The “big, beautiful bill” has turned into a bitter pill for bonds. As you’ve undoubtedly heard, bond buyers aren’t exactly thrilled about lending more money to a $36 trillion debtor that’s digging itself deeper into a financial ditch.

Prior to the proposed “One Big Beautiful Bill Act” (OBBBA), the Congressional Budget Office (CBO)—famous for crunching numbers through rose-colored glasses—already projected a $1.9 trillion deficit for 2025. Now, the CBO estimates that the current House-passed version of OBBBA will add an extra $3.8 trillion to the national debt over the next decade.

This leaves Uncle Sam staring into a $40 trillion hole, deepening by roughly $2 trillion each year.

Treasury bond yields spiked recently as buyers vanished. Last Wednesday, a seven-week stock rally reversed midday when the U.S. struggled through a weak $16 billion auction of 20-year bonds. The tepid demand for these long-dated Treasuries confirmed what many already thought—with Uncle Sam spending like a drunken sailor, who’d lend him more?

Thus, the popular mainstream conclusion: The U.S. has entered its final “doom loop” debtor stage. Rates are rising as bond investors demand higher compensation to offset the credit risk posed by Uncle Sam’s ugly finances (you know, $40 trillion…).

Higher rates increase the country’s financing costs, which worsens the debt situation, which leads investors to demand even higher rates, and so forth. This implies we should avoid bonds entirely.

To borrow a concept from billionaire investment manager Howard Marks, this is a “first level” interpretation. It is accurate on paper but misses the nuances.

In a truly free market, the “bond doom loop” narrative would be valid. But in the real world that you and I inhabit, my fellow contrarians, we must elevate our thinking to the second level for more nuanced consideration.

Here, we recognize the “Quiet QE” the U.S. Treasury began under then-Secretary Janet Yellen. She subtly influenced the bond market by issuing short-term debt rather than long-dated Treasuries. This maneuver reduced the supply of long-term bonds, thereby suppressing long-term yields. (The same number of buyers chased fewer long-dated bonds, pushing prices higher and yields lower.)

This strategic pivot was significant. At the end of 2019, short-term bills represented just 15% of marketable U.S. debt. By 2024, Yellen funded 75% of the deficit via the short end of the yield curve.

Two summers ago at Contrarian Outlook, we identified this Quiet QE interplay between Yellen and Fed Chair Jay Powell. Renowned economist Nouriel Roubini published a paper 12 months later identifying this “activist Treasury issuance” (ATI) as Uncle Sam’s favorite plumbing tweak.

Roubini confirmed the U.S. Treasury is, shall we say, finessing debt issuance to nudge longer-term rates lower than they’d naturally be. Without ATI, the 10-year Treasury yield would be 30 to 50 basis points higher—equivalent to up to two rate hikes in the Fed Funds rate.

In other words, the 10-year yield would top 5% today if not for Quiet QE. And the cost of borrowing for business (lending rates) and individuals (mortgage rates) would be notably higher.

Current Treasury Secretary Scott Bessent publicly criticized this tactic but has quietly continued it. Year-to-date, the Treasury has financed 80% of its funding needs through short-term issuance. If we witness more weak auctions like last week’s, Bessent could very well lean even harder into lower cost short-term borrowing.

Short-term rates are influenced primarily by the Federal Reserve rather than the broader bond market. And Jay Powell’s term ends in less than a year, when President Trump will likely appoint an ally like Kevin Warsh, Kevin Hassett, or Judy Shelton, who will cooperate with the administration to lower the Fed Funds rate.

A lower Fed rate will in turn reduce short-term Treasury yields. With 80% of issuance short term, this will significantly lower debt-service costs. In fact, this is already happening. Fellow financial author Mel Mattison notes that total interest on the public debt is declining year-over-year despite a ballooning deficit!

Mel reminds us that Powell didn’t start cutting the Fed Funds Rate until last September. So, this fall the decline in interest payments will really start showing up in the year-over-year data. More evidence against the case of the “interest rate doom loopers.”

Does this fix the giant US debt problem? Of course not. But Mel’s point is that our politicians and central bankers have “creative options” at their disposal. Vanilla investors tend to glance at the surface and move on. But we careful contrarians appreciate the nuances and gear our income portfolios accordingly.

The somewhat-secret swap to short-term debt should bring a ceiling on long-term yields. Bessent, after all, is not going to tolerate a higher 10-year yield that boosts interest on the debt. He wants a cap on long rates, which will provide a floor beneath the bond market. He’ll get one by limiting long-dated bond supply.

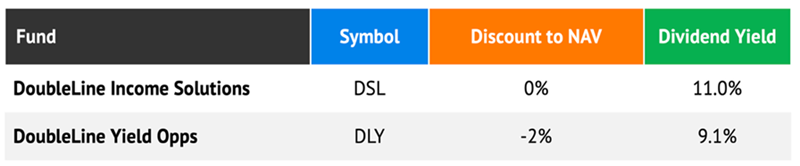

Viewed through this lens, our DoubleLine bond funds look attractive here. If long rates are near a high watermark, then the prices of the paper owned by DoubleLine will enjoy a yield-driven tailwind. DoubleLine Yield Opportunities Fund (DLY) yields 9.1% and trades at a 2% discount to its net asset value (NAV), while DoubleLine Income Solutions Fund (DSL) pays an 11% yield and trades at par.

These two bond portfolios are also supported by a strengthening economy. The negative first-quarter GDP print was likely the most bullish development for the real economy. Trump and Bessent will make sure we don’t experience negative GDP growth in the second quarter.

Consecutive negative quarters would officially signal a recession. They don’t want this scarlet letter heading towards the midterms. Trump and Bessent no longer need an economic slowdown to push long-term yields lower—they’ll simply work with the short end of the bond market from here.

Political pressure on Powell, the “lame duck” , will ease. As will pressure on the long end of the curve.

Let’s ignore the mainstream Chicken Littles declaring the end of bonds. These “first level” thinkers overlook the power of coordinated Treasury and Fed policy. Here at Contrarian Outlook we recognize the monetary “creativity”—and profit from it. Let’s keep enjoying these DoubleLine monthly payers yielding up to 11%.

For income investors who know where to look, there are more monthly dividend payers—yielding 8%+ annually—with underappreciated nuances. These dividend deals are available because, quite frankly, most individual investors (and money managers) don’t do their homework.

We contrarian income seekers specialize in the academic aspect of our work. Which is why we are able to identify 8%+ dividends like these that are ideal to retire on.

Before you make your next trade, you'll want to hear this.

MarketBeat keeps track of Wall Street's top-rated and best performing research analysts and the stocks they recommend to their clients on a daily basis.

Our team has identified the five stocks that top analysts are quietly whispering to their clients to buy now before the broader market catches on... and none of the big name stocks were on the list.

They believe these five stocks are the five best companies for investors to buy now...

See The Five Stocks Here

Enter your email address and we'll send you MarketBeat's list of ten stocks that are set to soar in Fall 2025, despite the threat of tariffs and other economic uncertainty. These ten stocks are incredibly resilient and are likely to thrive in any economic environment.

Get This Free Report