Global leading online education technology platform

2U Inc. NASDAQ: TWOU stock has been a

pandemic benefactor as global stay-at-home mandates caused educational institutions to transition to online learning. As schools start to resume in-class learning and

COVID-19 vaccine rollouts accelerate, it’s a logical assumption that a return-to-normal would be bearish for 2U. However, the “new” normal will undoubtedly still include

remote work, learn,

engage, and

entertain lifestyle changes that students and consumers were forced to adapt to during the pandemic. The new normal has introduced students and professionals to learn-at-home and online education platforms, whether they like them or not. The safety, convenience, and efficiency of online learning has been experienced and many will stick around even after the pandemic passes. The markets may be overreacting to the perceived reversion in online learning platforms underestimating the affinity of the

digital nomadic nature of the Gen-Y and Gen-Z demographic. A reversion to the pre-pandemic growth trajectory would still imply higher prices. Prudent investors who believe education technology is a part of the new normal can consider opportunistic pullbacks in 2U for exposure.

Q4 2020 Earnings Release

On Feb. 11, 2021, 2Ureleased its fiscal four-quarter 2020 earnings report for the quarter ending in December 2020. The Company reported an earnings-per-share (EPS) loss of (-$0.06), excluding non-recurring items, versus consensus analyst estimates for loss of (-$0.09), a $0.03 beat. Revenues grew 31.9% year-over-year (YoY) to $214.29 million beating consensus analyst estimates for $208.24 million. Adjusted EBITDA improved to $18.8 million, up $13.8 million. 2U provided flat guidance for full-year 2021 with revenues estimated to come in between $910 million to $945 million compared to $911.70 million consensus analyst estimates. The Company sees a net loss between $165 million to $185 million and adjusted EBITDA in the range of $45 million to $65 million.

Conference Call Takeaways

2U Co-Founder and CEO, Chip Paucek set the tone, “We hear three common interconnected themes emerging in our conversations. First, a focus on better serving non-traditional working adult learners who are looking for both degree and non-degree offering across their careers and lives. Second, pressure to identify new and sustainable revenue streams at the same time institutions are facing inescapable budgetary and investment constraints. And third, growing demand on colleges and universities from business and government to do a better job aligning in-demand jobs and creating career-focused upskilling and reskilling pathways.” CEO Paucek provided examples including the recent partnership with the iconic 154-year old Morehouse College in scaling its digital transformation with an online degree completion program. The Company recently signed up Simmons University and The London School of Economics onto its platform. 2U supports boot camps at 44 different universities in 28 states covering over 75% of the total US population. The workforce engagement team hosted over 750 job-related events and spent 22,000 hours support job-seeking students.

Segment Growth

2U CFO, Paul Lalljie provided growth metrics for the quarter. Revenues grew 32% to $215.3 million. The Degree segment revenue totaled $130.5 million, up 21% YoY driven by higher student demand and improved retention rates. Alternative Credential Segment revenues grew 54% to $84.8 million, which included $52.8 million from Trilogy, which grew 54% YoY and short courses grew 47% YoY. Total 2020 annual revenues grew 35% YoY and 21% on an organic basis. The Company enrolled 99,000 new students and they are expected to continue to drive revenue in the future as enrolled students complete their programs. Typically, Total Full Course Equivalent (TFCE) enrollment came in at 80,650 composed of graduate programs and reskilling and upskilling courses with an average of two years or more for graduation. Lalljie summed it up, “We expect the progress we made in 2020 to be sustainable and we will continue to operate the business in a portfolio basis… the year-over-year revenue comparisons will show more substantial growth in the first half of 2021 than in the second.”

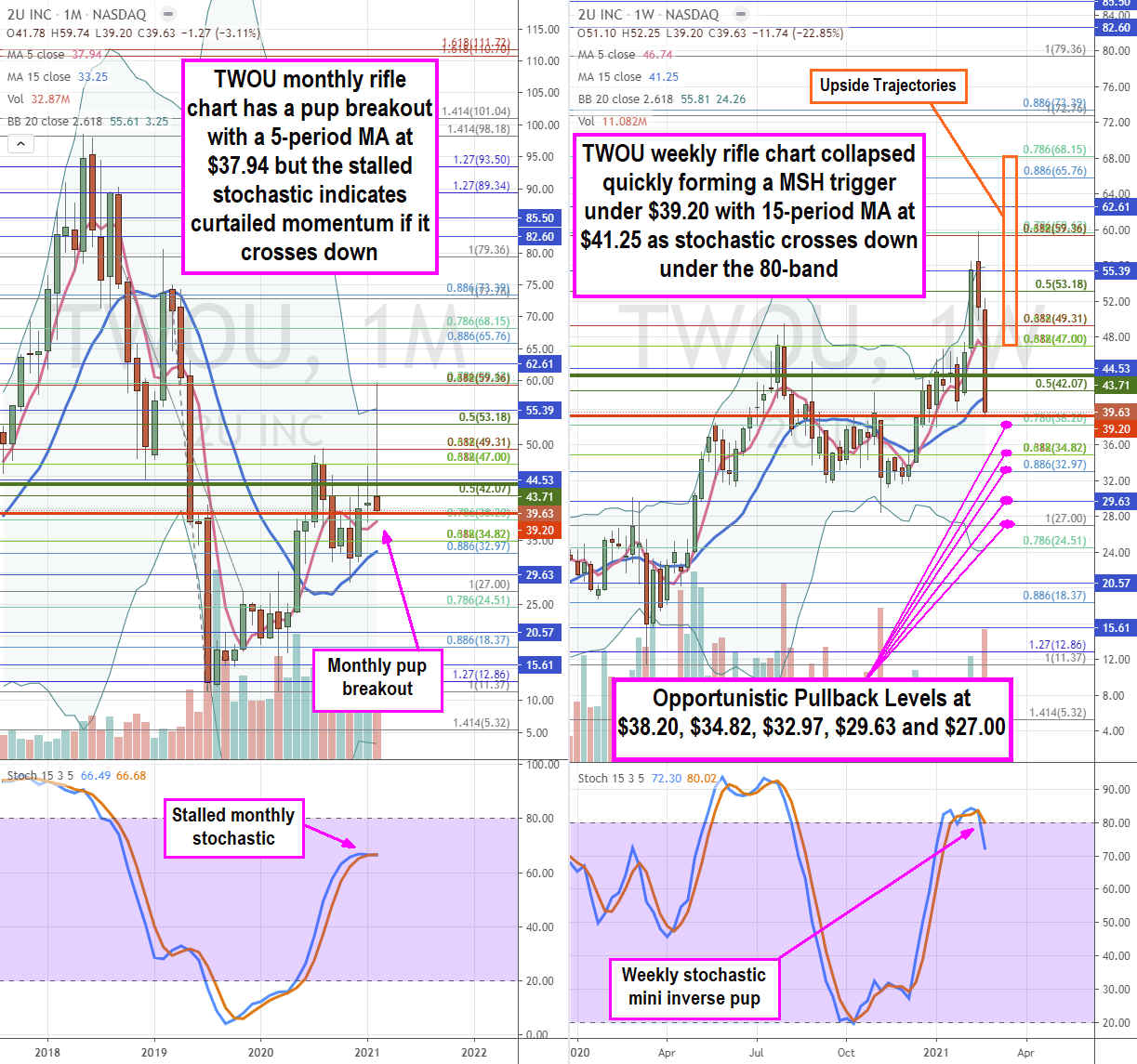

TWOU Opportunistic Pullback Levels

Using the rifle charts on the monthly and weekly time frames provides a full view of the price action playing field for TWOU stock. The monthly rifle chart formed a pup breakout causing shares to spike and peak off $59.56 Fibonacci (fib) level. The monthly 5-period moving average (MA) support is rising at the $39.20 fib but the monthly stochastic is stalling with the potential to cross down. It’s worth noting that the monthly upper Bollinger Bands (BBs) sit at $55.39. The most recent monthly market structure low (MSL) buy triggers above $43.71, but a looming weekly market structure high (MSH) sell trigger forms below $39.63. The weekly rifle chart uptrend has stalled as shares quickly collapsed below the 5-period MA at $46.74 and the 15-period MA at $41.25. The violent price drop caused the weekly stochastic collapse on a mini inverse pup through the 80-band. Risk-tolerant investors can look for opportunistic pullback levels at the $38.20 monthly 5-period MA/fib, $34.82 fib, $32.97 monthly 15-period MA/fib, $29.63 sticky 5s, and the $27.00 fib. The upside trajectories range from the $47.00 fib up to the $68.15 fib level. Keep an eye on peer Stride NYSE: LRN as these two stocks move together.

Before you consider 2U, you'll want to hear this.

MarketBeat keeps track of Wall Street's top-rated and best performing research analysts and the stocks they recommend to their clients on a daily basis. MarketBeat has identified the five stocks that top analysts are quietly whispering to their clients to buy now before the broader market catches on... and 2U wasn't on the list.

While 2U currently has a Hold rating among analysts, top-rated analysts believe these five stocks are better buys.

View The Five Stocks Here

Tesla, Nvidia, and Google helped shape the last era of market growth, but the next wave could come from a new group of companies. Inside this report, you’ll find 7 stocks that could play a major role in the next tech-driven market boom.

Get This Free Report

Like this article? Share it with a colleague.

Link copied to clipboard.