Vanilla investors fixate on price. We contrarians know better.

It’s all about the NAV. Net asset value, baby.

Price is what people pay at a given moment. But people panic. Many like to buy high—and sell low!

NAV, on the other hand, is what something is worth at that same moment. Price and NAV can become disconnected, especially during emotional market moments. When this happens, it is often a buying opportunity for careful contrarians like us.

Let’s take a pop quiz. Think about the funds you hold in your portfolio. What was your top performing NAV for the month of April?

I’ll share mine, with respect to our Contrarian Income Report portfolio. FS Credit Opportunities (FSCO) wins the top award for CIR with an unwavering NAV during April, the most volatile month since March 2020!

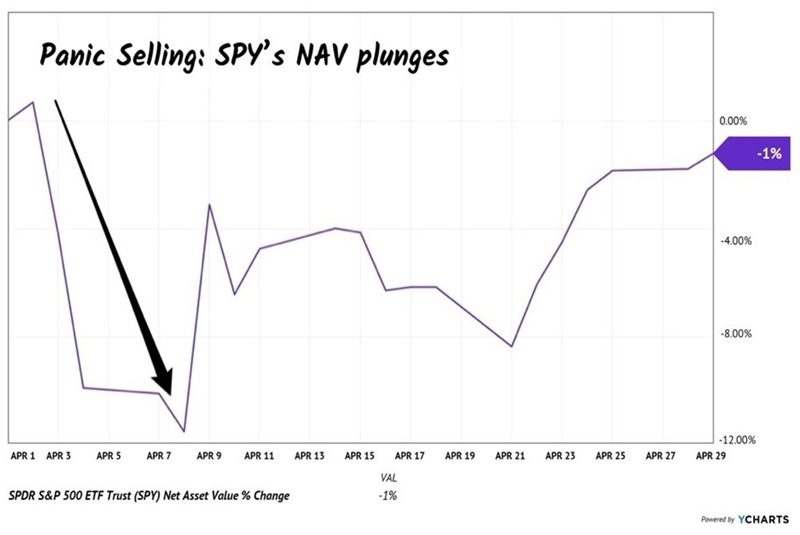

Dark it was. April 2025 began with a 12% drawdown in the S&P 500. “America’s ticker”—the SPDR S&P 500 ETF Trust (SPY)—took a licking! SPY’s NAV fell by an equal amount as its price—nearly 12% in 8 days—because investors dumped shares in the 503 stocks it owns. SPY’s NAV is “marked to market” constantly as its underlying shares trade.

This is the drawback of an NAV that is attached to other publicly traded positions. If the contents of the basket plummet in a panic, so does the fund’s NAV wrapper:

SPY’s NAV Plummets in April’s Panic

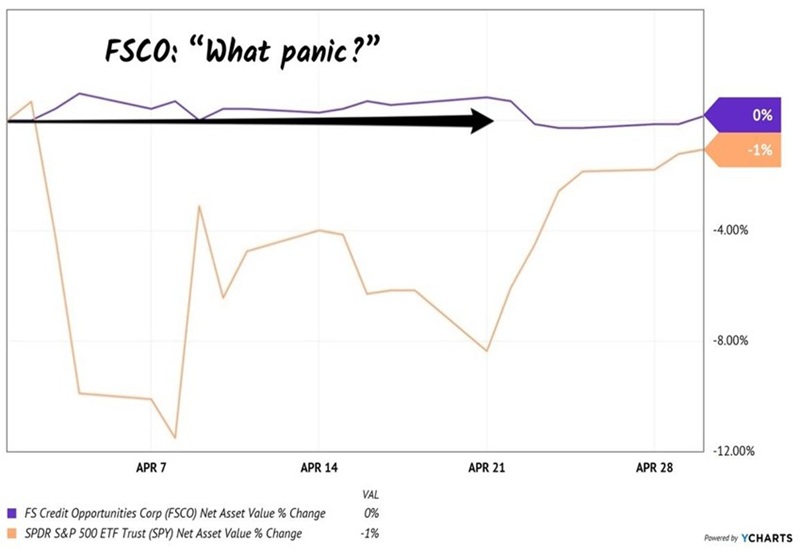

FSCO does not have this problem because its investments are in the calculated, relatively calm private markets rather than the manic, often-panicking public. The team extends private market loans, where FS can dictate favorable terms that secure its NAV.

Think of FSCO as a BDC (business development company) in a CEF wrapper. But it’s better than most BDCs. FSCO uses lower leverage and has a lower cost structure than the sector-at-large. Case in point, VanEck BDC Income ETF (BIZD) saw its NAV drop nearly 14% in the first eight days of April!

But while SPY and BIZD were in NAV freefalls, FSCO’s portfolio held up incredibly well. It didn’t budge!

FSCO’s NAV Unmoved in April’s Panic

With such an impressive pedigree, you might guess that FSCO trades at a premium to its NAV because every income investor on the planet would want in. The fund pays an 11% payout in monthly installments, and its NAV never moves. What’s not to like?

Amazingly, though, FSCO has traded at a discount since we first covered it here at Contrarian Outlook. In fact, when we added it to our Contrarian Income Report portfolio in October, it offered a 10% discount. Which meant this fine fund was a first-class find—available for just 90 cents on the dollar!

Why? The fund has been around for 10+ years but only traded publicly as a closed-end fund for the last two. CEF investors loathe newness. We want proof the income will last.

So. I called Josh Blum, Head of Investor Relations for FS Global Credit, to discuss. How is this incredible performance even possible during the most volatile month in recent memory?

“The NAV resilience reflects the focus on senior secured and structured credit strategies, which tend to exhibit lower correlation to the broader equity market movements,” Josh explained to me.

Portfolio manager Andrew Beckman and his team are skilled at “layering” credit, or structuring loans with different levels of protection, so that FSCO is positioned to get paid back first even if credit conditions worsen. Josh went on to explain that Beckman also deploys hedges from time to time to smooth out volatility.

“Strong underwriting fundamentals and limited mark-to-market exposure further supported the NAV stability,” Josh continued. His key point here is that FSCO is extending high-quality loans that are not subject to the daily whims of the public markets. These are private credit vehicles held by sophisticated investors who don’t care if the S&P 500 is down on a given day—they want their yield!

As do we income investors. Since we added FSCO to our Contrarian Income Report portfolio in October, this fund has been a rock with no NAV movement. This has not limited our gains, though! We have enjoyed total returns of 13.1% thanks to monthly dividends and price gains from FSCO’s shrinking discount window. These returns annualize to a terrific 23.4%.

FSCO Since October Add to CIR Portfolio

All looks great in the rearview mirror! But I wanted to know how conditions “on the ground” are looking to FS Credit today. Josh elaborated:

“We remain cautious credit pickers looking for value-based opportunities. Private credit remains a very large focus, but if public markets become dislocated due to tariff-driven volatility, we will migrate to that opportunity set from time to time.”

For us income investors, FSCO is a fantastic opportunity.

With funds like FSCO, we can turn our portfolios into monthly income machines. The darling discount we bagged buying FSCO last October has virtually vanished. Fortunately, there are other underappreciated monthly payers with 8%+ annual yields and 10%+ upside from current levels—like these.

Before you make your next trade, you'll want to hear this.

MarketBeat keeps track of Wall Street's top-rated and best performing research analysts and the stocks they recommend to their clients on a daily basis.

Our team has identified the five stocks that top analysts are quietly whispering to their clients to buy now before the broader market catches on... and none of the big name stocks were on the list.

They believe these five stocks are the five best companies for investors to buy now...

See The Five Stocks Here

Wondering what the next stocks will be that hit it big, with solid fundamentals? Enter your email address to see which stocks MarketBeat analysts could become the next blockbuster growth stocks.

Get This Free Report