Individual retirement accounts (IRAs) offer retirement savers tax breaks on the money they contribute, but only if they adhere to certain rules and stipulations. A traditional IRA has a tax break on the front end, where you can deduct contributions from your taxes unless your income exceeds the limit.

But Roth IRAs offer a tax break on the back end, so you make contributions with already-taxed dollars and investments grow tax-free. High earners cannot access either tax break unless they utilize a conversion technique we'll detail below. This article will discuss the backdoor Roth IRA 2023 strategy and its benefits if you follow the process correctly.

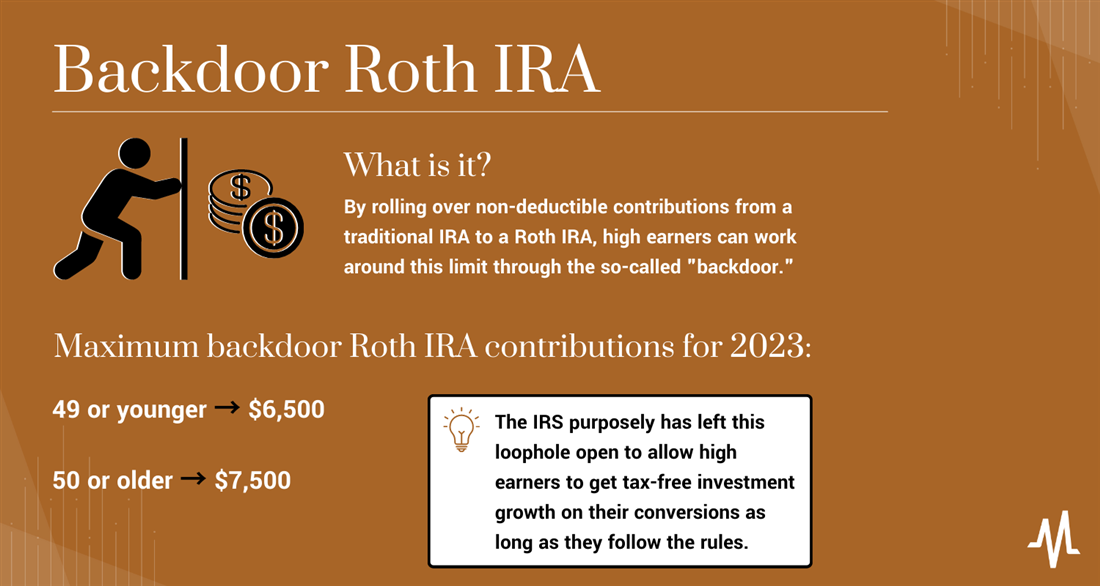

What is a Backdoor Roth IRA?

Traditional and Roth IRAs are specific accounts you can open at your brokerage or bank with minimal hassle. You fill out your information, apply for the account and in most cases, you can contribute funds the same day. Both IRAs are subject to the same $6,500 contribution limit ($7,500 if you're 50 or older) for 2023, meaning your combined contributions across all IRAs cannot exceed this amount for the calendar year.

The backdoor Roth may sound like an entirely new type of account, but it's actually a strategy. Because not only do traditional and Roth IRAs have contribution limits, but they also have income limits on who can get the benefits. For traditional IRAs, if you don't have a workplace retirement plan, you can deduct the $6,500 annual contribution regardless of income. But if a workplace plan covers your spouse and you file jointly, the tax deduction begins to phase out at $218,000 and ends entirely at $228,000.

If you do have a workplace retirement plan, you can only take the full deduction with income up to $73,000 (or $116,000 if married and filing jointly). The deduction phases out after those levels and ends at $83,000 ($138,000 for married filers).

For Roth IRAs, there's no upfront tax deduction to limit for high earners. Instead, contribution limits are reduced or cut off once your income exceeds a certain level. For example, in 2023, single fliers get a reduced contribution limit starting at $138,000 and cannot contribute anything once income reaches $153,000. For married fliers, these limits are $218,000 and $228,000, respectively.

Here's where your 2023 backdoor Roth IRA strategy comes in. Just because high earners cannot contribute to a Roth IRA directly doesn't mean they can't access the account benefits. By rolling over non-deductible contributions from a traditional IRA to a Roth IRA, high earners can work around this limit through the so-called "backdoor."

Who is a Backdoor Roth IRA for?

Utilizing the backdoor Roth IRA isn't cheating the system. The IRS purposely has left this loophole open to allow high earners to get tax-free investment growth on their conversions as long as they follow the rules.

For a backdoor Roth 2023, the primary beneficiaries are individuals with reported income over $153,000 or married couples filing jointly with income over $228,000. Retirement savers with incomes at this level usually don't get tax-advantaged investment growth, but the backdoor Roth loophole allows them to get not only tax-free asset growth but the other benefits of Roth accounts like no RMDs or the ability to withdraw principal at any time without penalty.

Benefits of a Backdoor Roth IRA

Here are the main benefits of using the backdoor Roth IRA strategy utilizing the backdoor Roth IRA limit 2023.

Tax-Free Investment Growth for High Earners

The top benefit is the obvious one. High earners can get around the usual Roth IRA income limits by converting funds from a traditional IRA to a Roth (as long as they follow the steps below). Once you fund the account, the stocks, bonds or other investments held in the Roth IRA will grow free from taxation. You still must adhere to the withdrawal rules to avoid penalties, though.

No Required Minimum Distributions

Tax-free investment growth isn't the only benefit of a Roth IRA. With traditional IRAs and 401(k) accounts, retirement savers must begin drawing down their accounts at age 70, regardless of whether they need the money. Many tax headaches can arise if you're unprepared for RMDs. But Roth IRAs do not require RMDs, meaning savers can withdraw as little or as much as they want from the account without penalty once they hit age 59 1/2.

Mega Backdoor Roth

A mega backdoor Roth conversion may sound like something from a "Transformers" movie, but it's actually a tweak to the backdoor Roth strategy that allows eligible participants to contribute up to $66,000 (or $73,500 if they're older than 50). You'll need a workplace account like a traditional 401(k) that allows non-deductible contributions to use this technique.

How to Open a Backdoor Roth IRA

Here are the steps to follow if you want to utilize the backdoor Roth IRA

Step 1: Open a traditional IRA (if you don't already have one).

You'll first need a traditional IRA to use the backdoor Roth IRA conversion.

Can you have traditional and Roth IRA accounts? Of course! Opening a traditional IRA is a simple process at any major brokerage firm and can usually be completed in a few minutes.

Step 2: Make a non-deductible contribution to your traditional IRA.

You can contribute up to $6,500 per year into a Roth IRA — the maximum amount you can convert from a traditional IRA to a Roth using this process. If your income is high enough or a workplace plan covers you, your traditional IRA tax break will be limited or nonexistent anyway. But the amount you seek to convert using a backdoor Roth IRA must come from dollars already taxed.

Step 3: Convert funds from your traditional IRA to a Roth.

Now you'll need to convert the cash in your traditional IRA to a Roth. Remember, this must be a non-deductible contribution going into the Roth IRA. For most brokerage houses, the conversion process will be simple. Backdoor Roth IRA contribution limits are the same as the front door variety ($6,500 in 2023, $7,500 if 50 or older). Since the funds were already taxed, you don't need to worry about paying the IRS as you would in a standard traditional to Roth IRA conversion.

Step 4: Mind the aggregation rule.

If you only have a traditional IRA to fund a backdoor Roth conversion, you won't need to worry too much about the aggregation rule. But you'll need to understand the IRS's aggregation rule if you have more than one traditional IRA or a single well-funded account. All traditional IRAs are treated as a single entity, meaning it's one account for tax purposes. If you open a traditional IRA just to make a backdoor conversion but have a traditional IRA at another broker with pre-tax contributions, you might face taxes.

For example, you make a full non-deductible contribution to a traditional IRA ($6,500) and roll it into a Roth. But you already have $6,500 in deductible contributions parked in a different traditional IRA. In this case, you'd owe taxes on 50% of your conversion amount since the total value of all your traditional IRAs was $13,000.

Contribution Limits

Here are the maximum Roth IRA contribution 2023 limits:

|

Age

|

Backdoor Roth IRA Contribution Limit 2023

|

|

49 or younger

|

$6,500

|

|

50 or older

|

$7,500

|

As mentioned above, income limits apply when taking a tax deduction from a traditional IRA or contributing directly to a Roth IRA. You and your spouse's use of a workplace retirement plan like a 401(k) account may also influence the amount of traditional IRA contributions you can deduct.

How to Avoid Penalties

Roth IRAs have a few unique features that make them arguably the best tax-advantaged retirement accounts, but you still need to follow some rules to avoid penalties. If you convert a traditional IRA into a Roth IRA with after-tax dollars, you can withdraw this principal whenever you like, but only after five years. Since it's a conversion, not a contribution, you must wait five years to touch that money as if you were opening a new Roth IRA each time. Remember this five-year rule when buying any stock investments for your account.

Additionally, you must know the Aggregation Rule and understand that backdoor Roth IRA conversions are taxed pro-rata. Don't think you can avoid taxation by making a single non-deductible contribution to a traditional IRA. Since all traditional IRAs count as a single entity, all distributions are taxed based on the percentages of pre- and post-tax dollars in the account. To avoid headaches from this rule, having all traditional IRA balances at zero is ideal by the end of the tax year.

When Not to Consider this Strategy

Here are a few scenarios where the backdoor Roth IRA conversion might not make sense:

- If you make less than $138,000 annually (or $218,000 if married and filing jointly)

- If you have a large amount of pre-tax contributions in various traditional IRAs, and will be taxed on backdoor conversions due to the aggregation rule

- If a backdoor Roth IRA conversion will bump you into a higher tax bracket

- If you want to withdraw your conversion amount within five years

Backdoor Roth Conversions: Useful for High Earners

Roth IRAs are great retirement and estate planning tools, but income restrictions require high earners to use a backdoor Roth IRA conversion to access the benefits. The ideal scenario for backdoor Roth IRA conversions is to contribute a full non-deductible $6,500 to a traditional IRA and convert it to Roth, avoiding all taxes and immediately getting access to tax-free investment growth.

Having all traditional IRA balances at zero will avoid any tax implications from the IRS's aggregation rule, which can be difficult to calculate. And remember to file IRS Form 8606 for all backdoor Roth conversions, even if you don't owe a dime in taxes.

FAQs

Backdoor Roth IRA conversions can be a tricky subject. Here are a few of the most frequently asked questions about them in 2023.

Will backdoor Roth be eliminated in 2023?

Is backdoor Roth going away? Not likely anytime soon. While some politicians have discussed limiting or eliminating the backdoor Roth loophole, there seems to be little possibility now.

What is the backdoor Roth IRA limit in 2023?

The limit on a backdoor Roth IRA conversion is the same as the limit if you make a standard contribution. For 2023, that limit is $6,500 for individuals under 50 and $7,500 for those 50 and older.

How many backdoor Roths can you do in a year?

There's no limit to the number of Roth conversions you can make, but most investors can do a single backdoor conversion per year with the full $6,500 lump sum. Make a non-deductible $6,500 contribution to your traditional IRA, immediately convert it to a Roth and enjoy the benefits of the account without any tax headaches on the conversion.

Before you make your next trade, you'll want to hear this.

MarketBeat keeps track of Wall Street's top-rated and best performing research analysts and the stocks they recommend to their clients on a daily basis.

Our team has identified the five stocks that top analysts are quietly whispering to their clients to buy now before the broader market catches on... and none of the big name stocks were on the list.

They believe these five stocks are the five best companies for investors to buy now...

See The Five Stocks Here

Discover the 10 Best High-Yield Dividend Stocks for 2026 and secure reliable income in uncertain markets. Download the report now to identify top dividend payers and avoid common yield traps.

Get This Free Report

Like this article? Share it with a colleague.

Link copied to clipboard.