While vanilla income investors limit their search to mere “common” dividends, we contrarians know where the real payout party is at—with preferred divvies.

Let’s talk about three preferred-stock vehicles that pay from 6.9% to 9.4%. All three of these funds dish monthly dividends.

And these payouts receive preferential treatment over common-stock dividends, making them safer than the common payouts offered by regular ol’ equities.

There are four main ways to buy preferreds, and three of them have some serious headaches and drawbacks:

- Individual preferred stocks: Research resources for individual preferred shares are few, far between and often require expensive paid subscriptions. Buying individual preferreds requires a lot of capital to diversify. We have to manage the preferred portfolio ourselves.

- Preferred mutual funds: Mutual funds solve a lot of the problems of buying individual preferreds. They also pay us monthly, whereas individual preferreds often pay quarterly or even semiannually. However, they may charge expensive annual fees. They may also charge front-end sales loads that really handicap our performance. They also usually require minimum purchases in the thousands of dollars.

- Preferred exchange-traded funds (ETFs): ETFs provide many of the same benefits of preferred mutual funds. But there are no investment minimums, fees are cheaper because they’re usually index funds, and we can buy and sell them during the trading session. However, because they’re often index funds, they’re tightly tied to their strategy—which means they can’t take advantage of discounts like managers can. Performance can be underwhelming.

- Preferred closed-end funds (CEFs): CEFs merge aspects of mutual funds and ETFs, solving for each other’s shortfalls. CEF managers can make the most of market opportunities, but CEFs trade throughout the day like ETFs and also don’t have investment minimums—all we need is the cost of a share. CEFs can also use debt leverage to boost returns and distributions. CEFs also use options to further juice income. CEFs also aren’t tied as tightly to their net asset value (NAV), so they can sometimes trade at discounts, allowing us to buy their underlying assets for cheaper. So, while CEF fees tend to be higher, performance can easily make up for it (and then some).

CEFs really do outperform their ETF “benchmark.” Consider this chart of three preferred-stock CEFs versus iShares Preferred and Income Securities ETF (PFF)—all three CEFs boast better returns than the popular PFF:

PFF Versus Preferred CEFs: The Price of Popularity

Of course preferred CEFs aren’t perfect. Fees are higher. The use of leverage makes preferreds swing more drastically than ETFs and mutual funds. And when preferreds heat up, CEFs can actually trade at a premium to NAV, which can drag on performance if we buy in at the wrong time.

That all said, CEFs are generally the easiest and most effective way for us to buy preferreds. Now let’s talk about the three that pay up to 9.4% in monthly divvies.

John Hancock Premium Dividend Fund (PDT)

Distribution Rate: 7.8%

I want to start with a “hybrid” preferred fund: the John Hancock Premium Dividend Fund (PDT).

PDT is technically an allocation fund (stock plus fixed income), split roughly 50/50 between preferred stocks and dividend-yielding common stocks. It’s a brilliant idea—combining two great income tastes—that I’m surprised isn’t more prevalent in ETF-land, where they can build an index and launch a product overnight.

Not that I’d trust an index with this kind of portfolio.

John Hancock’s team of capital and credit managers have built a pretty tight portfolio of around 125 holdings. Utilities, which are directly stated as part of the fund’s strategy, make up the vast majority of common-stock holdings. Financials make up the bulk of the preferred allocation—a surprise to no one familiar with preferred portfolios. Top holdings include high-yielding commons from telecoms AT&T (T) and Verizon (VZ), as well as utilities like Duke Energy (DUK) and BP (BP), but also preferreds like a 7.56% series from Citizens Financial.

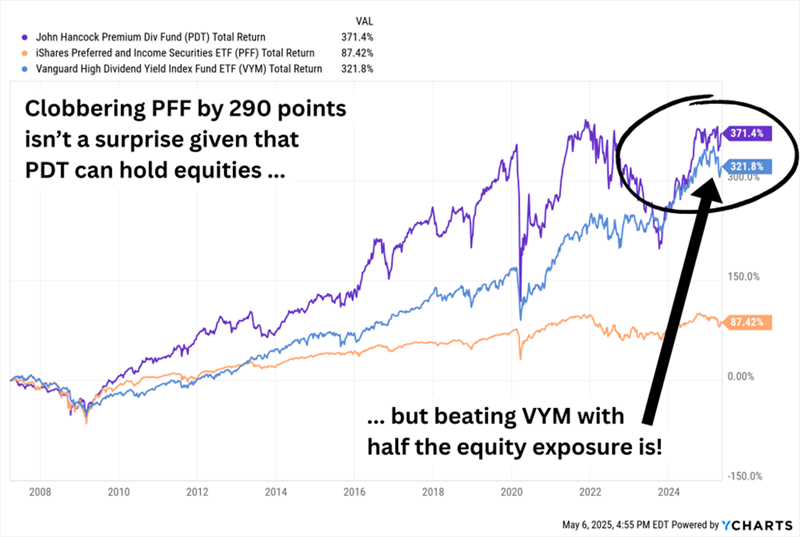

PDT has historically beaten up on plain-vanilla preferred ETFs like the iShares Preferred and Income Securities ETF (PFF). Of course it has. Not only does it have the benefit of owning some traditional equities, but management also uses a high amount of leverage (34% currently), which lets it make even more out of bull markets.

Perhaps more surprising is its performance against pure high-yield common-dividend-stock funds:

John Hancock’s Hybrid Mix Has Been Better Than Either Pure-Play Side

The tradeoff, as the chart clearly shows, is volatility. Whereas basic preferred funds are often held to stabilize portfolios, John Hancock’s fund’s equity holdings and leverage are more geared toward performance than comfort.

Fortunately, PDT actually delivers that performance, making it worthy of a look—especially when it trades at a discount to NAV, which it does right now. A 6% sale on PDT’s assets might not sound like much, but over the past five years, the CEF has traded at a premium on average.

Flaherty & Crumrine Dynamic Preferred and Income Fund (DFP)

Distribution Rate: 6.9%

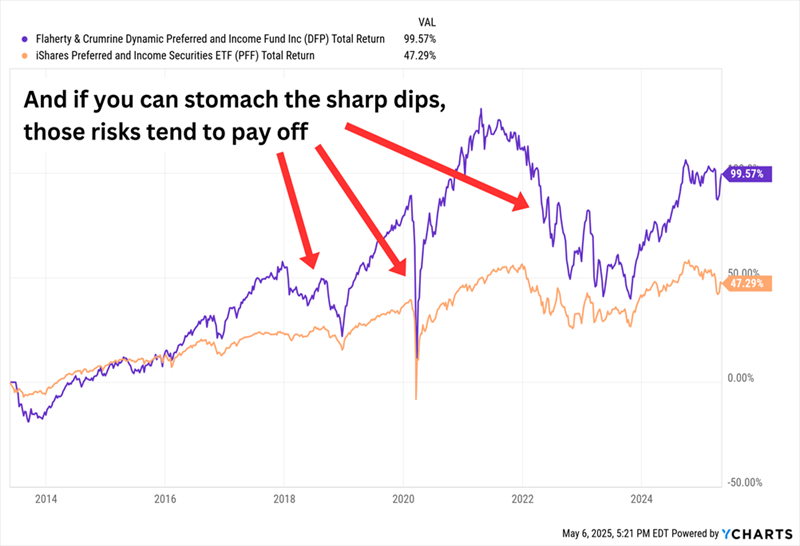

Traditionalists will lean more toward funds such as the Flaherty & Crumrine Dynamic Preferred and Income Fund (DFP), which is as straightforward a preferred CEF as we could ask for.

DFP holds about 250 positions, nearly 80% of which are issues from financial-sector firms. This is also a “global” fund, split about 70 domestic/30 international, so in addition to preferreds from the likes of Citigroup (C) and Morgan Stanley (MS), we also get exposure to preferreds from Lloyds Banking (LYG) and Banco Santander (SAN).

Management is more than happy to take some hard swings, too. About half of the portfolio is below-investment-grade, and DFP juices performance and yields further with nearly 40% debt leverage.

DFP Takes Risks to Earn Rewards

Flaherty & Crumrine’s preferred CEF also offers the best headline pricing of the bunch, at an 8% discount to NAV. And like with PDT, it’s also a relative bargain compared to its five-year average discount, which sits around 2%.

(Readers enjoyed 57% total returns from DFP in my Contrarian Income Report service.)

First Trust Intermediate Duration Preferred & Income Fund (FPF)

Distribution Rate: 9.4%

Most preferred stocks are perpetual in nature. They don’t have expiration dates, and thus duration isn’t usually necessary when evaluating preferred-stock funds.

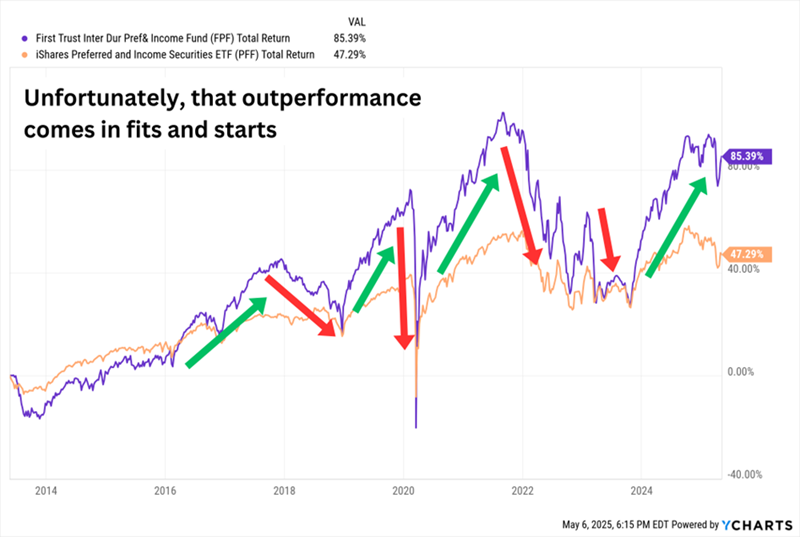

First Trust Intermediate Duration Preferred & Income Fund (FPF) is different, aiming for a portfolio duration of between three and eight years (and currently sits near five).

If we back out the emphasis on duration, FPF looks an awful lot like a regular preferred CEF. Financials command a clear majority of assets. It’s not afraid to shy away from international preferreds, which make up more than 40% of assets (Canada alone accounts for 15%). Leverage is high, at 34%. Dividends are high, at nearly 10%. Those dividends come each and every month.

FPF Has Also Wiped the Floor With iShares’ Preferred ETF

Two things about FPF that stand out more than anything?

On the upside, First Trust’s CEF has pretty great credit quality, with about two-thirds of assets in investment-grade preferreds. Another 15% or so is in BB+, the highest junk tier. Sure, that’s why FPF, while better than PFF, hasn’t performed as well as the prior two funds. But it’s also why FPF boasts the lowest volatility of the three (as measured by beta) over every meaningful time period.

On the downside, we’re getting a “phantom” sale on FPF right now. It currently trades at a 5% discount to NAV, but over the past five years, it has actually traded at a 6% discount on average.

A Fully Paid Retirement for Just $500,000?

Why do I love preferred CEFs? Because big monthly dividends are one of the best ways to retire comfortably with as little as $500,000.

My 8%+ Monthly Payer Portfolio dishes $40,000 in dividends on this relatively modest nest egg.

Got a million? Great—we’re looking at $80,000 or more.

Better still? The money comes in about every 30 days because we are focused on monthly payers.

No “lumpy” payouts. No complex dividend calendars. No dumping money into certain stocks because you’re getting underpaid every third month.

Just paydays as smooth as when you were collecting a check from work!

Don’t miss out on these terrific income plays while you can still get in at a bargain. Click here for all the details, and to download a FREE Special Report revealing my favorite stocks and funds.

Before you make your next trade, you'll want to hear this.

MarketBeat keeps track of Wall Street's top-rated and best performing research analysts and the stocks they recommend to their clients on a daily basis.

Our team has identified the five stocks that top analysts are quietly whispering to their clients to buy now before the broader market catches on... and none of the big name stocks were on the list.

They believe these five stocks are the five best companies for investors to buy now...

See The Five Stocks Here

Looking to profit from the electric vehicle mega-trend? Enter your email address and we'll send you our list of which EV stocks show the most long-term potential.

Get This Free Report