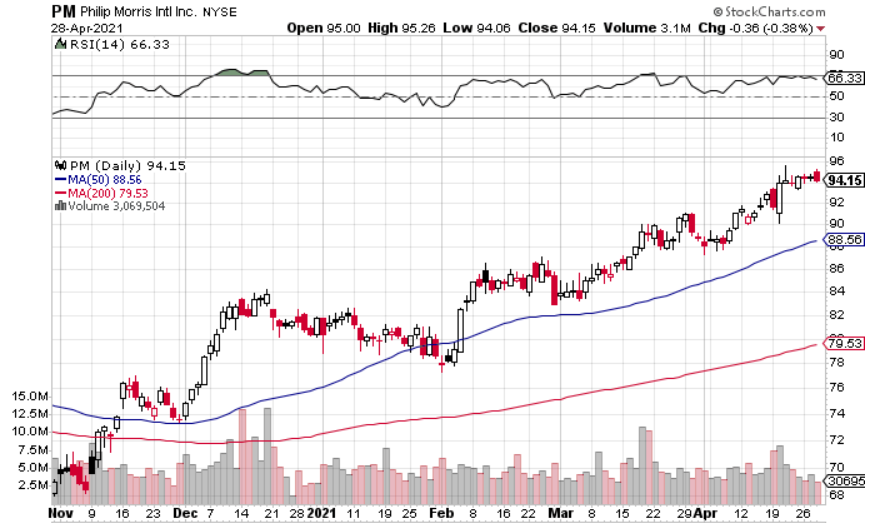

Philip Morris International NYSE: PM broke out of a two-year base in February, and the tobacco giant’s shares have shown no signs of slowing down. In the two-and-a-half months since the breakout, PM shares have moved around 10% higher. That doesn’t sound like a lot, but it’s a big move for a tobacco company. We’re not talking about a high-flying growth stock, after all.

You may have heard about President Joe Biden’s plan to ban menthol cigarettes and significantly reduce nicotine levels. If the plan comes to fruition, wouldn’t it be a huge blow to tobacco companies – including Philip Morris?

No, because Philip Morris International doesn’t sell cigarettes in the United States.

Philip Morris does have a US division, but it is owned by Altria NYSE: MO. So, Altria shares predictably cratered on the news. As did British American Tobacco NYSE: BTI shares. But Philip Morris International shares were barely impacted.

But what if similar regulations are put into place in other countries?

There’s no reason to expect a widespread crackdown on menthol cigarettes and nicotine levels across the world. But even if there is, Philip Morris International investors wouldn’t be too impacted. Particularly in the long run.

Philip Morris Continues Moving Towards Smoke-Free Products

The CFRA expects cigarette consumption to decline by around 3% per year moving forward. Philip Morris sells hundreds of billions of cigarettes per year, so this long-term downtrend seems ominous for shareholders. At least at first glance.

Investors shouldn’t be too concerned because Philip Morris’ reduced-risk product (RRP) segment looks like it can pick up the slack. The company recently reported its fiscal first-quarter earnings; sales of RRPs were up 32.1% yoy and made up 27.9% of overall sales for the quarter. That marked an improvement on an already impressive full-year 2020 for the RRP segment, when sales rose 22.2% yoy to nearly $7 billion, accounting for a little less than a quarter of company-wide sales.

In the first quarter, RRP growth (in dollars, not percentages) was greater than the decline in combustible products. As a result, company-wide sales jumped 6% yoy to $7.59 billion. Earnings-per-share came in at $1.55. Wall Street was expecting revenue of $7.27 billion and earnings-per-share of $1.40, so Philip Morris beat on both the top and bottom lines.

You may be wondering whether Philip Morris faced easy comps from Q1 2020. It turns out that it didn’t; revenue increased 6% yoy in that quarter, well above consensus estimates.

Philip Morris Raised Guidance… Slightly

On the first-quarter earnings call, CFO Emmanuel Babeau said, “While the speed and shape of the global recovery from the pandemic remains uncertain, the strong business results and underlying momentum of the first quarter, notably from our IQOS business led us to raise our outlook.”

Philip Morris now expects revenue to grow 5-7% in full-year 2020 vs. previous guidance of 4-7% growth. That may not seem worth mentioning, but increasing guidance at all in such an uncertain environment is a welcome development. Reading between the lines, it’s possible that Philip Morris is expecting revenue to come in a lot higher than previously expected, but didn’t want to be too aggressive with its estimates.

The Value is Still There

Philip Morris has been one of the best value plays in the market over the last several months. That hasn’t changed – even though shares have appreciated a lot.

Shares are trading at 15.5x forward earnings – not bad at all for a company that is seeing mid-single-digit revenue growth. The forward dividend yield of 5.41% makes Philip Morris one of the most attractive dividend stocks in the market. Unlike some high-dividend stocks, Philip Morris’ dividend seems safe.

How Should You Play Philip Morris?

Philip Morris shares are a bit extended after their recent run-up. Over the last six sessions, however, volume has dried up as shares have traded in a tight range.

Ideally, shares would continue going sideways for another week or two and then break out above $96.

If that happens, you will have a nice entry point on a stock with low downside and moderate upside.

Before you consider Philip Morris International, you'll want to hear this.

MarketBeat keeps track of Wall Street's top-rated and best performing research analysts and the stocks they recommend to their clients on a daily basis. MarketBeat has identified the five stocks that top analysts are quietly whispering to their clients to buy now before the broader market catches on... and Philip Morris International wasn't on the list.

While Philip Morris International currently has a Moderate Buy rating among analysts, top-rated analysts believe these five stocks are better buys.

View The Five Stocks Here

Enter your email address and we'll send you MarketBeat's list of seven stocks and why their long-term outlooks are very promising.

Get This Free Report

Like this article? Share it with a colleague.

Link copied to clipboard.