Winnebago Falls Hard After Earnings Smasher

Winnebago Falls Hard After Earnings Smasher

Winnebago (NYSE:WGO) is a pandemic horror-story for investors. The company is firing on all cylinders, producing sustained double-digit growth, and has a growing backlog to fuel business over the next year and yet the stock continues to fall. The fiscal Q4 report was chock full of great news and sent shares higher in early trading but for some reason, the short-sellers piled in hard and drove shares down more than 11%. Now, with the stock trading at a two-week low, the stock is setting up for a buying opportunity but there is a caveat. That opportunity is not here just yet.

Winnebago Blows Away The Consensus

Winnebago is no slouch when it comes to performance. The company brought in $737.81 million in revenue for the quarter or up 40% from last year. The increase in revenue is driven by a 15.3% increase in organic sales driven by strength in the higher-margin Towables segment. In terms of the analysts and their expectations, Winnebago beat the consensus by $14.92 million or about 2.0%.

Moving down the report, the gross margin increased 90 basis points. A combination of lower costs in the Motorhome segment and cost-leverage in Towables as offset by sales mix. EBITDA came in at $76.5 million or 30% above consensus and Operating Income is $68.4 million or up 52%. Finally, on the bottom line, GAAP EPS of $1.25 beat by $0.28 while Adjusted earnings of $1.45 beat by $0.52. Looking forward, the company backlog increased by high triple digits which ensures plenty of business in the year to come.

“We added motorized scale through the acquisition of Newmar and continued to grow our RV market share throughout the year by leveraging strong dealer relationships, exciting new products and record consumer interest. Winnebago Industries also generated expanded margins and stronger cash flows... Looking ahead, we enter our 2021 fiscal year with four premier brand platforms, strong operational momentum, a record backlog, and the financial flexibility to manage through the ongoing uncertainty in the environment,” said CEO Michael Happe.

Winnebago Pays A Safe Dividend

Winnebago pays a safe, if small, dividend worth about 0.84% yield with shares trading near $50. The company’s payout ratio is very low at 22% so nothing to worry about there but if you are looking for growth this may not be the place to get it. The company just upped the distribution last quarter and the cash flow is a little tight which leads me to think stability is the best to expect. The total debt is still very low at only 64% of equity but coverage is low and the leverage ratio is running near 6X. The company’s not in a bad position by any means but it’s using leverage to expand and may shy away from giving too much cash back to shareholders.

Winnebago Falls But The Analysts Still Love It

More than half the analysts covering Winnebago have a Strong Buy, Very Bullish, or Overweight rating on Winnebago. Within the last two months, there’ve been six bullish notes with three upgrades, and three target increases. The latest comes from CFRA which upped the target to $75 citing the rising backlog and strong demand trends.

“In short, we think the pandemic-driven RV boom has legs, as evidenced by YoY increases in its backlog to record levels (+219% for Towables and +536% for Motorhomes)," notes analyst Garrett Nelson on the report.

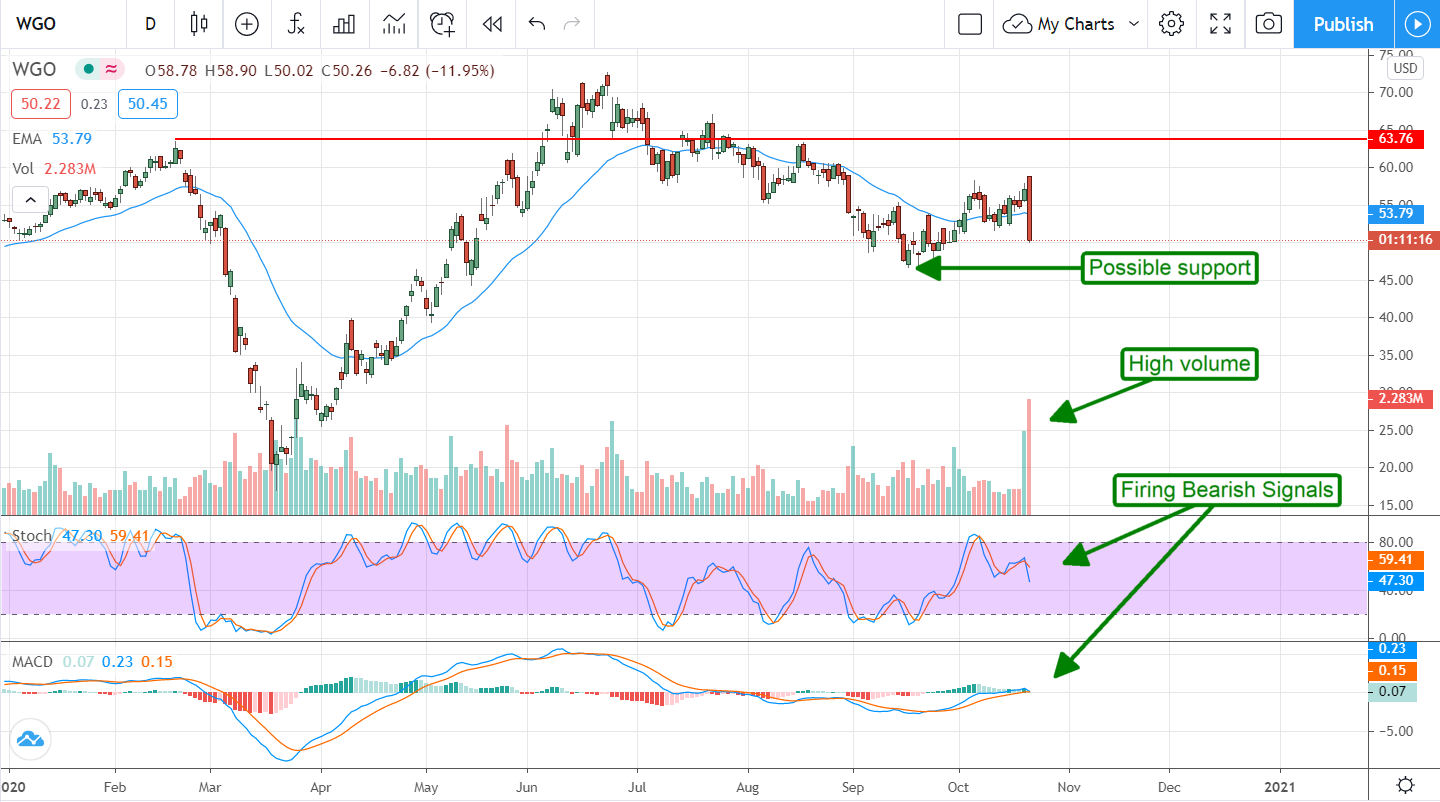

On a technical basis, today’s fall in share prices does not look good. The stock is forming a large Dark Cloud Cover that confirms the downtrend that began over the summer. On top of that, the indicators are bearish and set up to fire a strong, bearish, trend-following signal with high volume driving price action. I will be surprised if this stock doesn’t fall at least a little bit more. The next target for firm support is near $47, if price action falls below here this stock could fall another 5% to 10% below that level, or about 50% below the consensus target.

Before you consider Winnebago Industries, you'll want to hear this.

MarketBeat keeps track of Wall Street's top-rated and best performing research analysts and the stocks they recommend to their clients on a daily basis. MarketBeat has identified the five stocks that top analysts are quietly whispering to their clients to buy now before the broader market catches on... and Winnebago Industries wasn't on the list.

While Winnebago Industries currently has a Hold rating among analysts, top-rated analysts believe these five stocks are better buys.

View The Five Stocks Here

Tesla, Nvidia, and Google helped shape the last era of market growth, but the next wave could come from a new group of companies. Inside this report, you’ll find 7 stocks that could play a major role in the next tech-driven market boom.

Get This Free Report

Like this article? Share it with a colleague.

Link copied to clipboard.