Are we careening towards a recession, or is a pickup in inflation the big threat to the stock market?

The negative first quarter GDP print has recession fears in the financial headlines. Meanwhile, Fed Chair Jay Powell remains fixated on inflation.

Ironically, both may come to pass. Which means we must prepare our portfolios for a slowdown that is quickly followed by a pickup in prices.

Let’s put one smart lender on our “Goldilocks” watch list. This ticker yields 10% today (with some nice “dividend insurance” we’ll talk about in a moment). But the key point is that it profits as inflation—and interest rates—tick higher.

Let’s talk about the “slowdown-inflation two-step” I see coming—and how it’s set to open the door on this 10% dividend opportunity.

Slowdown Now …

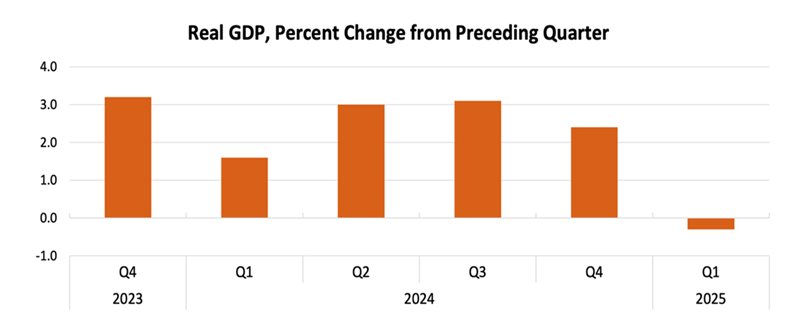

Let’s start with the slowdown, which, as we discussed last week, is already upon us. The evidence: A 0.3% decline in first-quarter GDP:

Source: Bureau of Economic Analysis

But the underlying numbers were actually more bullish than the headlines suggested.

That’s because the pullback was in large part due to a spike in imports as retailers stocked up ahead of Trump’s tariffs—and imports are calculated as a drag on GDP. That trend is likely to fade. Government spending also fell in light of DOGE cuts (though as we’ll discuss next, this will likely be fleeting), while consumer spending largely held up.

We’ll happily take a GDP dip caused by temporary factors! But a slowdown is still likely. There were hints of this in the April employment report, which, while better than expected, still showed a slight slowdown from March.

… Inflation Next

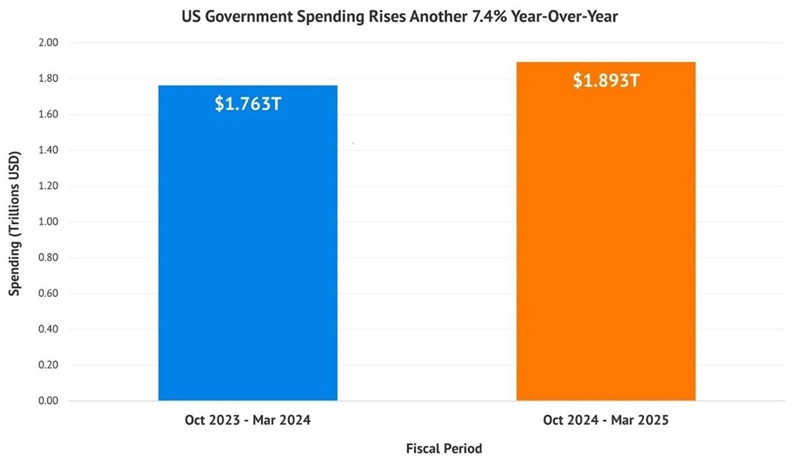

Meantime, despite DOGE’s efforts, government spending rose 7.4% year-over-year for the first six months of this fiscal year (which began October 1, 2024).

Tax receipts, by the way, are not up 7.4%. And remember that most of federal spending is untouchable: Messing with Social Security, Medicare or Medicaid is political suicide. Defense spending seems “secure” given the current state of the world.

That makes it far more likely that a future Fed Chair (remember that Jay Powell’s term is up in a year) will resort to money printing quantitative easing (and with it, sustained, or rising, inflation and rates in the longer term).

Enter Our 10%-Paying “Floating-Rate” Lender

Enter commercial mortgage real estate investment trusts (mREITs), which stand to see higher income from their floating-rate loans as inflation—and interest rates—hold at current levels or tick up.

When most people think of REITs, they think of those that own physical properties, like shopping malls, hotels and apartments. Instead, mREITs buy and originate mortgages on these properties. (But like their property-owning cousins, they get a hall pass on their corporate taxes so long as they pay out 90% of their income as dividends.)

mREITs’ lending operations make money by borrowing at low short-term rates, then lending that cash out in the form of mortgages based on long-term rates. They then pocket the difference.

This business model prints money when long rates (i.e., those on the 10-year Treasury) are steady or, better yet, declining, as we’ll likely see in the coming slowdown. That’s because, when long-term rates drop, mREITs’ existing loans become more valuable because new loans pay less. That’s the setup we’re likely to see in the coming months.

But what about when rates rise? That can hurt mREITs because their existing mortgage portfolios fall in value. But remember that they do see rising income from those floating-rate loans.

Moreover, the best mREITs are run by experienced managers and have their hands in businesses beyond commercial lending, helping them navigate any rate environment.

Starwood: Much More Than a Mortgage Lender

Which sets up the 10%-yielding stock we’re going to talk about today: Starwood Property Trust (STWD). It really is the poster child for mREITs. For starters, its loan book is 98% floating-rate. And as we’ll see below, it’s diversified into other businesses that help hedge it against inflation.

Starwood is managed by Barry Sternlicht’s Starwood Capital, which he founded with $20 million in 1991. Today, Starwood Capital manages over $120 billion in assets.

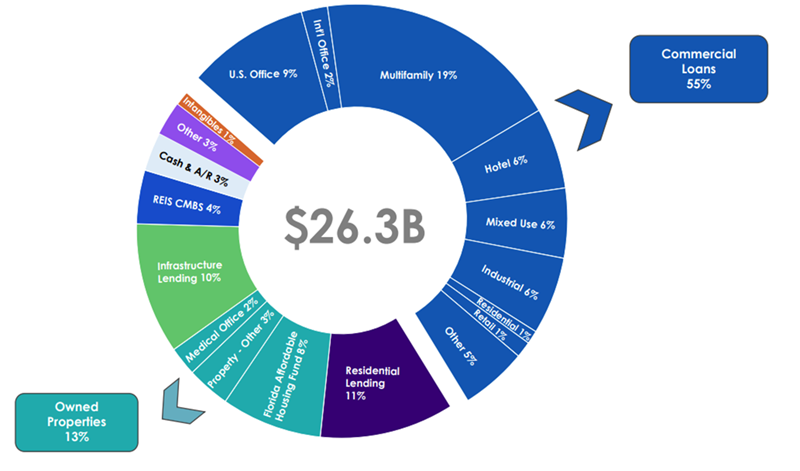

These folks know the credit and real estate markets, and they’ve built STWD to thrive in all rate setups: Beyond commercial lending, which is about 55% of assets, STWD holds residential loans (11%) and devotes about 13% of its assets to owned properties.

It also makes loans in the growing infrastructure space (a keen focus of the company) and originates, acquires and manages mortgage-backed securities. In addition, it runs LNR Partners LLC, which focuses on resolving distressed mortgages. Since its launch in 1993, LNR has resolved some $94.5 billion worth of such loans.

On the commercial loan side, the company’s loan book is as diverse as they come, with mortgages spread across office, housing, hotel, industrial, infrastructure, mixed-use properties, international properties and more.

Source: Starwood Property Trust Q1 investor presentation

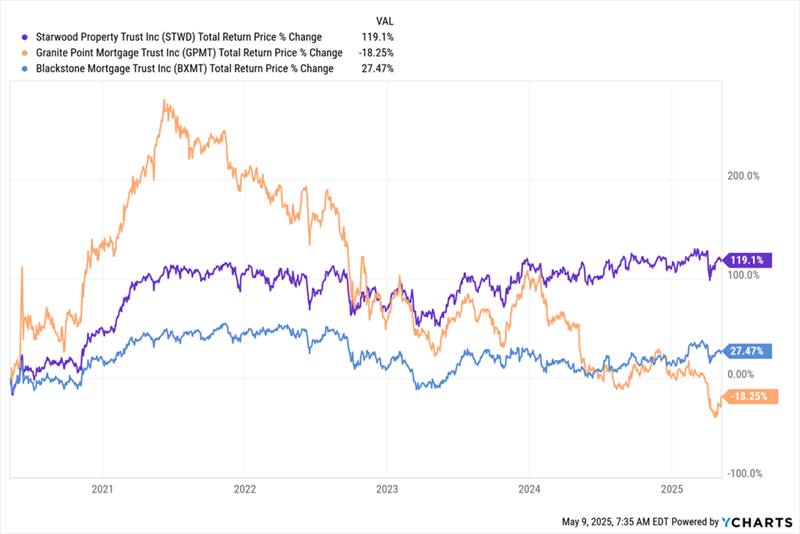

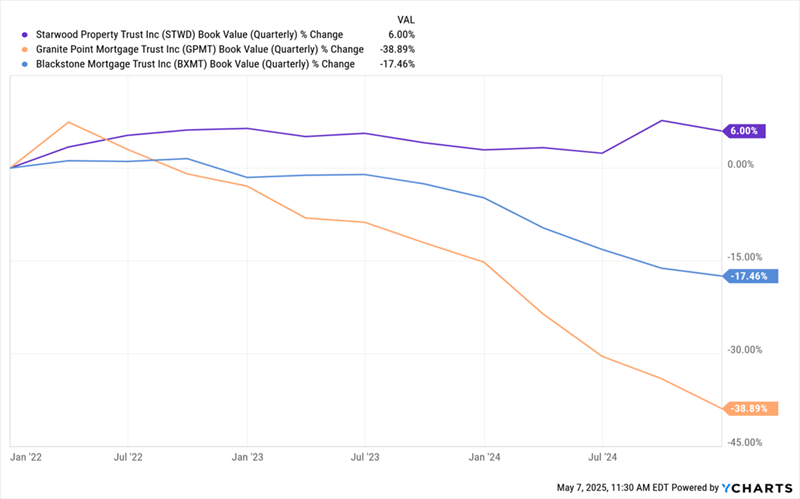

All of this has helped this “ironclad” mREIT blow past competitors Blackstone Realty Trust (BXMT) and Granite Point Mortgage Trust (GPMT) in the past five years—through COVID, plunging rates, rising rates and the trade war—and with far less drama, too:

Starwood Soldiers Through the Wild 2020s

That share-price gain is deserved. Just look at how STWD’s book value grew from the start of the rising-rate period, in January 2022, to the end of 2024—when 10-year Treasury rates shot up from 1.5% to 4.6%. At the same time, the book values of BXMT and GPMT plummeted:

Starwood Shakes Off Rising Rates, Grows Its Assets

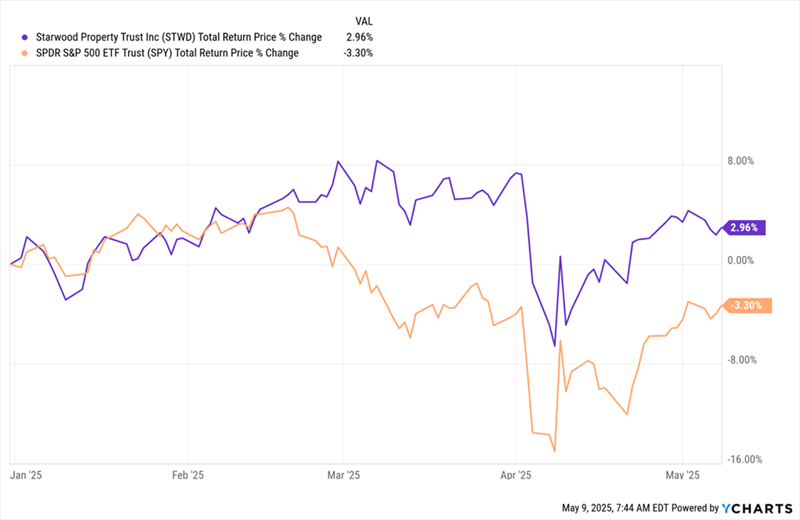

And this year? Despite concerns about inflation/recession, Starwood has posted a total return of roughly 3% and has only barely slipped into the red this year, while the S&P 500’s total return remains underwater, with volatility that’s gone through the roof:

“Tariff Tantrum” Fails to Dent Starwood

On the dividend front, Starwood raised the payout after its 2009 IPO and has held it steady, at $0.48 quarterly, for the past decade. And that payout looks safe: Management says it has $1.5 billion (or $4.53 a share) in unrealized distributable earnings from property gains to put toward the payout.

That’s nearly 2.5 years of payouts, based on the current annualized rate.

Slowdown Could Give Us a Better Deal on Starwood

So why are we putting Starwood on our watch list and not our buy list, now? It goes back to book value: Right now, Starwood trades “at book,” which isn’t bad—but I expect a slowdown to pull the stock below book by a bit. That’s what happened in March 2023, when the collapse of Silicon Valley Bank and friends sent recession fears soaring.

Back then, STWD traded at 82% of book. And with another slowdown likely, I expect another chance to buy for less than book value in the coming months (though likely not quite at that 18%-off deal we saw in 2023!).

When that opportunity appears, I’ll tip off members of my Contrarian Income Report service in our regular monthly issue.

Put Starwood on Your Watch List—But Snap Up This Cheap 11% Payer NOW

While we’re waiting on Starwood, we’re buying another investment—a closed-end fund (CEF) that’s kicking off a huge 11% dividend (paid monthly!) right now.

This off-the-radar corporate-bond fund shares two key things with Starwood:

- A huge dividend—11%!

- A top-flight manager. This fund will “see” Starwood’s Sternlicht and “raise” with its own savant, who’s crushed the corporate-bond benchmark by nearly 3X over the long run.

But there is one key difference here—and it’s why we’re waiting on Starwood now, while we BUY this 11% (monthly) payer with both hands:

- A big—and highly unusual—discount in disguise!

As rates fall and other income options wane, I expect this 11% payer’s discount/dividend combo to be a shiny lure for the mainstream crowd. And we have a shot at “front-running” them today.

Don’t miss this opportunity. Click here and I’ll tell you all about this incredible 11%-paying fund and how to get your FREE Special Report revealing the name, ticker and my detailed research.

Before you make your next trade, you'll want to hear this.

MarketBeat keeps track of Wall Street's top-rated and best performing research analysts and the stocks they recommend to their clients on a daily basis.

Our team has identified the five stocks that top analysts are quietly whispering to their clients to buy now before the broader market catches on... and none of the big name stocks were on the list.

They believe these five stocks are the five best companies for investors to buy now...

See The Five Stocks Here

Enter your email address and we'll send you MarketBeat's list of seven stocks and why their long-term outlooks are very promising.

Get This Free Report