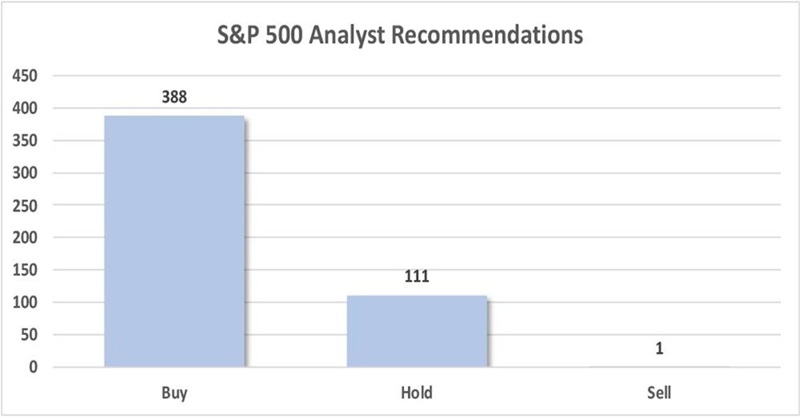

Wall Street analysts have “Buy” ratings on 388 stocks in the S&P 500. That’s over 76% of the index!

Thank you, suits, for the curation. No, seriously. We contrarians are going to comb through the Holds and, even, the lone Sell:

Analysts Rate Most Stocks as “Buys”

Source: S&P Global Market Intelligence

Analyst optimism is the norm. Analysts need access, companies provide them with access. One hand washes the other, thus it is rare to see unfavorable ratings on stocks.

The problem with a Buy rating is that there is nobody left to upgrade the stock. Every delta is a downgrade.

Contrast this with the Holds and Sells—it can only get better from here! The only analyst move is an upgrade. So why not “front run” these upcoming bandwagon calls?

Let’s look at four disliked stocks yielding between 6.6% and 16.5%. These big payers aren’t receiving any love from the suits—which is often a perfect time to buy.

National Storage Affiliates Trust (NSA)

Dividend Yield: 6.6%

National Storage Affiliates Trust (NSA) is a self-storage real estate investment trust (REIT) with 1,075 self-storage properties in 41 states and Puerto Rico.

Self-storage is generally recession-resistant. In good times, people accumulate stuff, and that stuff has to go somewhere, and that somewhere is storage units. In bad times, consumers don’t want to get rid of all their stuff, even if they must downsize. So, they pile belongings into storage units.

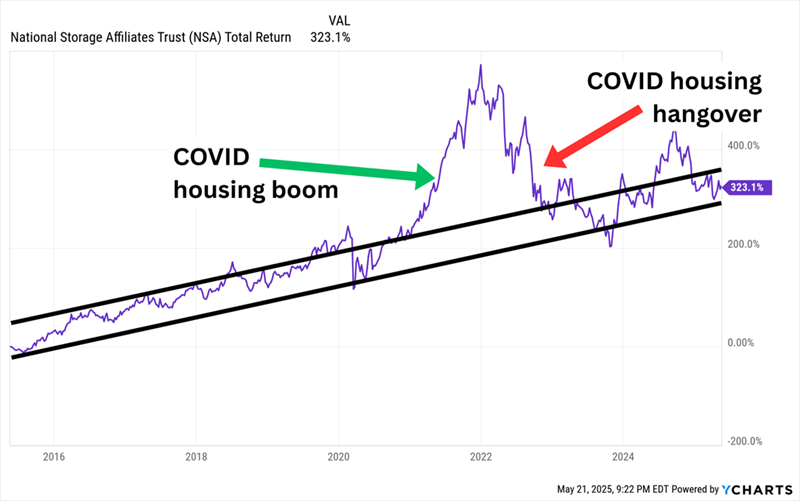

Now self-storage itself has boom-and-bust cycles. We just saw this during the COVID-era housing explosion and subsequent dry spell.

NSA Shakes Off the Housing Hangover

NSA has historically been a competent operator. It handled the self-storage downturn admirably; move-in rates are significantly improving, and “street rates” (the prices a customer would see if they walked into a facility off the street) are headed considerably higher.

Wall Street’s dour consensus is not surprising (just one Buy vs. 10 Holds and four Sells). Vital metrics like same-store net operating income (SSNOI) and funds from operations (FFO) growth have trailed peers of late. And while the 6%+ yield is better than what we can get from most self-storage names, NSA’s payout represents 97% of its own 2025 FFO estimates. That’s very tight coverage.

NSA might be a more enticing bet at a better price. But the stock trades at roughly 15 times those estimates—fair, but hardly a deal right now.

CNA Financial (CNA)

Dividend Yield: 8.1%

CNA Financial (CNA) is one of the largest commercial property and casualty (P&C) insurers in the U.S. It’s also an oddball—it’s technically publicly traded, but 90% of the company belongs to conglomerate Loews (L).

Nonetheless, we can still buy a piece, and that piece will earn us a fat 8%+.

Though maybe not in as smooth a fashion as we’d like.

CNA is an increasingly common variety of company that pays both regular dividends and regular special dividends. In CNA’s case, it pays a (rising) regular dividend that’s currently at 46 cents per share, which is good for 3.9% in yield right now. It has also paid a special dividend in March each year for the past decade; 2025’s two bucks per share added another 4.2%.

Investors focused on retirement income can’t wait around on “lumpy” distributions like that—consistent payouts are a must, and monthly dividends are ideal. But it’s still a great dividend for anyone not relying on their IRA yet.

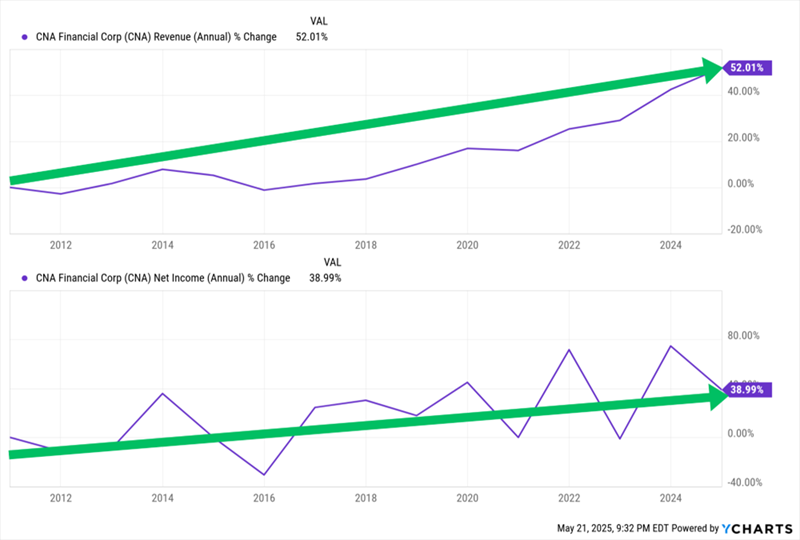

It’s also a responsible payout system. A base-plus-special format allows companies to pay big when they can, and to hang on to cash when they can’t, all while providing some sort of baseline income for shareholders. And that’s a godsend for insurers, where profits are inconsistent even among the best operators. Consider that CNA, which is a high-quality P&C firm, hasn’t enjoyed two consecutive years of profit growth since 2016-17.

So for insurers, we just want to see the arrow pointed in the right direction. And in CNA’s case, it has been for a long time.

Ignore the Noise: The Trends Are Still Our Friend

CNA Financial has a bearish consensus rating, but in fact, there is no bearish consensus—just a lone bearish wolf. CNA has one covering analyst, and that analyst says the stock is a Sell. Sometimes, a lack of analysts can be a negative statement in and of itself; the pros sometimes drop coverage because they’d rather stop covering a company rather than call it a dud.

But in some cases, analyst firms are just tightening up coverage amid scarcer resources that they want to allocate to spicier businesses than, say, insurance, and I think that’s the case with CNA.

Cricut (CRCT)

Dividend Yield: 15.5%

If the name Cricut (CRCT) doesn’t ring a bell, talk to someone who shops at Michaels or Jo-Ann Fabrics. The company’s namesake machines let users turn their ideas into professional-looking handmade goods: mugs, cards, T-shirts, even large-scale interior decorations.

Cricut also calls itself a “creativity platform.” It has software that integrates its machines with design apps (including its own Cricut Joy App), and a pair of subscription plans that offer additional fonts, images and more.

And believe it or not, this is a truly global name spanning six continents. (Sorry, Antarctica.)

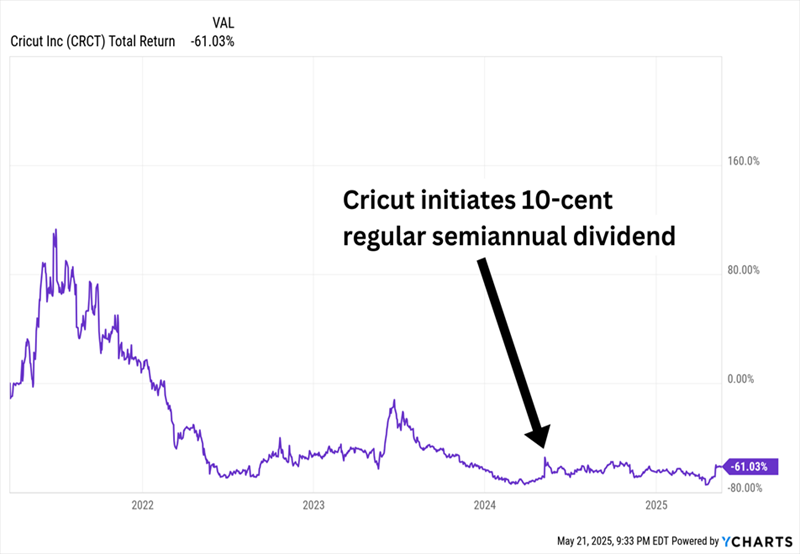

I featured this stock last year when I examined some fresh-faced dividends. In May 2024, in the midst of a multiyear collapse in its top and bottom lines, it shocked some investors by both announcing a substantial 40-cent-per-share special dividend, and initiating a 10-cent regular semiannual dividend.

New Dividends Often Reflect Growth (But Apparently Not Always)

It followed that up by continuing the regulars this year and announcing a 75-cent special, payable in July.

While that combined payout is several times bigger than expected adjusted earnings this year, CRCT does have the cash flows to manage it.

But the confidence management is projecting with these dividends seems to smack in the face of what Circuit is facing. While CRCT managed to finally stem the bleeding and grow the bottom line last year, demand and engagement trends are still pointed in the wrong direction (revenues actually sagged another 7% in 2024), and promotional spending remains high. Moreover, profits are expected to decline in each of the next two years, and tariffs could further weigh on the company, which relies heavily on international manufacturing, especially in southeast Asia.

The pros are negative—CRCT has three Sell calls and a Hold right now—and I’m inclined to agree. A whopper of a dividend aside, there’s little to suggest a change in Cricut’s growth prospects is on the horizon.

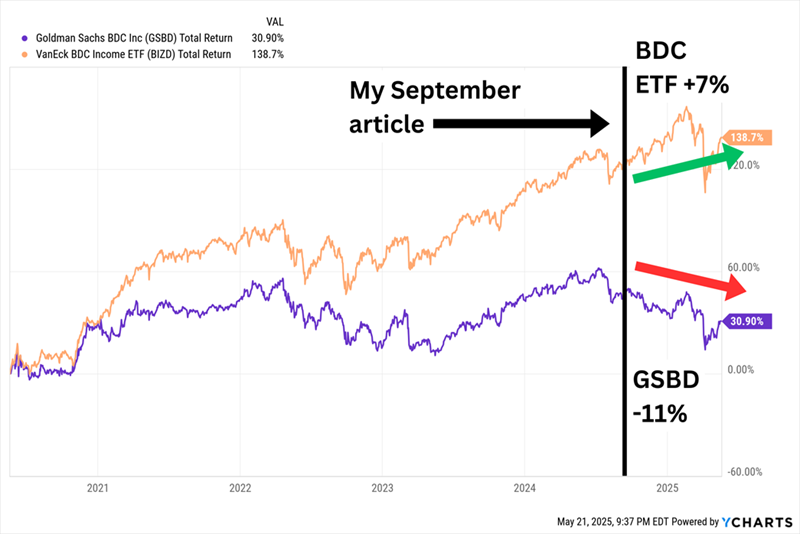

Goldman Sachs BDC (GSBD)

Dividend Yield: 16.5%

Goldman Sachs BDC (GSBD) is a business development company (BDC) that targets companies bringing in between $5 million and $75 million in annual EBITDA (earnings before interest, taxes, depreciation and amortization). Its typical investment ranges between $25 million and $75 million, and it deals almost exclusively in debt.

I singled out Goldman Sachs BDC back in September for its hated status, and that hasn’t changed, with analysts issuing three Holds, one Sell, and a couple of No Opinions (they’ll provide earnings and other financial estimates but won’t make a call on the stock).

Investors are naturally drawn to this BDC for an obvious reason: the connection to Goldman Sachs (GS). GSBD isn’t shy about this, saying that management may “draw upon the vast resources of Goldman Sachs to assist in the evaluation of potential investment opportunities.”

But as I said in September:

“Unfortunately, [GSBD’s] dividend hasn’t budged since the company went public roughly a decade ago. And despite GSBD’s ‘vast resources,’ the company has underperformed the BDC industry for years.”

That’s also still the case—indeed, Goldman Sachs BDC has only continued to underperform.

So Much for Goldman’s Expertise

In fact, quality issues—namely high non-accruals (loans that are delinquent for a prolonged period, usually 90 days) and dropping net investment income (NII)—finally forced Goldman Sachs BDC to cut its regular dividend by nearly 30% in February.

Bizarrely, Goldman Sachs is now paying out more than it used to. At least for the moment.

GSBD cut its regular dividend from 45 cents per share to 32 cents, starting in Q1. But at the same time, it also announced 16-cent special dividends for Q1, Q2, and Q3—effectively 48 cents per share in each of those three quarters. On top of that, in May, it announced an additional 5-cent supplemental dividend, bringing the total payout for Q2 to 53 cents per share.

Maybe Goldman just bought itself some optionality. And heck, GSBD isn’t all warts. The BDC says just four of its 163 portfolio companies should be affected by tariffs, the stock trades at a healthy 17% discount to NAV right now, and based on all the dividends promised for 2025 (four 32-cent regulars, three 16-cent specials, and the 5-cent Q2 supplemental), it yields a mouth-watering 16.5%—with the potential for more if it issues a Q4 special or any additional supplementals.

This 11% Dividend Is an URGENT Trump 2.0 Buy

If we’re investing our hard-earned money in hopes of enjoying growth and generating retirement income for years to come, we want to do so in companies that actually have solid track records of providing both.

But while we’re not touching GSBD right now, we’re not sitting on our hands, either.

Right now, we’re buying another investment—a closed-end fund (CEF) that kicks off both of our checkboxes in a major way:

- A huge dividend—11%–paid monthly

- A big—and highly unusual—discount in disguise!

This isn’t some vanilla index fund. This CEF is actively run by a manager who’s at the top of the bond world. He has been named Fixed Income Manager of the Year by Morningstar, and he has been inducted into the Fixed Income Analysts Society Hall of Fame!

As rates fall and other income options wane, I expect this 11% payer’s discount/dividend combo to be a shiny lure for the mainstream crowd. And we have a shot at “front-running” them today.

Don’t miss this opportunity. Click here and I’ll tell more about this incredible 11%-paying fund and how to get your FREE Special Report with all of my detailed research.

Before you make your next trade, you'll want to hear this.

MarketBeat keeps track of Wall Street's top-rated and best performing research analysts and the stocks they recommend to their clients on a daily basis.

Our team has identified the five stocks that top analysts are quietly whispering to their clients to buy now before the broader market catches on... and none of the big name stocks were on the list.

They believe these five stocks are the five best companies for investors to buy now...

See The Five Stocks Here

With the proliferation of data centers and electric vehicles, the electric grid will only get more strained. Download this report to learn how energy stocks can play a role in your portfolio as the global demand for energy continues to grow.

Get This Free Report