Dividends over drama, please. Like these five steady stocks that yield 7.2%, on average.

Back in school they taught us that to increase returns, investors had to take on additional risk. This was a financial engineering class at Cornell University, by the way. The prof should have known better, but he didn’t, because he was a researcher and not an actual investor.

It’s a common mistake in academia, and those who try to invest “buy the book.” The book says more beta means more returns. Well, this text is often wrong!

Big dividends and low volatility are a beautiful combination.

Volatility can be measured several ways. I find that “beta” is one of the best ones for regular investors because it’s easy to understand, and because it’s widely available from just about every market data provider.

Beta measures an investment’s volatility against a benchmark. The benchmark (for instance, the S&P 500) will always have a beta of 1. So:

- A stock with a beta of 1 moves in line with the market.

- If the S&P 500 gained 1%, we’d expect the stock to gain 1%.

- A stock with a beta above 1 is more volatile than the market.

- If the S&P 500 gained 1%, we’d expect a stock with a beta of 1.5 to gain 1.5%

- A stock with a beta below 1 is less volatile than the market.

- If the S&P 500 gained 1%, we’d expect a stock with a beta of 0.5 to gain 0.5%

Importantly, the reverse tends to be true—high-beta stocks generally fall more sharply than the market, while low-beta stocks often decline by less.

So if we want some peace of mind, especially in a market like this, we want low-beta stocks.

And if we really want to improve our chances of enjoying upside in downturns, we also want high yields. That’s in part because of the income return potential itself, but also because that income tends to attract more buyers during market scares.

So let’s review several stocks that …

- Have low volatility

- Have produced gains against a down market in 2025

- Have high yields—they average 7.2% as a group, which would generate a healthy $72,000 annually on a million-dollar nest egg.

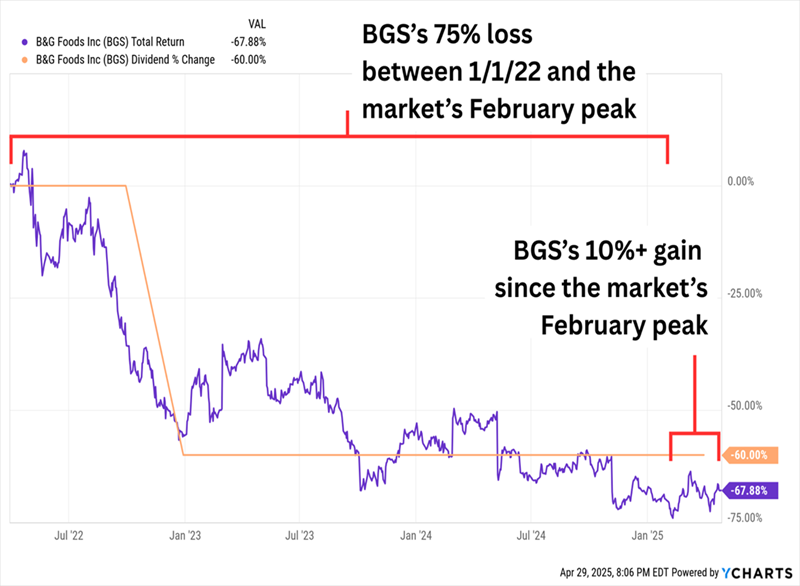

Let’s start with B&G Foods (BGS, 11.1% yield), which we’ve discussed very recently, because it serves as a perfect warning about the dangers of relying on headline numbers alone.

A stock can look like a perfect candidate in a screener, only to fall apart after just a little bit of scrutiny.

B&G Foods is a consumer staples stock whose brands include pantry regulars like Crisco and Cream of Wheat. It has an 11% yield. Its 5-year beta is 0.8. Its 1-year beta is negative 0.6, which implies that when the market zigs, it zags—exactly what we want in a down market. And B&G is killing it in 2025. The market is off about 10% since its Feb. 19 high; BGS shares are up by more than 10%.

What’s not to love?

That’s Not So Great.

It’s arguable that the only reasons BGS has defied the market’s gravity lately are its yield and positioning in the staples sector. Past that, though, B&G earned less than it paid out in dividends last year, and it’s projected to do so this year and next. It’s also just a couple months removed from having to write down the worth of several of its best brands.

Great headline metrics, but it’s downhill from there.

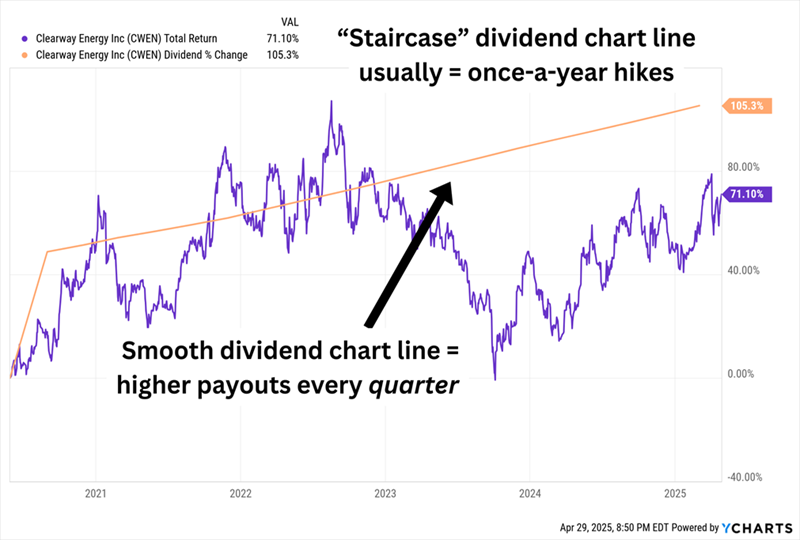

Clearway Energy (CWEN/CWEN.A, 5.8% yield) is a different story.

CWEN owns a portfolio of non-regulated clean energy generation assets representing 11.8 gigawatts of gross capacity—9 gigawatts from wind, solar, and battery energy storage systems, and 2.8 gigawatts of conventional dispatchable power capacity. So while it’s technically in the utility sector, its operations aren’t the same as our garden-variety power-or-gas “ute.”

However, like utilities, Clearway is enjoying a surge in demand from data centers. It’s already developing traditional data center agreements, but it’s also beginning to scope “behind-the-meter” agreements, where data centers generate energy on-site using renewables rather than tapping into a traditional utility grid. CWEN has also been re-contracting its gas portfolio, which takes some important question marks off the board for the next few years.

Clearway seems to have plenty of firepower to support its 5%-8% annual dividend growth goal. That’s a fine level for a stock that’s already yielding nearly 6%, and better still, shareholders have been enjoying those raises on a quarterly basis for years.

This Is What Getting Paid More Every Paycheck Looks Like

In addition to the dividend, shareholders have enjoyed relative stability of late—CWEN’s five-year beta of 0.9 is a hint less volatile than the market, but its shorter-term beta of around 0.4 reflects much smoother sailing over the past year.

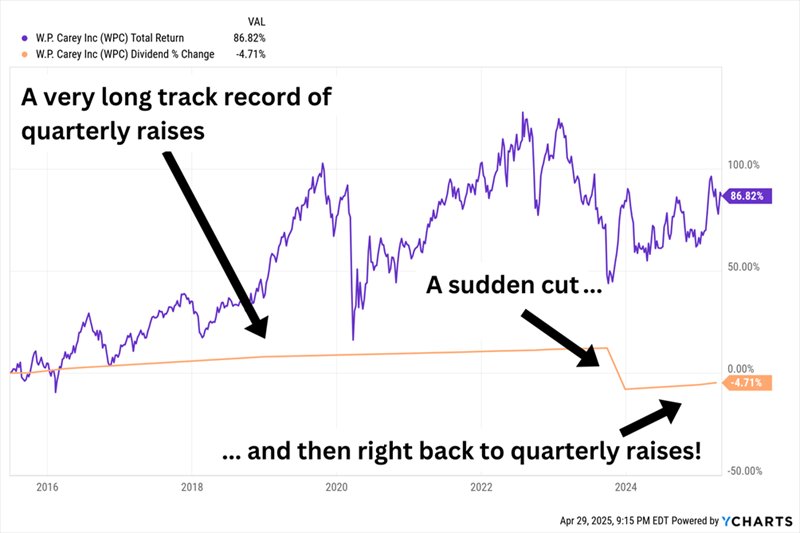

W.P. Carey (WPC, 5.8% yield) is another quarterly dividend raiser, but its smooth path has quite the hiccup in it.

It Got Knocked Down, But It Got Up Again

W.P. Carey is a massive, diversified net-lease real estate investment trust (REIT) that boasts more than 1,600 properties leased out to more than 360 tenants in 90 industries. More than a third of its portfolio is made up of industrial real estate, another quarter is warehouses, about 20% is retail, and the remainder is scattered across other property types including self-storage.

What’s missing there is office properties, which W.P. Carey exited in September 2023 by spinning them off into Net Lease Office Properties (NLOP). Alongside that plan was a necessary “reset” of the dividend policy to account for the shift in assets.

In other words, WPC’s dividend “cut” was merely a technicality—the dividend itself is quite healthy. That’s in part because virtually its entire portfolio (99.6%) includes rent escalators; high occupancy of 98%-plus helps, too.

Five- and one-year betas of 0.8 and 0.3, respectively, reflect W.P. Carey’s status as a historically cool cucumber, too.

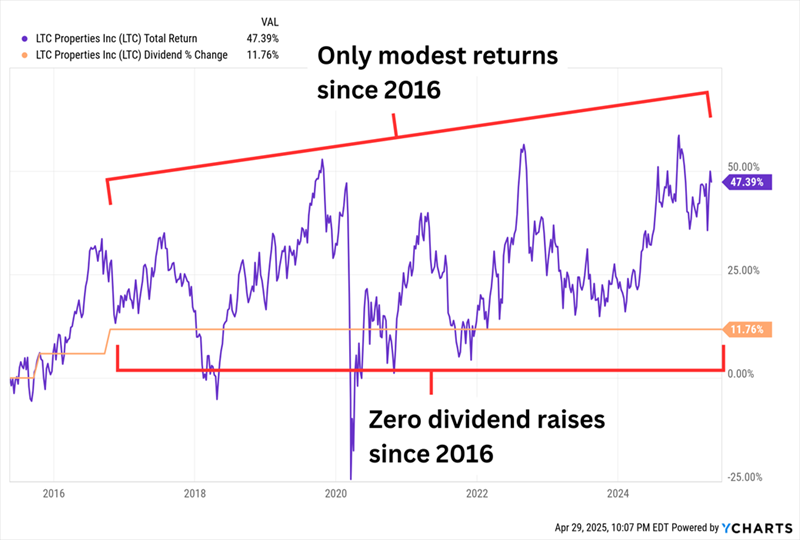

Another REIT, LTC Properties (LTC, 6.4% yield), offers up the gold standard in dividend delivery: monthly payments.

LTC, which stands for “long-term care,” boasts 190 properties in 25 states, with its investments split roughly 50/50 between assisted living properties and skilled nursing facilities. These were promising businesses until COVID ruptured the space; operations are recovering, though.

The stock actually managed to hit its pre-COVID high back in 2023, but that was short-lived. But its second attempt, which started six months ago, is looking better—and shares are stabilizing while the rest of the market falters. LTC not only boasts a five-year beta of 0.7 (good), but an extremely low one-year beta of just over 0.1 (great).

That said, LTC is walking into a whirlwind of uncertainty—though possibly for the better. The company plans on pivoting to a RIDEA structure, which stands for the REIT Investment Diversification and Empowerment Act. Without getting too far into the weeds, this act lets REITs participate in net operating income, and it’s where LTC believes the majority of external growth opportunities in assisted living remain. Specifically, the company expects to convert $150 million to $200 million of gross investment assets to RIDEA-structured contracts by Q2 2025.

It’s a potentially transformative structure, but also a complete unknown. One vital sign to look out for? A long, long-needed increase in its dividend, which has remained stagnant for nearly a decade.

REIT Investors Expect Better Payout Performance Than This

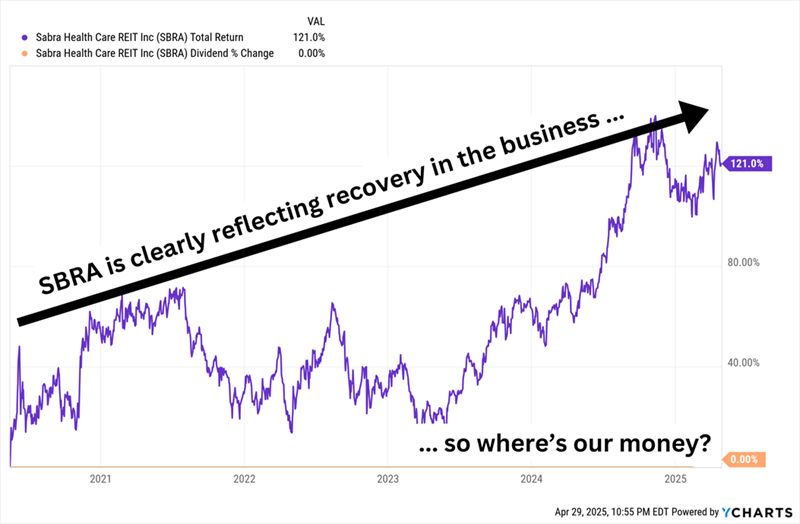

Sabra Health Care REIT (SBRA, 6.9% yield) is similar to LTC in that it’s a senior-focused healthcare play. Roughly half of Sabra’s portfolio is in skilled nursing and transitional care facilities, though it also has large allocations to managed senior housing (20%), behavioral health (14%) and leased senior housing (11%).

A big signal of improvement in Sabra’s operational health came a little more than a year ago when it provided full-year guidance. Yes, that guidance missed estimates, but it actually released guidance—something it wasn’t able to do a year before that.

That said, like LTC, while we’re seeing improvement in the underlying business, we need to see that improvement in our pockets, too.

SBRA’s Dividend Hasn’t Budged Since Its 2020 Distribution Cut

Still, SBRA ended up returning more than 30% in 2024, crushing the VNQ and its piddly 5% advance.

Shares have cooled off in 2025 but are still up a few percentage points since the Feb. 19 market peak. They also offer a high yield of nearly 7%, and extremely low volatility—a beta of 0.9 over the past five years isn’t much to look at, but it has registered a nearly unconscious beta of 0.2 over the past 52 weeks. And health care REITs could continue to be defensive if the economic environment continues to worsen.

5 Soaring Dividends That Were Made for This Trade War

We all know the score. Investors are fleeing to low-vol and other safety trades because America’s trade war with the rest of the world is threatening us with recession, inflation, stagflation, you name it.

And that’s why I’ve put together a “mini-portfolio” of 5 picks my Dividend Magnet system has pinpointed as the very best “battleship” dividends to own right now.

They’ve held up well in past downturns. They throw off steady dividend payouts. And they provide services and products consumers must have, whether we’re in a recession, a trade war, an inflation spike—it just doesn’t matter.

Each of these 5 stocks pays a rich (and growing) dividend. Each trades at a bargain. And I’m ready to GIVE you their names in a free Special Report.

The time to buy them is now. Click here and I’ll tell you more about them and give you my complete Dividend Magnet strategy. You’ll also learn how to get that free Special Report, which names all 5 of these soaring “Dividend Magnet” stars.

Before you make your next trade, you'll want to hear this.

MarketBeat keeps track of Wall Street's top-rated and best performing research analysts and the stocks they recommend to their clients on a daily basis.

Our team has identified the five stocks that top analysts are quietly whispering to their clients to buy now before the broader market catches on... and none of the big name stocks were on the list.

They believe these five stocks are the five best companies for investors to buy now...

See The Five Stocks Here

Thinking about investing in Meta, Roblox, or Unity? Enter your email to learn what streetwise investors need to know about the metaverse and public markets before making an investment.

Get This Free Report