Let’s invest like private equity pros without needing seven figures. Yes, that’s right—PE-style starting for as little as $8.

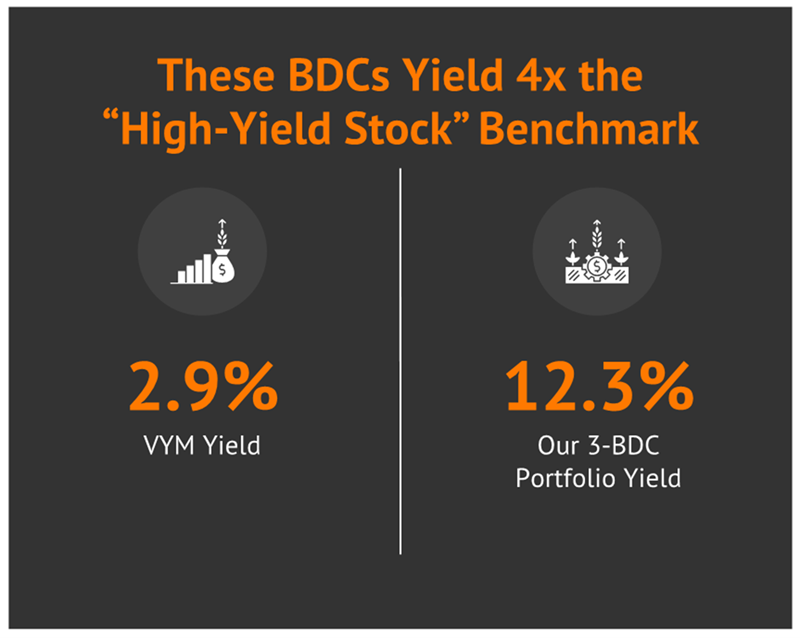

Plus, yields up to nearly 13%.

No special access or options trades needed. Just a few clicks through our brokerage accounts buying regular ol’ tickers.

The sneaky dividend-dishing subjects? Meet business development companies (BDCs), publicly-traded firms that lend to small businesses.

BDCs were invented by Congress years ago to create a new type of lender to small businesses. They were also given the same mandate as real estate investment trusts (REITs): Return at least 90% of taxable income back to shareholders in the form of dividends.

And man, do they pay or what?

Let’s dive into three compelling BDCs that not only dish big dividends but also trade for less than the sum of their parts.

BlackRock TCP Capital Corp. (TCPC)

Dividend Yield: 12.9%

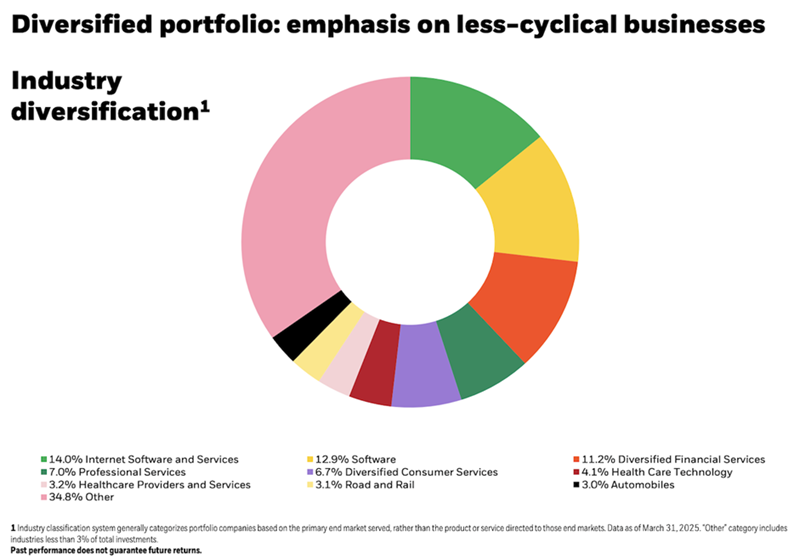

BlackRock TCP Capital Corp. (TCPC) is a middle-market lender that favors middle-market companies with enterprise values of between $100 million and $1.5 billion. It has a fairly diverse portfolio of 146 companies across several “less-cyclical” industries.

Source: BlackRock TCP Capital Corp. Q1 2025 Investor Presentation

TCPC’s investment mix is heaviest in first-lien debt, at 83% of the portfolio; second-lien debt is another 7%, and 10% of its deals (at fair value) are in equity. The vast majority of its debt (94%) is floating-rate in nature, which is typical for many BDCs.

That has its upsides and downsides. In a normal rising-rate environment (think 2015-19, not 2022-23), rising rates are generally good for BDCs that work heavily with floating-rate debt. The potential for declining rates (or actually declining rates)? Not so good.

Also, as one might have guessed, TCPC has a connection to BlackRock (BLK)—specifically, it’s externally managed by an indirect, wholly owned subsidiary of BlackRock (BLK). This connection allows it to access BlackRock’s many resources, which in theory should make it a particularly competitive BDC.

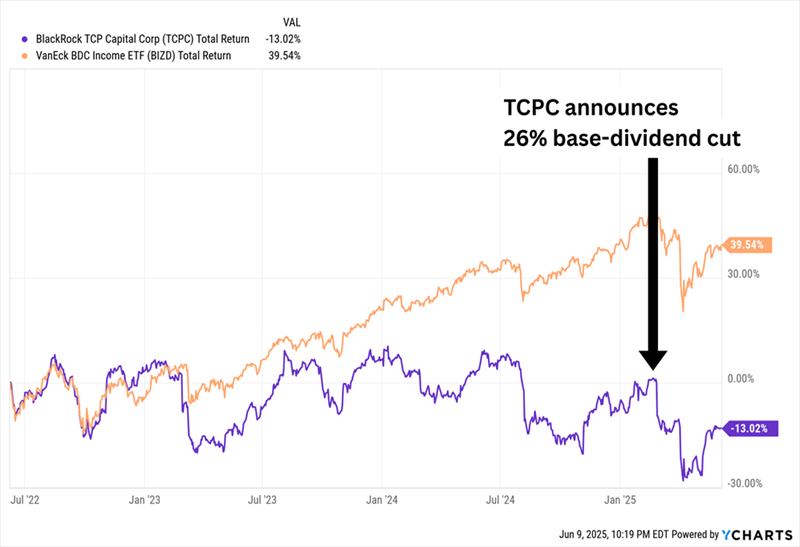

In Practice, TCPC Has Been a Straight-Up Dud

I warned in November 2024 that BlackRock TCPC keeping its base dividend flat for a fifth consecutive quarter raised “a little concern that TCPC’s dividend might be plateauing.” Three months later, the BDC pulled the rug out from under its investors with a drastic dividend cut. That’s despite a practice of pairing its base dividend with special dividends as profits allow.

BlackRock TCPC’s declines have opened up a generous 13% discount to NAV. And even with the reduced 25-cent-per-share base dividend (and an already announced 4-cent special dividend for Q1), the stock still yields a sky-high 13%.

But TCPC hasn’t exactly fixed what got it here. The dividend is more affordable, and the company’s adviser is waiving a third of its fee through Q3. But it’s still thick in non-accruals (loans that are delinquent for a prolonged period, usually 90 days), which even after improving this past quarter sit at an elevated 12.6% and 4.4% of the portfolio at cost and at fair value, respectively.

Crescent Capital BDC (CCAP)

Dividend Yield: 11.5%

Crescent Capital BDC (CCAP) is another BDC that’s paired with (and enjoys the resources of) a larger investment company. Crescent Capital BDC is tied to global credit investment firm Crescent Capital Group, which itself specializes in below-investment-grade credit strategies.

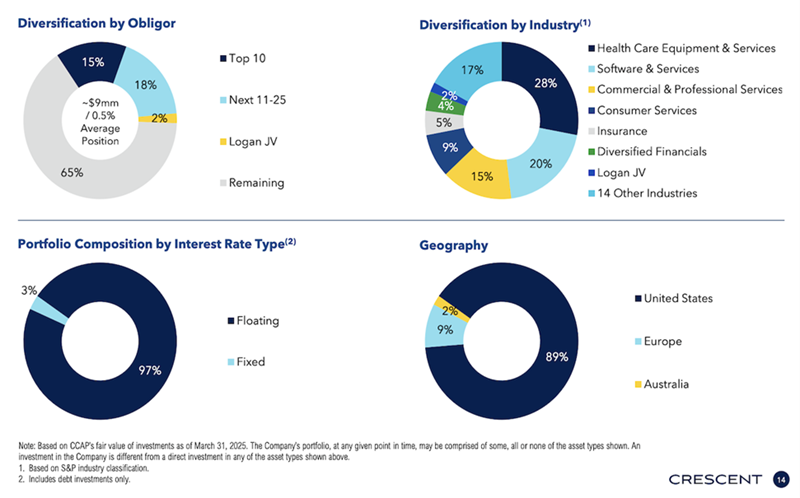

CCAP currently invests in 191 portfolio companies, with a penchant for private middle market companies. It’s predominantly U.S.-focused, though it does have 9% portfolio exposure to Europe and a thin 2% exposure to Australian companies. It’s similar to TCPC in that it primarily deals in first-lien debt (91%), and the vast majority (97%) is floating-rate in nature.

Source: Crescent Capital BDC Q1 2025 Investor Presentation

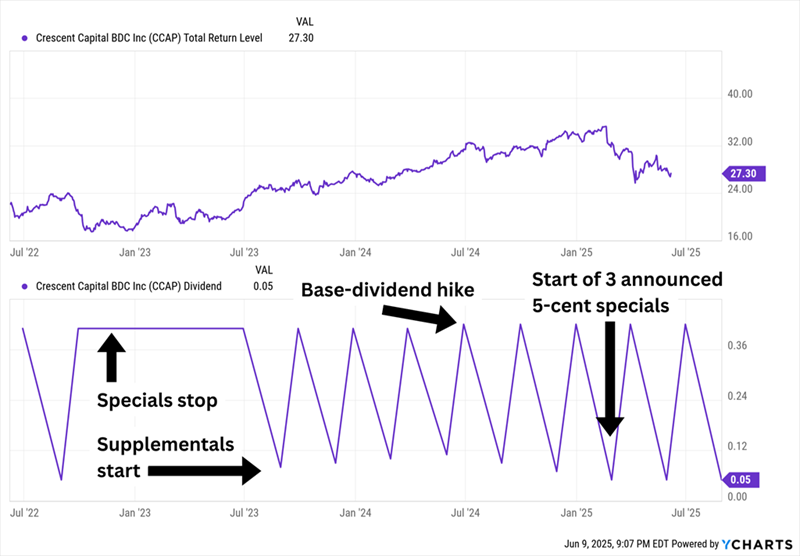

The last time I looked at CCAP, I mentioned that it has quite the oddball dividend history:

In March 2023, the company closed on its acquisition of First Eagle Alternative Capital (FCRD) at a hefty 66% premium … Admittedly, the deal forced CCAP to halt a run of 5-cent special dividends. Fortunately, not only have specials come back—they’ve gotten bigger. And perhaps even more telling—the company raised its regular dividend, albeit by a penny per share, for the first time in years. (It’s an odd special, too. Crescent Capital announces its special dividends after the fact; for instance, in August, it declared a Q3 base dividend of 42 cents per share, but also a 9-cent-per-share supplemental for the second quarter.)

I’m afraid the dividend picture hasn’t become any less complicated since then.

Crescent Capital has kept up with its 42-cent-per-share base dividend. But the action in its special dividends has changed. The variable supplemental dividends, which had been around for six quarters, disappeared at the start of this year. At the same time, CCAP announced 5-cent specials for the first, second, and third quarters—but they’re related to undistributed taxable income.

So while it looks like CCAP’s variable supplemental has just gotten a little smaller, in reality, it’s not paying any supplementals (or, at least, it hasn’t for the past two quarters).

There’s a Lot Going on Here

Those supplementals might not return for some time, either. Wall Street is increasingly worried about rate compression among BDCs, for one. CCAP itself, meanwhile, is running into increasing credit issues, a spate of new non-accruals, and the winding-down of the Logan joint venture, which was providing CCAP with some cash flows.

At least investors are being realistic about Crescent Capital’s dimming prospects of late, driving shares down to a wild 23% discount to NAV. This normally defensively positioned BDC hardly looks like the pinnacle of health right now, but a discount that deep (plus an 11% yield on the base dividend alone) could attract some bargain hunters.

PennantPark Floating Rate Capital (PFLT)

Dividend Yield: 11.8%

I’ll start with PennantPark Floating Rate Capital (PFLT), which targets midsized companies that are “profitable, growing and cash-flowing,” with a specific focus on firms that generate $10 million to $50 million in annual earnings before interest, taxes, depreciation and amortization (EBITDA).

Currently, PFLT’s portfolio is 190 companies wide, and those 190 companies are supported by roughly 110 private equity sponsors. And while some BDCs are happy to invest in a wide variety of companies, “value-added” BDCs that lend expertise tend to be more selective. In this case, PennantPark Floating Rate’s interests lie in five primary categories: health care, software and technology, consumer, business services and government services.

Most important, however, is what gives PennantPark Floating Rate Capital its name. While BDCs often deal with floating-rate first-lien debt, PFLT takes it to the max: About 90% of the portfolio is first-lien debt, virtually all of which is floating-rate in nature. (The remaining 10% is split 80/20 between equity co-investments and joint venture equity.)

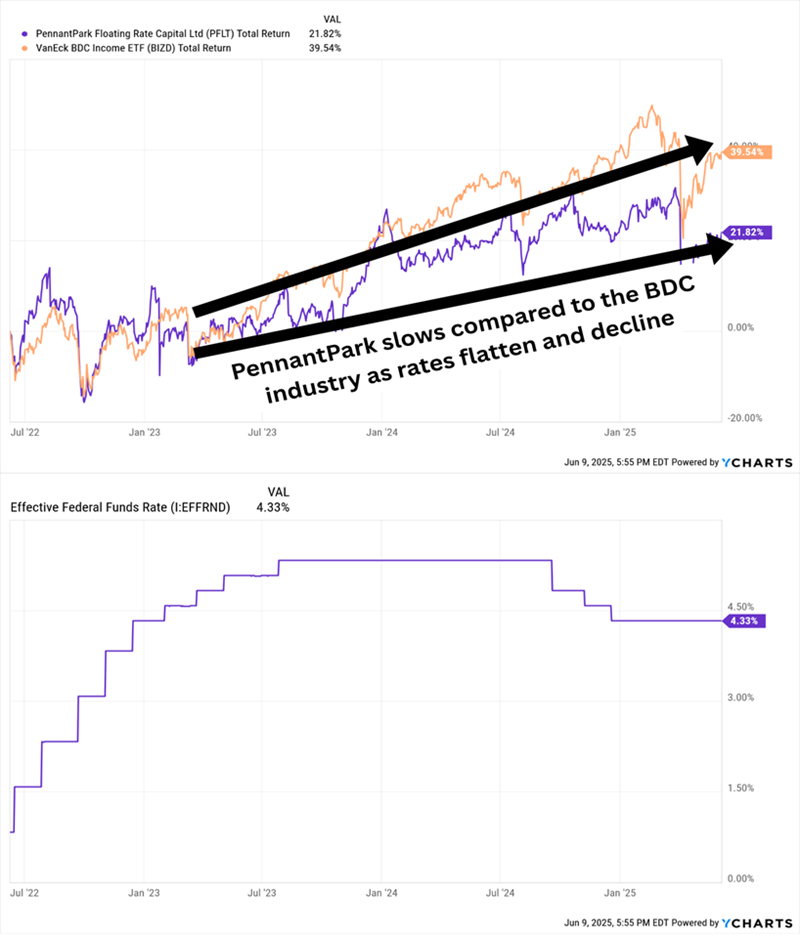

As I mentioned before, the Fed’s flattening and eventual reduction in interest rates took a toll on many BDCs.

But PennantPark Floating Rate Felt It More Than Most

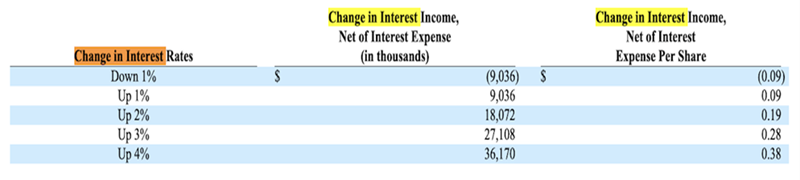

PFLT is, in fact, pretty open about what shrinking rates mean for its bottom line:

Source: PennantPark Floating Rate Capital Q2 2025 10-Q

PFLT trades at a 6% discount to NAV; that’s nice, but it almost feels like an optimistic valuation given the uncertainty facing the rate environment and PennantPark right now.

On the upside, PFLT is actually a monthly dividend payer, and a generous one, too, at nearly 12%.

On the downside, coverage of that dividend is getting awfully tight. In fiscal 2024 (its year ends in September), PFLT paid $1.23 per share on net interest income of $1.27 per share (a 97% NII payout ratio), generated from profits of $1.18 per share. It’s expected to earn $1.21 per share and $1.18 per share over the next two years, and we can reasonably expect NII to be proportional.

That’s OK (not great) if all goes well, but a lot hinges on what the Federal Reserve does next—an open question.

A Fully Paid Retirement for Just $500,000?

Monthly dividend schedules, like how PennantPark pays its investors, are a cornerstone of what I think makes an ultimate retirement income portfolio.

But at least for now, we can do better than PFLT’s tightly covered payout.

We don’t want dividends that are just frequently paid—we also need them to be consistently paid, so we need to make sure our high yields are well covered, too.

Just like the picks in my 8%+ Monthly Payer Portfolio.

My 8%+ Monthly Payer Portfolio is filled with the kinds of companies we need to live on dividends alone—without selling a single stock to generate extra cash.

This portfolio is capable of generating a $48,000 annual dividend “salary” from a $600,000 nest egg. And depending on where in the country you live, a $40,000 salary on a $500,000 nest egg could be enough for a fully paid retirement.

And if you’ve managed to stow away a cool million dollars to work with, the 8% Monthly Payer Portfolio would pay you a cool $80,000 in dividend income every year.

Better still? That money would find its way to you each and every month.

No “lumpy” payouts. No complex dividend calendars. No dumping money into certain stocks because you’re getting underpaid every third month.

Just paydays as smooth as when you were collecting a check from work!

Don’t miss out on these terrific income plays while you can still get in at a bargain. Click here for all the details, and to download a FREE Special Report revealing the names and tickers of all the stocks and funds in my 8% Monthly Payer Portfolio.

Before you make your next trade, you'll want to hear this.

MarketBeat keeps track of Wall Street's top-rated and best performing research analysts and the stocks they recommend to their clients on a daily basis.

Our team has identified the five stocks that top analysts are quietly whispering to their clients to buy now before the broader market catches on... and none of the big name stocks were on the list.

They believe these five stocks are the five best companies for investors to buy now...

See The Five Stocks Here

Nuclear energy stocks are roaring. It's the hottest energy sector of the year. Cameco Corp, Paladin Energy, and BWX Technologies were all up more than 40% in 2024. The biggest market moves could still be ahead of us, and there are seven nuclear energy stocks that could rise much higher in the next several months. To unlock these tickers, enter your email address below.

Get This Free Report