Small-cap stocks haven’t been this cheap in decades. This valuation advantage gets interesting when we add big fat dividends and today, we’ll discuss five cheap small stocks yielding between 8.3% and 17.1%. (That’s no typo by the way—we only talk serious dividends here at Contrarian Outlook!)

The Apples, Google and Microsofts of the world are priced like luxury goods. Smaller stocks, meanwhile, have been left at the discount rack. Let’s shop:

- S&P 500: 21.2 times earnings (pricey!)

- S&P MidCap 400: 15.4 times (better…)

- S&P SmallCap 600: 14.7 times (bingo!)

The valuation spread between the S&P 500 and S&P 600 hasn’t been this wide since Bill Clinton was wondering whether dot-com was one word or two. Is a bust to follow again or are these big yields from small stocks really spectacular deals? Let’s explore.

Playtika Holding (PLTK)

Dividend Yield: 8.3%

Israel-based Platytika Holding (PLTK) is a gamemaker that primarily makes casino-themed titles for countries on just about every continent. Here in the U.S., Playtika’s best-known titles include Bingo Blitz, Redecor and Domino Dreams.

Playtika has done quite a bit of building by acquisition, purchasing Seriously, JustPlay.LOL, Youda Games, Innplay Labs and, most recently, SuperPlay, among others. (It tried to buy Angry Birds maker Rovio in 2023, but the deal eventually fell apart.)

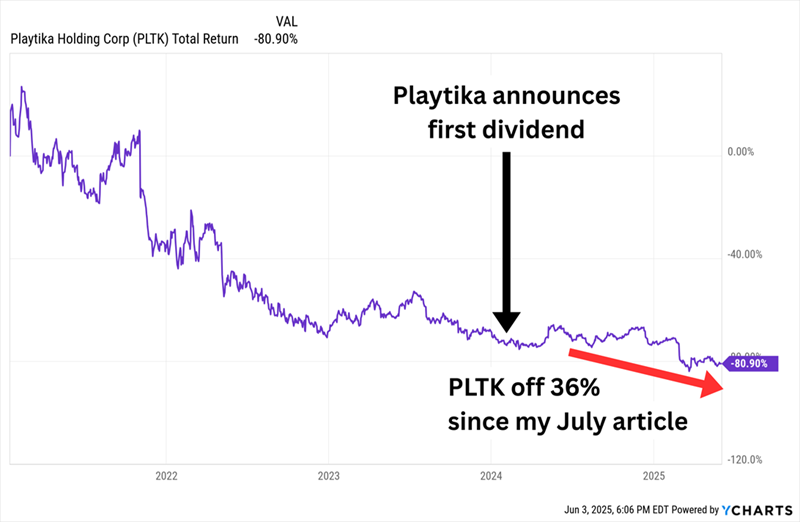

Playtika hasn’t been a dividend stock for very long—it initiated its dividend program in late February 2024. About a year ago, when I examined PLTK among other “inaugural dividends,” I mentioned its 10-cent-quarterly dividend translated into a nice 5% yield, but also more than 60% of the company’s estimated earnings for 2024. By the time all was said and done, it ended up being closer to 70% of adjusted profits for last year.

Fast-forward to today: PLTK hasn’t raised its payout, but it now yields north of 8%. This is the “wrong way” to raise a dividend.

Playtika’s Downward Spiral Continues

As I said in my previous writeup, the mobile game market is brutal, especially among the “free to play” titles that Playtika specializes in. PLTK had been suffering from years of profit declines and flat sales, and sure enough, 2024 saw another drop in earnings and a modest decline in sales.

And yet … the few pros who cover the stock are quite bullish about what comes next. While revenue growth estimates for the next two years aren’t much to scream over, they’re looking for a 32% jump in profits this year, and a respectable 23% improvement in 2026. Meanwhile, PLTK’s woeful performance has driven the dividend higher and its valuation down to a dirt-cheap 6 times forward earnings.

Still, Playtika is asking for a lot of faith in its growth prospects while (so far) providing very little evidence.

Carlyle Secured Lending (CGBD)

Dividend Yield: 12.6%

Carlyle Secured Lending (CGBD) is a business development company (BDC) that’s externally managed by a subsidiary of multinational asset manager Carlyle Group (CG).

CGBD invests primarily in U.S. middle market companies with between $25 million and $100 million in annual EBITDA. And it predominantly deals in first-lien debt (83%), though it has single-digit exposure to second-lien debt, equity investments and even investment funds. Its 138 portfolio companies cover a couple dozen industries, including healthcare/pharmaceuticals, software, consumer services, and business services.

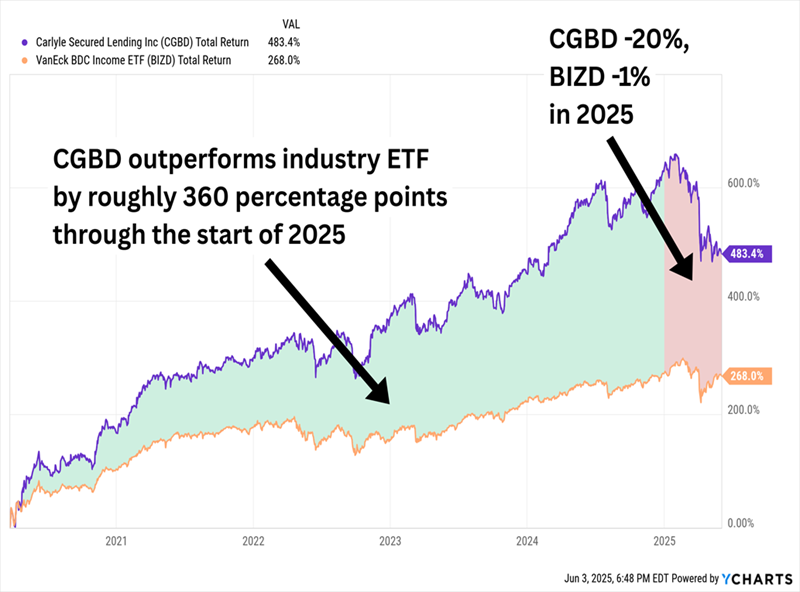

Carlyle Secured Lending came public in 2017. And as we neared the end of 2024, I noted that shares had and spent most of their time putting up downright excellent returns.

Things have changed—drastically!—since then.

In Short: 2025 Has Been a Train Wreck for CGBD

What went wrong?

Two earnings reports have revealed some growing cracks in Carlyle’s armor. In February, profits came in below estimates, thanks largely to a markdown on hotel management company Aimbridge Hospitality. It also doubled the number of companies on non-accrual (loans that are delinquent for a prolonged period, usually 90 days), from two to four. In May, the company reported disappointing earnings again, and an additional company went on non-accrual, bringing non-accruals up to 1.6% of the total portfolio at fair value.

More importantly, the company announced it would only pay a base dividend of 40 cents per share. That’s problematic for two reasons:

- Carlyle Secured Lending’s base dividend had been on the rise for several years. If past was precedent, Carlyle would have increased the dividend during Q1 2025, but it remained stagnant.

- The company announced there would be no special dividend. CGBD is among numerous BDCs that regularly augment their base payout with special dividends, and in fact, Carlyle hadn’t missed a beat since 2020.

Based on net investment income (NII) estimates for the rest of the year, dividend coverage could be tight; it’s possible the company might need to rely on “spillover” income to cover the payout for at least a quarter or two.

CGBD is just a couple months removed from a potentially beneficial merger with another BDC, Carlyle Secured Lending III; even without any more specials, its base dividend translates into an 11%-plus yield; and shares now trade at a nice 16% discount to net asset value (NAV). But I’d like to see signs that CGBD is correcting its recent operational slide.

Bain Capital Specialty Finance (BCSF)

Dividend Yield: 11.5%

Bain Capital Specialty Finance (BCSF) is a diversified BDC that provides a variety of financing solutions to 175 portfolio companies primarily in North America, but also Europe and Australia (a rarity for many BDCs).

The lion’s share of Bain Capital’s investments are first-lien in nature—in addition to 64% exposure directly through portfolio companies, it also has almost 16% more through its investment vehicles. It also deals in equity and preferred equity interest, as well as second-lien and subordinated debt.

Unlike CGBD, Bain Capital hasn’t exactly lit the industry on fire, but it has caught its stride over the past couple of years. Other reasons to like it? A low cost of debt, a higher-than-average portfolio yield (made even better by its joint ventures), investment-grade debt and an 11% discount to NAV.

However I’m nervous about its dividend situation.

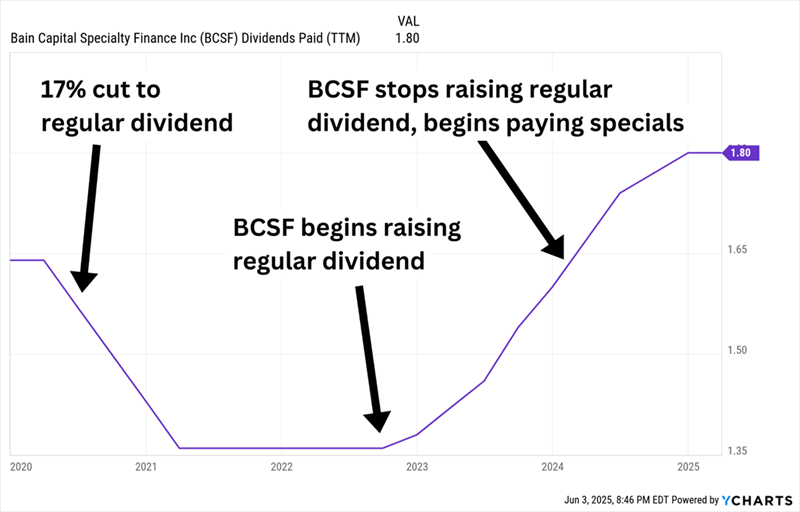

BCSF Shifted to a Base-Plus-Special Model in 2024

Dividend coverage has been a strength for the past couple of years, but that could be changing. In 2024, Bain Capital stopped a short streak of dividend hikes and kept its 42-cent regular dividend in place. It instead began paying 3-cent quarterly special dividends, which it has kept up with ever since.

That 45 cents quarterly comes out to $1.80 per share in annual dividends.

However, analysts expect net investment income to drop from $2.09 per share in 2024 to $1.84 per share this year and $1.82 per share in 2026. That means dividend ratios in the 98%-99% range, which leaves almost no room for error. If BCSF does run into difficulty over the next couple of years, we could see the special dividends reduced or taken away outright—certainly a better look than having to cut a regular dividend, but the practical end result is still less income, even if temporarily.

On the other hand, the base-and-special system gives BCSF room to reward us more if Wall Street’s expectations prove overly pessimistic.

Two Harbors Investment Corp. (TWO)

Dividend Yield: 17.1%

Let’s move to another high-yield corner of the market: mortgage real estate investment trusts (mREITs).

For the unfamiliar: The typical REIT deals in physical properties—apartments, strip malls, hospitals, casinos. But mortgage REITs deal in “paper” real estate. They borrow at low short-term rates, lend that cash out in the form of mortgages based on long-term rates, then pocket the difference.

If “long” rates (like those on the 10-year Treasury) are steady or, better yet, declining, that’s great news for mREITs. New loans pay less, so their existing loans become more valuable.

That’s been a mixed bag for mREITs in 2025, which enjoyed declining rates for the first couple months of the year, but have been suffering from a rebound ever since.

First up is Two Harbors Investment (TWO), which deals in mortgage servicing rights (MSRs), agency residential mortgage-backed securities (RMBSs) and other financial assets. It also owns an operational platform, RoundPoint Mortgage Servicing LLC, and it has a direct-to-consumer originations business that’s still in its early innings.

Whenever we see a yield near 20%, it’s almost always caused by a sharp decline in share prices. That’s very much the case with Two Harbors, whose shares traded in the $60s before collapsing during COVID, only mildly rebounded, then deteriorated ever since to current prices around $10 per share.

That action pretty accurately reflected a miserable operating picture:

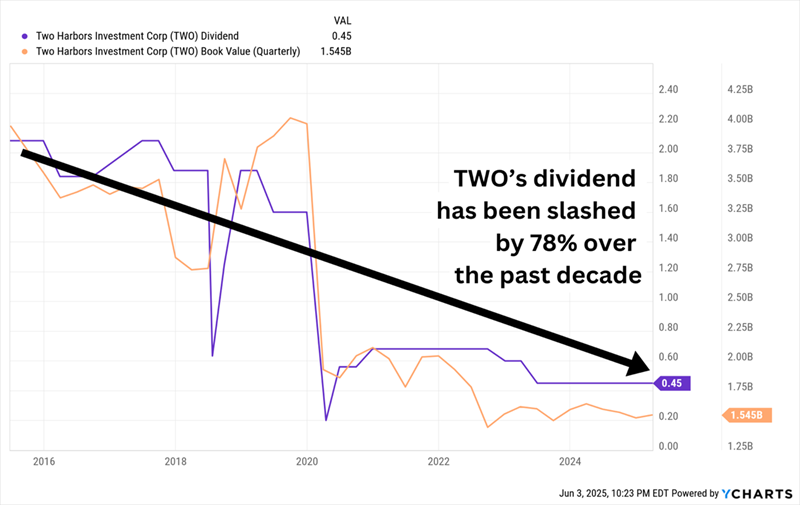

2020 Forced a “Hard Reset” in TWO’s Book Value and Dividend

Still, we’re talking about a 17%-plus yield. If there’s any sort of redeeming value, it’s worth looking into. Well, Two Harbors has been working on lowering its debt-to-equity ratio, the company’s book value ticked up in the most recent quarter, and it trades at a low 70% of that (still relatively decimated) book value.

But all of those positive bullet points have been canceled out by an 8-K filed near the end of May.

Two Harbors announced it was taking a $198.9 million charge related to litigation dating back to 2020 against PRCM Advisers, its former external manager. That comes out to roughly $1.90 per share, or 13% of TWO’s last reported book value of $14.66 per share.

The potential danger is that this significant hit to book value could impact earnings available for distribution (EAD), putting its current dividend rate of 45 cents per share at risk. While the company doesn’t report earnings until July, TWO typically announces its dividends in the middle of the month prior to the month in which it reports—so, in this case, we might know by sometime in mid-June.

Too much dividend drama.

Franklin BSP Realty Trust (FBRT)

Dividend Yield: 13.0%

Take Franklin BSP Realty Trust (FBRT), a mortgage REIT dealing in commercial mortgage-backed securities (CMBSs). Multifamily is king here, at more than 70% of the portfolio, but FBRT is happy to take on just about any type of commercial property—it also holds loans in hospitality, industrial, office, retail and other sectors.

Virtually all of its portfolio is senior debt, and nearly 90% of that is floating-rate in nature. Collateralized loan obligations are the bulk of its financing sources at a hair over 80%, but Franklin BSP Realty Trust also has 11% exposure to warehouse lending (credit lines extended by banks to originate mortgages), 5% to repurchase agreements (repo), and sprinklings of unsecured debt and asset-specific financing.

FBRT shares are down by double digits year-to-date, but now trade at an attractive 28% discount to book and a P/E of around 7 based on 2026 earnings estimates, which is pretty low among mREITs. And there are reasons for optimism—chiefly, the looming July close on the acquisition of NewPoint Holdings JV LLC. The deal to absorb this privately held commercial real estate finance company could set Franklin apart from other commercial mREITs.

Again, though, the dividend situation is perhaps shakier than many of us would want.

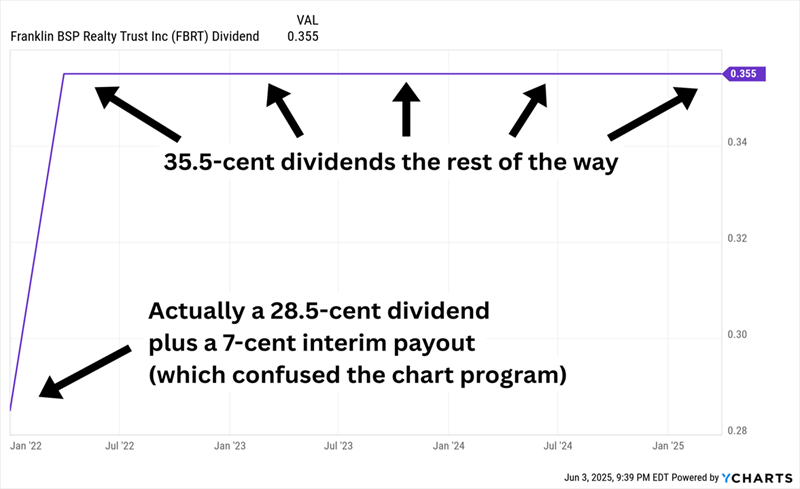

For one, the payout hasn’t budged since the company started trading in 2021:

If Not for a Chart Error, FBRT’s Dividend Growth Is a Horizontal Line

Also problematic—real-estate owned (basically, foreclosures) and short-term non-market financing have been dragging on earnings. On the most recent conference call, CFO Jerome Baglien said, “While we believe in the long-term earning power of the company to cover the dividend, if REO sales slow or volatile market conditions persist, it could be prudent to revisit our dividend in the short term.”

There is a little good news: If earnings expectations stay on track, on the other side of FBRT’s short-term drag is a path to more solid dividend coverage longer-term.

This 11% “Trump 2.0 Buy” Is on Firmer Footing—And Another Big Distribution Is Coming Up Soon

Some of these stocks have potential for aggressive investors as dirt-cheap distressed properties that, if the stars align, could be flipped for a profit eventually.

There’s a time and a place for those kinds of trades.

But when it comes to investing our hard-earned money in companies that can actually generate meaningful retirement income for years on end … we need high yields and solid track records.

Right now we’re buying another investment that delivers both.

In fact, this heralded closed-end fund (CEF) checks off a bunch of important retirement boxes in a major way:

- A huge dividend—11% at current prices!

- Monthly distributions

- A big—and highly unusual—discount in disguise!

This isn’t some vanilla index fund. This CEF is actively run by bond royalty. This fund captain has been named Fixed Income Manager of the Year by Morningstar, and he has been inducted into the Fixed Income Analysts Society Hall of Fame!

As rates fall and other income options wane, I expect this 11% payer’s discount/dividend combo to be a shiny lure for the mainstream crowd. And we have a shot at “front-running” them today.

Don’t miss this opportunity. Click here and I’ll tell you about this incredible 11%-paying fund and how to get your FREE Special Report revealing the name, ticker and my detailed research.

Before you make your next trade, you'll want to hear this.

MarketBeat keeps track of Wall Street's top-rated and best performing research analysts and the stocks they recommend to their clients on a daily basis.

Our team has identified the five stocks that top analysts are quietly whispering to their clients to buy now before the broader market catches on... and none of the big name stocks were on the list.

They believe these five stocks are the five best companies for investors to buy now...

See The Five Stocks Here

Wondering what the next stocks will be that hit it big, with solid fundamentals? Enter your email address to see which stocks MarketBeat analysts could become the next blockbuster growth stocks.

Get This Free Report