Boston Beer

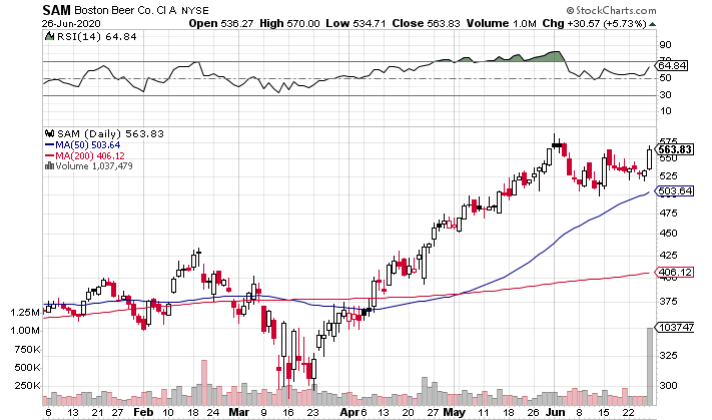

NYSE: SAM surged more than 5% on Friday on

more than 6x its average volume. After nearly doubling from mid-March to the end of May, shares spent most of June taking a breather.

Friday’s move indicates that Boston Beer could be ready for another leg up.

With nightlife unlikely to return to pre-pandemic levels anytime soon, can Boston Beer’s uptrend continue?

A Mixed Bag

Boston Beer reported revenue of $330 million in Q1 2020, up more than 31% yoy. However, net income dipped by $5.5 million to $18.2 million. The decrease was a result of higher operating expenses and lower gross margins.

Let’s start by looking at the top-line growth:

Depletions increased by 36% in Q1, with 30% of that coming from legacy brands and the other 6% from Dogfish Head, acquired in 2019. The Samuel Adams and Angry Orchard brands declined, but the Truly Hard Seltzer and Twisted Tea brands more than offset those declines.

Twisted Tea is set to see double-digit growth in 2020, an acceleration from 2019 growth rates. But Truly is the brand that is really shining for Boston Beer.

The hard seltzer market is on fire. According to IWSR, it now makes up over 2.5% of the total U.S. market for alcohol, tripling from a year ago. And as the #2 brand in the space (White Claw is #1), Truly is well-positioned to take advantage of this increase.

On the Q1 2020 earnings call, CEO David A. Burwick said, “we've got an opportunity to get trial among a lot of new consumers. 41% of the consumers that tried Truly in the last month were new to the brand.”

But all of this growth is coming at a price as Boston Beer is forced to rely on third-party brewers to help meet the soaring demand. Those contract brewers are more expensive. This partially explains Boston Beer’s Q1 2020 decrease in gross margin; it was 44.8%, down from 49.5% in Q1 2019.

Operating costs also contributed to the dip in net income, with advertising, promotional, and selling expenses increasing. The advertising and promotional expenses can be viewed as investments in Boston Beer’s brands though.

On the other hand, labor and safety costs jumped due to the pandemic.

Pandemic Impact on Demand

The pandemic has been another mixed bag for Boston Beer.

Its Samuel Adams and Angry Orchard volumes continued to decline, seeing outsized impacts from the on-premise shutdowns. Boston Beer acknowledges that it’s unlikely to return these brands to growth in 2020, but the company is working to position them for a better 2021.

On the other hand, restaurant and bar closures have not slowed the hard seltzer market’s momentum. According to Nielsen, Memorial Day weekend sales in the space increased by 250% yoy. This bodes well for demand for as long as pandemic-related restrictions last.

Valuation

SAM is trading at around 58x projected 2020 earnings and around 42x projected 2021 earnings. So a decent amount of growth is priced into the shares.

Boston Beer’s future share price depends largely on Truly. The hard seltzer market still comprises just 2.5% of alcohol sales; it still has a lot of room to increase. That said, Truly will face increasing competition going forward.

It’s hard to expect much from Samuel Adams and Angry Orchard. A stabilization of these brands’ revenue may be the most realistic expectation.

The bottom line, I think SAM is reasonably valued. It’s just not a screaming buy based on the fundamentals alone.

But the chart makes a short to intermediate-term play appealing…

Technicals

As touched on earlier, Boston Beer took off on Friday. It’s in striking distance of the all-time high it made at the end of May and appears ready to make fresh new highs.

The price action in June leading up to Friday was very bullish. Shares traded in a tight range on light volume for a few weeks; this reflected a widespread desire among long-term investors to hold on to their shares while the stock digested its gains from the previous two-and-a-half months.

The massive volume behind Friday’s move shows that there is a ton of demand for SAM shares. And since the stock is coming off its recent consolidation, the shares are not extended. This looks like an early opportunity to get into SAM – it could easily take off past $600 in the next week or two.

The Verdict

Buying and holding SAM stock is a little risky due to the mixed bag of fundamentals

But when you consider the sterling technicals, the shares become an attractive proposition. The best move on SAM is to get in now and put in a stop-order 5-10% below your entry-level. This way, you can ride this uptrend for as long as it lasts without being exposed to the risk that the Truly brand fails to meet expectations.

Before you make your next trade, you'll want to hear this.

MarketBeat keeps track of Wall Street's top-rated and best performing research analysts and the stocks they recommend to their clients on a daily basis.

Our team has identified the five stocks that top analysts are quietly whispering to their clients to buy now before the broader market catches on... and none of the big name stocks were on the list.

They believe these five stocks are the five best companies for investors to buy now...

See The Five Stocks Here

Enter your email address and we’ll send you MarketBeat’s list of ten stocks set to soar in Summer 2026, despite the threat of tariffs and what's happening in Iran. These ten stocks are incredibly resilient and are likely to thrive in any economic environment.

Get This Free Report