The market-at-large is expensive by historical metrics. So let’s look past the pricey, low-yielding ETFs in favor of cheap dividend stocks.

That’s right, good ol’ value investing bargains. With high yields too! We’re talking about divvies of 5%, 8% and even 11% that we’ll discuss in a moment.

The spring market dip sure was brief, wasn’t it? The S&P 500 sank into near-bear territory in roughly a month, then snapped back just as quick.

Now? If We’re Buying the Market, We’re Buying Even Higher

In doing so, Mr. and Ms. Market took valuations to high levels. The S&P 500’s forward price-to-earnings (P/E) ratio of 22.1 remains in rarefied air, last reached during the COVID rebound, and before that, the dot-com bubble.

Which is fine. We’ll leave the 22 P/Es to the vanilla investors while we focus on bargains with respect to two “cash is king” metrics:

- Big dividends: These generous stocks dish out 4x to 9x the market’s yield.

- Cheap price-to-cash-flow: These companies are priced dirt cheap with respect to the cash flow they generate.

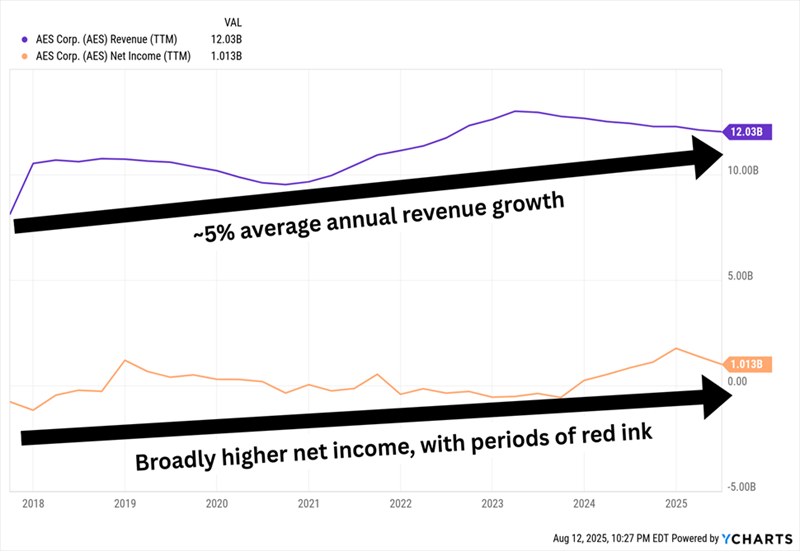

Let’s start with Virginia-based electric utility AES Corp. (AES, 5.5% yield), which we recently discussed as a low-beta name. This means AES, being a safe, stodgy utility, is more insulated from market pullbacks than run-of-the-mill dividends.

AES also has upside potential. Its renewable energy-selling business gives it growth potential that many utility stocks don’t have.

Potential, But So Far, It Hasn’t Shown Up Much in Practice

It’s also cheap. AES trades at a cheap 5 times cash-flow estimates, as well as a 0.6 PEG that implies it’s also cheap compared to its growth estimates. (Remember: A PEG under 1.0 signals that a stock is inexpensive.) The stock yields more than 5%, to boot, which is better than the already generous utility sector.

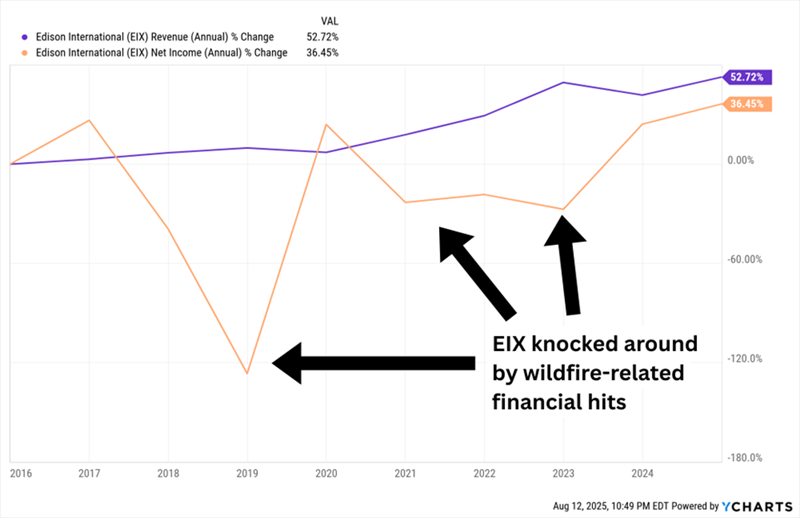

Edison International (EIX, 5.9%) is another utility company—this one more typical of the sector. It’s the parent of regulated utility Southern California Edison (SCE), which serves more than 15 million customers and generates much of its electricity from renewable sources including solar, wind, and hydro. It does, however, have a second business—Trio (formerly Edison Energy), a global energy advisory firm that serves large commercial, industrial and institutional organizations.

Unlike other utilities, however, EIX is a bit more “exciting.” It spent years in court fighting litigation over wildfire damage and ended up having to pay multiple billion-dollar-plus settlements. And the legal drama has returned in 2025. Shares have lost more than a quarter of their value, with most of that coming in January amid Los Angeles County wildfires, including the massive Eaton Fire, which prompted multiple suits against SCE over allegations that the company had “violated public safety and utility codes and was negligent in its handling of power safety shut-offs.” SCE is also being investigated in connection with the Hurst Fire.

In Fact, Wildfire Woes Have Been Par for the Course

If, for a minute, we closed our eyes and ignored all that, there’s a lot to like about Edison. It’s expected to generate decent top-line growth and a significant snap-back in profits over the next couple years. The big drop in shares has launched EIX’s yield to nearly 6%. It trades at just 3 times cash-flow estimates. And its PEG, which at fractionally under 1 suggests the stock is only mildly underpriced, is substantially down from the nearly 3 it traded at when I evaluated the stock a couple years ago.

But we can’t ignore the fire liabilities—they’re why EIX’s valuations are so low. That makes Edison a much bigger high-risk, high-reward gamble than the average utility.

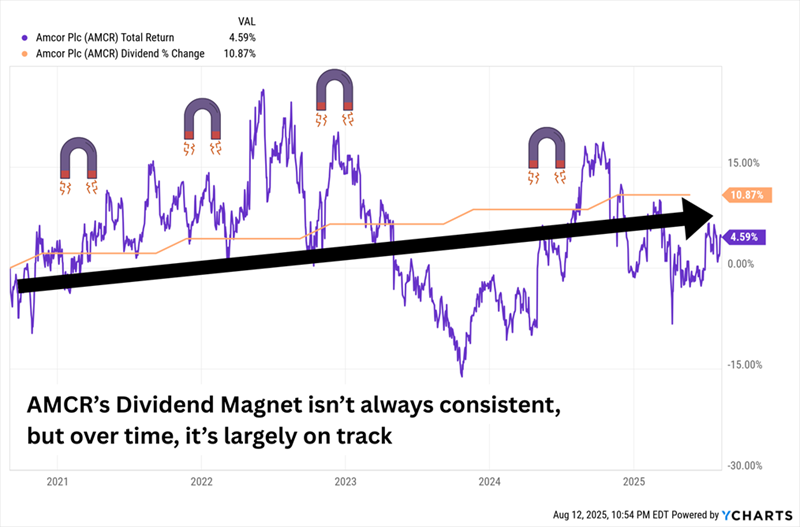

Amcor (AMCR, 5.2% yield) is technically a cyclical stock, but it acts defensively. That’s because, as a packaging specialist, it’s in the business of—well, other business’s business. It makes everything from high-barrier paperboard trays for beef and meats to glass dressing bottles to overwrap for home and personal care. And its applications go far beyond the grocery store: Amcor’s products are used in garden and outdoor products, agriculture, pet care, healthcare, even building and construction. So Amcor is simultaneously a play on the broader economy and all the businesses it supports, but it also fills a vital need across a diversified set of companies.

AMCR stands out for a few reasons:

- It’s a Dividend Aristocrat with a 5%-plus yield, which is rare. The hallowed group of dividend growers know how to stack pennies over time, but their headline numbers often leave a lot to be desired.

- Amcor’s shares tend to be less volatile than most.

- The stock is cheap, at least as far as cash flow is concerned; P/CF is roughly 6x right now. It’s a little less attractive by other metrics; its forward P/E (12) is so-so, and its PEG (1.3), while cheaper than the market, is still a bit overpriced.

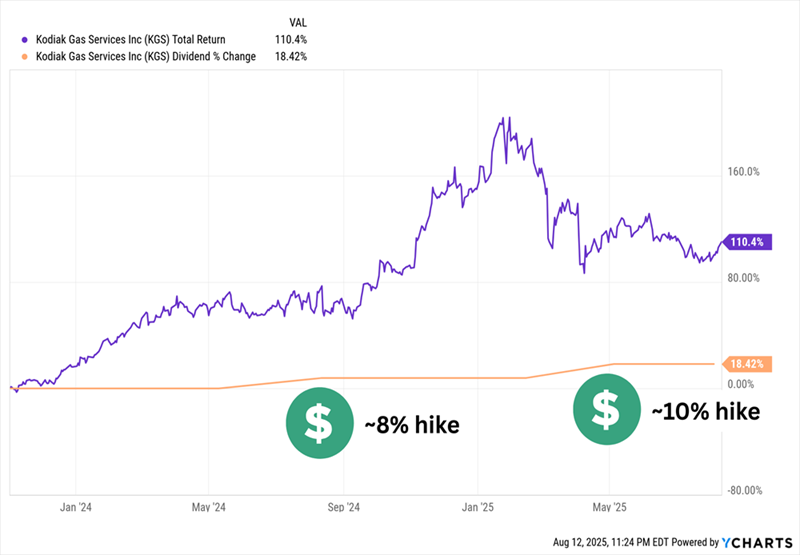

Kodiak Gas Services (KGS, 5.2% yield) is an energy services firm that provides natural gas compression services, mostly in the Permian Basin of Texas and New Mexico. Its compression units are critical to upstream and midstream natural gas firms, so it’s able to secure multiyear, fixed-revenue contracts. There’s nothing novel about the business model, though. Like other energy services firms, if natural gas/liquefied natural gas (LNG) is in demand, Kodiak will be in demand, so the fact that global LNG demand is expected to grow over the next few years bodes well for KGS.

That’s in large part because Kodiak is extremely well-positioned to capture that growth. In late 2023, KGS announced it would acquire CSI Compressco LP to create the industry’s largest compression fleet. Kodiak’s fleet is young, too (read: less maintenance and replacement costs).

There’s not much stock history to examine, however. Kodiak is a relatively new issue that went public just a few months before the CSI announcement. But the company has started a dividend and raised it twice since then, including a nearly 10% improvement announced in April 2025.

A Stock Doubler-Plus + A New and Rising Dividend. Nice Start!

Meanwhile, its yield has wafted up to over 5% amid energy’s weakness this year—and left shares relatively cheap. KGS trades at roughly 6 times cash flow estimates and a low PEG of 0.13.

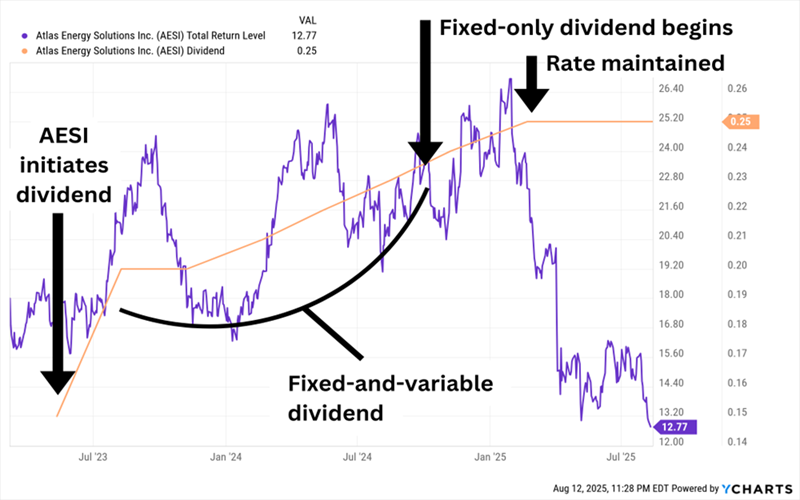

Atlas Energy Solutions (AESI, 8.4% yield) is another Permian Basin energy equipment and services firm, this one providing transportation and logistics, storage solutions, and contract labor services to oil and natural gas E&P firms, as well as other oilfield services companies. Its most important offering is mesh frac sand used in hydraulic fracturing (fracking). I had been keeping tabs on it because of its unorthodox streak of dividend hikes, but that streak stopped earlier this year.

The Trap Door Opened Soon After AESI Stopped Raising

It’s not ideal. Nor is the fact that AESI shares have been hammered to the tune of 45% this year. Again, energy services haven’t had a great 2025, but Atlas has been downright miserable amid slower-than-expected U.S. completion activity and droopy frac-sand prices. If there’s any silver lining to that, it’s that AESI shares now trade at just 5.7 times estimates for cash flows, as well as an attractive PEG of 0.75.

The dividend at least appears to be safe, too. While things look bad from an adjusted earnings perspective ($1.00 in dividends annually vs. forecasts for just 25 cents this year), Atlas has more than enough FCF to cover the payout. Example: Last quarter, it generated $48.9 million in adjusted FCF while paying out $30.9 million. Those cash flows are substantial because AESI is a low-cost operator—crucial for survival in this industry. But like any energy services provider, Atlas needs commodity prices to cooperate.

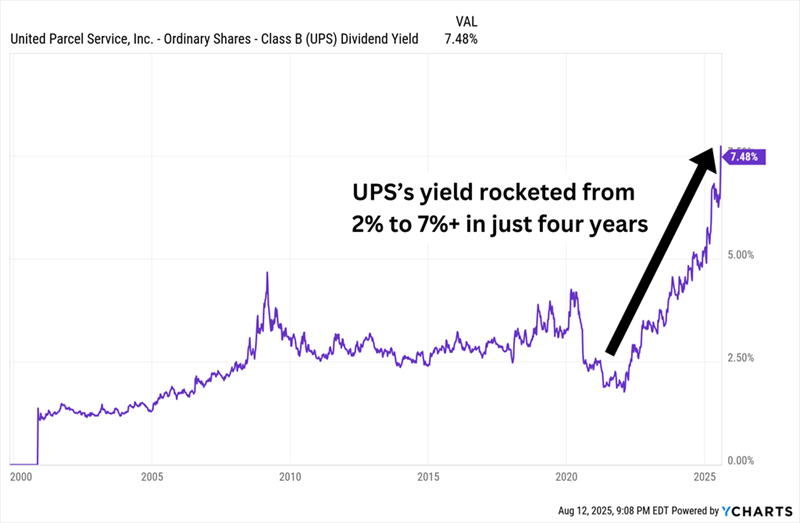

It’s unusual for a blue-chip stock like United Parcel Service (UPS, 7.5%) to yield north of 7%, but it’s also rare for a blue-chip stock like UPS to have its shares hemorrhage so much without a recession or broader bear market.

Lower-margin e-commerce volumes, higher costs because of its unionized workforce, and a weak freight environment hampered the company in 2024.

Then in early 2025, it spooked investors with a weak 2025 forecast and announced that—in hopes of shifting away from those lower-margin volumes—it would drastically reduce its business with Amazon (AMZN), which accounted for roughly 10%-12% of annual UPS revenues. The April tariff announcement also hit shares hard.

The result? UPS shares have lost nearly half of their value in just two years.

The upshot? UPS trades at roughly 8 times cash-flow estimates and has never offered a better yield in its 26 years of trading.

Sadly, Dividend Growth Had Little to Do With It

Is UPS a dividend trap? Perhaps. The company pulled its full-year revenue and profit forecasts in April, and didn’t bring them back in its late July report.

Meanwhile, Wall Street is expecting a roughly 15% drop in adjusted earnings, to $6.61 per share. That specific number matters: UPS has a target dividend payout ratio of approximately 50% of prior-year adjusted EPS. It currently pays $6.56 across four quarterly dividends. (That’s 99%!) CEO Carol Tomé continued to signal commitment to the dividend in the earnings call—“UPS is rock-solid strong and so is our dividend. The UPS dividend is backed by solid free cash flow and a strong investment-grade balance sheet,” she said—but if the delivery giant continues to struggle, simple numbers might force management’s hand.

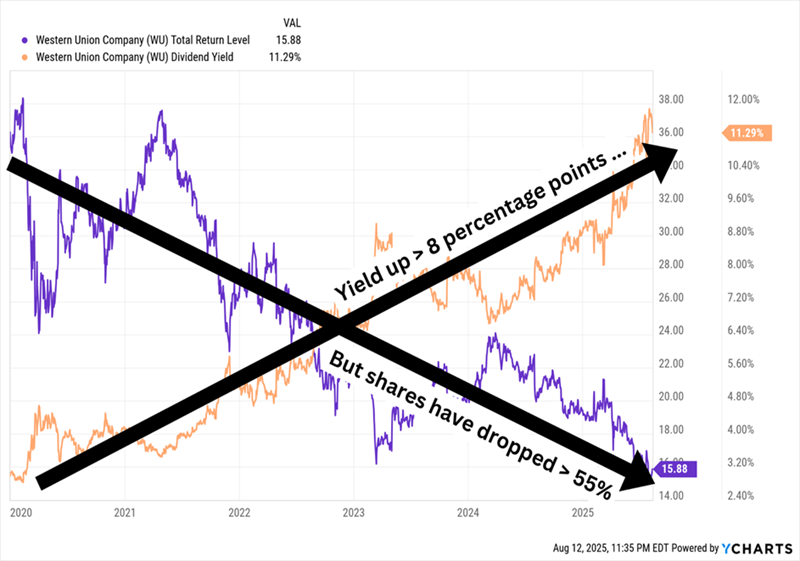

Western Union (WU, 11.3% yield), somehow, is still in business. Payment apps like PayPal, Venmo and Zelle have been taking business from the “OG” of money transfer. WU boasts a big yield but for the wrong reason—its divvie looks big because shares are (deservedly) way down!

Western Union Has Been Headed South for Years

WU, to its credit, has launched an initiative called “Evolve 2025” in which it’s rolling out new products, improvements and an operational efficiency program. It’s also expanding its digital wallet offerings in Mexico and Singapore. And its latest move, announced just a couple days ago, is the $500 million acquisition of Miami-based International Money Express (IMXI), aka Intermex, which serves some 6 million customers who send money from the United States, Canada, Spain, Italy, the United Kingdom, and Germany to more than 60 countries.

But c’mon man—this dog is dead. The business trades for 4x cash flow and a sub-5 forward P/E, but who cares? Not me.

Fortunately, we don’t have to stretch as far as buying Western Union to secure high yields right now. In fact, I know 3 incredible dividend payers dishing out yields up to 10%—and they even pay us monthly! Click here for the details.

Before you make your next trade, you'll want to hear this.

MarketBeat keeps track of Wall Street's top-rated and best performing research analysts and the stocks they recommend to their clients on a daily basis.

Our team has identified the five stocks that top analysts are quietly whispering to their clients to buy now before the broader market catches on... and none of the big name stocks were on the list.

They believe these five stocks are the five best companies for investors to buy now...

See The Five Stocks Here

Wondering where to start (or end) with AI stocks? These 10 simple stocks can help investors build long-term wealth as artificial intelligence continues to grow into the future.

Get This Free Report