g class="alignleft" src="https://www.marketbeat.com/logos/articles/small_Depositphotos_220397672_s-2019.jpg" alt="High-Yield Verizon Is A Buy On Post-Earnings Weakness" width="400" height="266">

Verizon Is A Top Pick For High-Yield Investors

We've like Verizon (

NYSE: VZ) for the last 18-months to two years for a variety of reasons that include but not limited to value, yield, growth, the consumer, digital, streaming, 5G, and the IoT. While the former makes the stock an attractive buy the latter makes it a must-own stock, at least in our opinion. The consumer is driving our economy, digital and streaming are high-growth markets, 5G is going to ramp all that into overdrive, and the IoT is quietly waiting for it to happen. There are others in the space but T-Mobile doesn't pay a dividend and AT&T has too much baggage for our taste. The bottom line, Verizon is a

lightly valued blue-chip company supported by secular trends and one that pays a safely growing 4.3% yield.

Mixed Results Fail To Drive Verizon Higher

Shares of Verizon are down following

the Q1 release despite what appears to be a decent report. The two biggest negatives we see are the larger than expected declines in both post-paid and wireless customers and the fact results only barely beat the consensus. Looking at the one in light of the other, the larger than expected decline in post-paid and wireless users can be overlooked. The $32.9 billion in revenue is down from the peak holiday quarter but that was expected. More importantly, the revenue is up 4.1% from last year and 135 basis points above the consensus.

In terms of user count, the post-paid business shed 178K users versus the 42K expected while the wireless business shed 170K versus the expectation for gains. This was offset by gains in other areas, however, the led to positive results for all three business segments. On the consumer end, revenue grew 4.7% on strength in the Fios fiber optic bundle. Fios grew by 80%. On the business end, revenue grew by 1.3% while the Media segment grew a more substantial 10.4%. Moving down to the bottom line, the company's net income increased by 25% over the past year due to cash-saving efforts (reached ahead of target) and business strength. On the bottom line, the GAAP $1.27 is up 27% from last year and beat the consensus by a penny. The adjusted $1.31 grew by at a slower 5% rate but also beat the consensus.

The takeaway for us is that, even with the decline in user counts, the company reaffirmed its guidance for the year. Execs are expecting to see revenue growth at a minimum of 2.0% YOY with total wireless in the range of 3.0%. This should produce earnings in the range of $5.00 to $5.15 versus the $5.07 consensus figure and we think the guidance is light. Aside from the fact that Verizon tends to beat the consensus more often than not, we don't think this guidance takes into account the strength of the rebound and the impact of rapidly improving consumer conditions on phone, Internet, and wireless usage.

Verizon Is A Safely Growing 4.3% Yield

Verizon doesn't pay as much as AT&T but once again there is much less baggage and legacy issue with Verizon. That said, the 4.3% yield is attractive from

the high-yield perspective and it is backed up by some solid metrics. To start, the payout ratio is fairly low at 50% and there is room to bump it up on the cash-flow statement. Looking at the balance sheet, the company is well-capitalized with some debt but there are two things to consider. First, even at current levels the company is only moderately levered and has reasonable coverage so no threat to the distribution. Second, debt is coming down and helping to free up the cash flow. The takeaway here is the current payout is safe and the outlook for a 9th consecutive dividend is good, but we don't recommend counting on a large one.

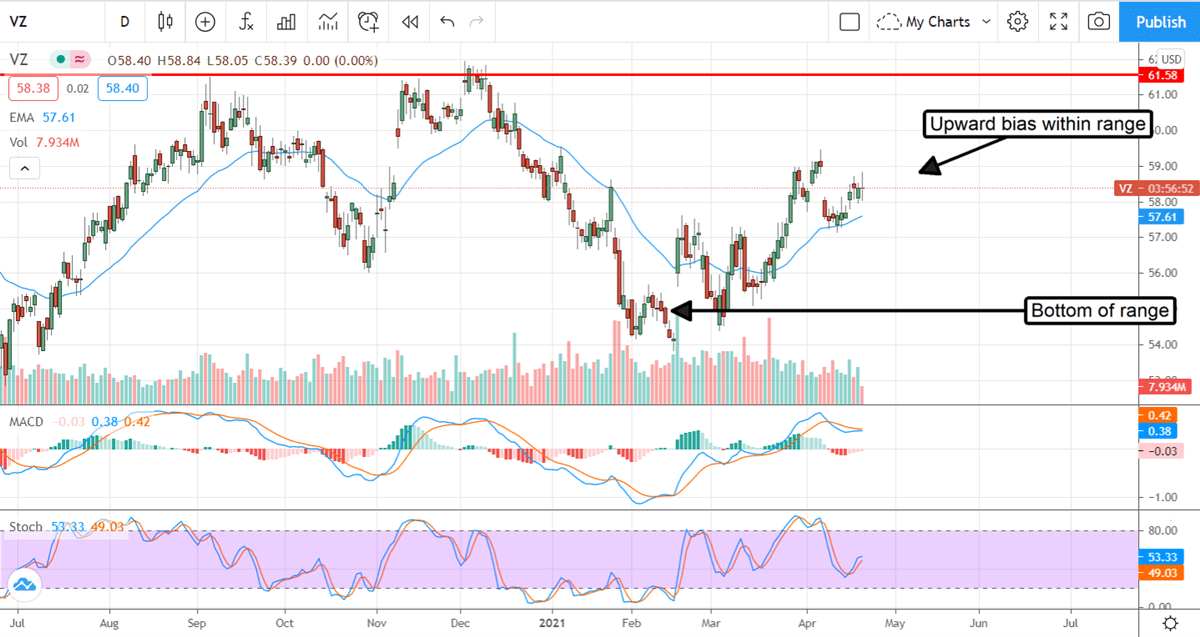

The Technical Outlook: Verizon Pulls Back Into A Buying Opportunity

Shares of Verizon pulled back after the Q1 report but are already showing signs of support. Support appears to be near the $58 level which is consistent with

past price action. The indicators are still mixed but have a bullish bias which suggests a swing in momentum is about to carry this stock higher. The next key level of resistance is at $59, once the stock gets back above there we see it moving up into the end of the year and closing well above the $62 level.

Before you consider Verizon Communications, you'll want to hear this.

MarketBeat keeps track of Wall Street's top-rated and best performing research analysts and the stocks they recommend to their clients on a daily basis. MarketBeat has identified the five stocks that top analysts are quietly whispering to their clients to buy now before the broader market catches on... and Verizon Communications wasn't on the list.

While Verizon Communications currently has a Moderate Buy rating among analysts, top-rated analysts believe these five stocks are better buys.

View The Five Stocks Here

Unlock the timeless value of gold with our exclusive 2025 Gold Forecasting Report. Explore why gold remains the ultimate investment for safeguarding wealth against inflation, economic shifts, and global uncertainties. Whether you're planning for future generations or seeking a reliable asset in turbulent times, this report is your essential guide to making informed decisions.

Get This Free Report

Like this article? Share it with a colleague.

Link copied to clipboard.

View Alphabet Inc. Purchases Shares of 8,943,486 AST SpaceMobile, Inc. (NASDAQ:ASTS)Alphabet Inc. Purchases Shares of 8,943,486 AST SpaceMobile, Inc. (NASDAQ:ASTS)By MarketBeat | July 17, 2025

View Alphabet Inc. Purchases Shares of 8,943,486 AST SpaceMobile, Inc. (NASDAQ:ASTS)Alphabet Inc. Purchases Shares of 8,943,486 AST SpaceMobile, Inc. (NASDAQ:ASTS)By MarketBeat | July 17, 2025 View Teacher Retirement System of Texas Takes Position in Rivian Automotive, Inc. (NASDAQ:RIVN)Teacher Retirement System of Texas Takes Position in Rivian Automotive, Inc. (NASDAQ:RIVN)By MarketBeat | July 16, 2025

View Teacher Retirement System of Texas Takes Position in Rivian Automotive, Inc. (NASDAQ:RIVN)Teacher Retirement System of Texas Takes Position in Rivian Automotive, Inc. (NASDAQ:RIVN)By MarketBeat | July 16, 2025 View Why Wall Street Is Betting on These 3 Comeback StocksWhy Wall Street Is Betting on These 3 Comeback StocksBy Nathan Reiff | July 12, 2025

View Why Wall Street Is Betting on These 3 Comeback StocksWhy Wall Street Is Betting on These 3 Comeback StocksBy Nathan Reiff | July 12, 2025 View QuantumScape (QS) to Release Quarterly Earnings on WednesdayQuantumScape (QS) to Release Quarterly Earnings on WednesdayBy MarketBeat | July 18, 2025

View QuantumScape (QS) to Release Quarterly Earnings on WednesdayQuantumScape (QS) to Release Quarterly Earnings on WednesdayBy MarketBeat | July 18, 2025 View Joby vs. Archer: Which eVTOL Stock Is Better for Your Portfolio?Joby vs. Archer: Which eVTOL Stock Is Better for Your Portfolio?By Jeffrey Neal Johnson | July 14, 2025

View Joby vs. Archer: Which eVTOL Stock Is Better for Your Portfolio?Joby vs. Archer: Which eVTOL Stock Is Better for Your Portfolio?By Jeffrey Neal Johnson | July 14, 2025