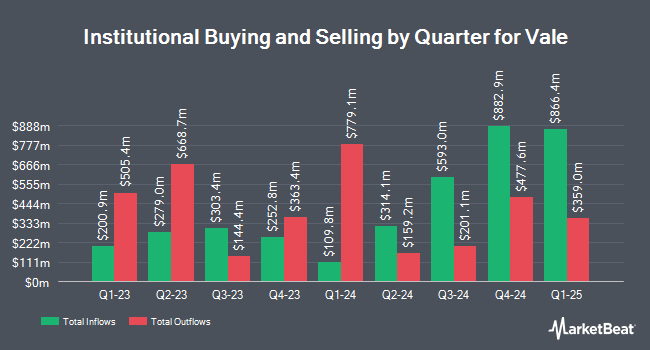

Ascent Group LLC increased its stake in shares of Vale S.A. (NYSE:VALE - Free Report) by 197.2% in the 1st quarter, according to its most recent disclosure with the Securities & Exchange Commission. The fund owned 59,968 shares of the basic materials company's stock after purchasing an additional 39,791 shares during the period. Ascent Group LLC's holdings in Vale were worth $598,000 as of its most recent filing with the Securities & Exchange Commission.

Several other hedge funds have also recently made changes to their positions in VALE. Banque Transatlantique SA purchased a new position in shares of Vale during the first quarter valued at approximately $30,000. Golden State Wealth Management LLC increased its holdings in Vale by 193.0% during the first quarter. Golden State Wealth Management LLC now owns 4,119 shares of the basic materials company's stock valued at $41,000 after buying an additional 2,713 shares during the last quarter. J.Safra Asset Management Corp purchased a new stake in Vale during the first quarter valued at approximately $41,000. Capital Analysts LLC purchased a new stake in Vale during the first quarter valued at approximately $51,000. Finally, Allworth Financial LP increased its holdings in Vale by 233.7% during the first quarter. Allworth Financial LP now owns 5,440 shares of the basic materials company's stock valued at $53,000 after buying an additional 3,810 shares during the last quarter. 21.85% of the stock is owned by hedge funds and other institutional investors.

Analyst Upgrades and Downgrades

A number of analysts have commented on VALE shares. Clarkson Capital started coverage on shares of Vale in a report on Wednesday, September 3rd. They set a "buy" rating and a $12.00 target price for the company. Zacks Research cut shares of Vale from a "hold" rating to a "strong sell" rating in a report on Tuesday, September 9th. Scotiabank reduced their target price on shares of Vale from $13.00 to $12.50 and set a "sector perform" rating for the company in a report on Tuesday, July 22nd. Barclays upped their target price on shares of Vale from $12.75 to $13.00 and gave the company an "overweight" rating in a report on Wednesday, July 2nd. Finally, JPMorgan Chase & Co. reduced their target price on shares of Vale from $15.00 to $13.50 and set an "overweight" rating for the company in a report on Thursday, September 4th. Six research analysts have rated the stock with a Buy rating, five have issued a Hold rating and one has issued a Sell rating to the stock. According to data from MarketBeat.com, the company presently has a consensus rating of "Hold" and an average price target of $11.71.

Read Our Latest Research Report on VALE

Vale Price Performance

Shares of NYSE VALE traded up $0.04 during midday trading on Tuesday, reaching $10.87. The stock had a trading volume of 14,299,693 shares, compared to its average volume of 35,840,125. The stock has a 50-day moving average of $10.08 and a 200-day moving average of $9.72. The company has a debt-to-equity ratio of 0.48, a quick ratio of 0.85 and a current ratio of 1.22. The company has a market capitalization of $49.33 billion, a price-to-earnings ratio of 8.85 and a beta of 0.79. Vale S.A. has a 12-month low of $8.06 and a 12-month high of $12.05.

Vale (NYSE:VALE - Get Free Report) last announced its quarterly earnings data on Thursday, July 31st. The basic materials company reported $0.50 earnings per share (EPS) for the quarter, topping analysts' consensus estimates of $0.34 by $0.16. The firm had revenue of $8.80 billion during the quarter, compared to analysts' expectations of $9.54 billion. Vale had a net margin of 14.23% and a return on equity of 18.14%. As a group, research analysts anticipate that Vale S.A. will post 1.85 EPS for the current fiscal year.

Vale Cuts Dividend

The business also recently announced a semi-annual dividend, which was paid on Wednesday, September 10th. Investors of record on Wednesday, August 13th were paid a dividend of $0.3417 per share. This represents a yield of 740.0%. The ex-dividend date of this dividend was Wednesday, August 13th. Vale's dividend payout ratio (DPR) is presently 59.35%.

Vale Company Profile

(

Free Report)

Vale SA, together with its subsidiaries, produces and sells iron ore and iron ore pellets for use as raw materials in steelmaking in Brazil and internationally. The company operates through Iron Solutions and Energy Transition Materials segments. The Iron Solutions segment produces and extracts iron ore and pellets, manganese, and other ferrous products; and provides related logistic services.

Recommended Stories

Before you consider Vale, you'll want to hear this.

MarketBeat keeps track of Wall Street's top-rated and best performing research analysts and the stocks they recommend to their clients on a daily basis. MarketBeat has identified the five stocks that top analysts are quietly whispering to their clients to buy now before the broader market catches on... and Vale wasn't on the list.

While Vale currently has a Moderate Buy rating among analysts, top-rated analysts believe these five stocks are better buys.

View The Five Stocks Here

Discover the 10 Best High-Yield Dividend Stocks for 2025 and secure reliable income in uncertain markets. Download the report now to identify top dividend payers and avoid common yield traps.

Get This Free Report

Like this article? Share it with a colleague.

Link copied to clipboard.