As I’m sure you have heard, Moody’s downgraded US debt last weekend.

The stock market panic that ensued lasted for, oh, about an hour of trading.

Why did this already get shrugged off? It’s a classic empty-calorie headline. The practical impact of the downgrade to top holders of Treasuries—banks and pension funds—is nil.

Treasuries are still classified as top-grade collateral, which means banks can continue to leverage these securities. T-bills are just as good as cash for bank reserves, as they were before the downgrade. No need to scramble for new collateral.

And Treasuries still have investment-grade status, which means pension funds don’t have to make any moves. Current asset allocations are just fine. It is “business as usual” at major financial institutions after the dramatic downgrade news.

Of course, the federal deficit is humungous and unlikely to ever be paid back. In real terms, that is. Nominally, the repayment will happen. An important distinction! Creditors will ultimately receive depreciated dollars due to inflation.

In other words, the $36 trillion owed to Treasury bond holders likely gets repaid in nominal (the actual number that includes inflation) versus real (inflation adjusted) terms. So creditors will receive the number of dollars borrowed plus interest, but those will be depreciated dollars—bucks themselves that due to inflation will be worth less than today.

Which means the key to successful retirement investing will be diversifying away from US dollars and into “hard asset” plays. We’ll discuss two today that will appreciate as the dollar declines. One yields 8.6%!

Why is the debt and path of the dollar an issue now when we’ve been on this debtor path as a country through many administrations for decades? Because we are teetering on the debt tipping point. The Social Security trust fund is projected to go negative by 2030, which will force the government to draw from general revenues.

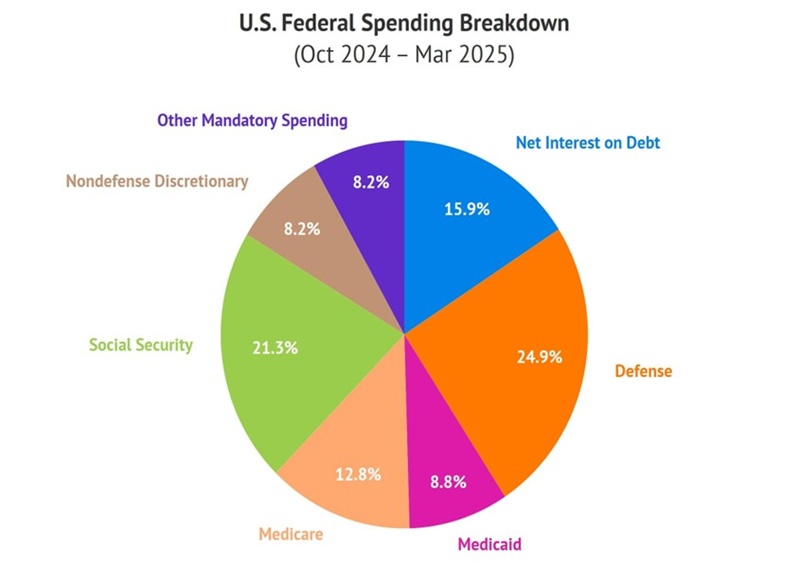

Think DOGE is going to save the day? No. Most of the federal spending is untouchable. Messing with Social Security, Medicare or Medicaid is political suicide. Same with “other mandatory spending”—these are benefits that have been promised. Voters won’t have it any other way. And older people who receive Social Security and Medicare? They vote at the highest rate of any age group.

The net interest on our debt continues to climb. Defense spending seems “secure” given the current state of the world. Which leaves the modest nondefense discretionary slice, just 8.2% of the federal spending pie for DOGE to slice from:

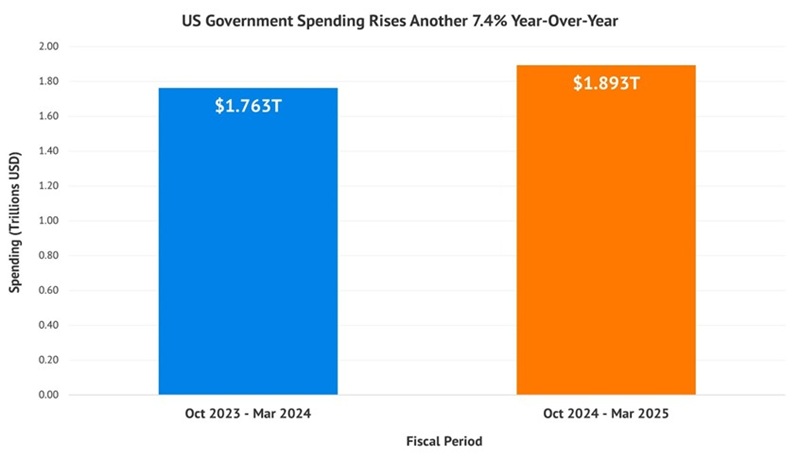

With such a small austerity target, it’s no wonder that government spending is up 7.4% year-over-year for the first six months of this fiscal year (which began October 1, 2024):

Tax receipts, however, are not up 7.4%. These “revenues” are only up 3%. The US has a highly-indebted balance sheet with expenses growing faster than sales—not good.

If austerity via DOGE is not happening, then what is the alternative? Money printing. Jay Powell’s term is up one year from now. Trump will appoint a friendly face such as Kevin Warsh, Kevin Hassett or Judy Shelton who will work with the administration to (ahem) paper over some of these debt issues.

And by the way, Powell may be insistent on “higher for longer” rates, but he is not acting hawkish across the board. In fact, the market saw right through his “all bark, no bite” rhetoric at the last Fed meeting because his recent actions have spoken louder than his words.

If you’re wondering who is buying Treasuries at 4-some-percent in today’s environment, the answer should be no surprise—the Fed. Yup. Powell & Co. recently “stepped up” their buying an extra $20 billion per month!

With the Fed the new “whale” at the table, foreigners are (believe it or not) once again scrambling to buy Uncle Sam’s bonds. They briefly paused in tariff-laden April but have returned in a big way in May. We saw robust demand at the May 6 auction, with foreign investors buying 71.2% of the $42 billion in 10-year Treasury notes (up from an average of 67.6%).

It takes a village to keep the Treasury yield down! And all hands are on deck. The Fed increasingly supports the Treasury market. Don’t listen to the naysayers who claim the Moody’s downgrade is going to crush the bond market—the administration, Treasury, and Fed are working together to keep the lid on bonds.

The US runs the world’s printing press, and Uncle Sam is using it to buy more of his own debt. This is why gold has glittered year to date, and why the yellow relic’s move higher is likely to continue.

Gold miners themselves have retreated modestly from mid-April levels. VanEck Gold Miners ETF (GDX) sits 8% off its recent all-time highs and is likely to bottom.

The fundamental backdrop for yellow metal miners couldn’t be better. Gold prices are high and oil prices are low—which means maximum profit margins.

That’s why we like GDX even though it yields a mere 1%. Its real potential lies in its price appreciation. While GDX is up 37% year-to-date—even after its recent pullback—investors will realize the only “way out” for the federal government is monetary inflation and they will drive up the price of gold even more.

Let’s close with a discounted way to invest in gold. GAMCO Global Gold, Natural Resources & Income Trust (GGN) is a closed-end fund trading at a 3% discount to net asset value (NAV) as I write. GGN’s “97 cents on the dollar” price tag is attractive.

About half of the fund’s portfolio sits in mining stocks—both gold and non-gold plays like iron miner Rio Tinto (RIO). The miners-at-large have some great earnings reports ahead of them thanks to low energy prices because oil, a key input cost for mining operations, is down 27% year-over-year.

This underfollowed, misunderstood fund should continue to grind higher as the government papers over its pile of debt. GGN will pay us 3 cents per month, every month, as our slow-motion monetary train crash unfolds. And that’s good for 8.6% per year.

With funds like GGN it is possible to retire on as little as $500K.

But we retirees and retirement-hopefuls must be careful with monetary inflation ahead!

A $500K nest egg is either growing or shrinking. With funds like GGN, our capital will grow as our portfolio pays us 8.6%—which is $43,000 per year on $500,000.

It is possible to bank tens of thousands of dollars in yearly dividend cash for every $500,000 invested. With inflation-protected principal, to boot! Let’s talk about how to live off $500K… practically forever.

Before you make your next trade, you'll want to hear this.

MarketBeat keeps track of Wall Street's top-rated and best performing research analysts and the stocks they recommend to their clients on a daily basis.

Our team has identified the five stocks that top analysts are quietly whispering to their clients to buy now before the broader market catches on... and none of the big name stocks were on the list.

They believe these five stocks are the five best companies for investors to buy now...

See The Five Stocks Here

Enter your email address and we'll send you MarketBeat's list of ten stocks that are set to soar in Fall 2025, despite the threat of tariffs and other economic uncertainty. These ten stocks are incredibly resilient and are likely to thrive in any economic environment.

Get This Free Report