Crocs

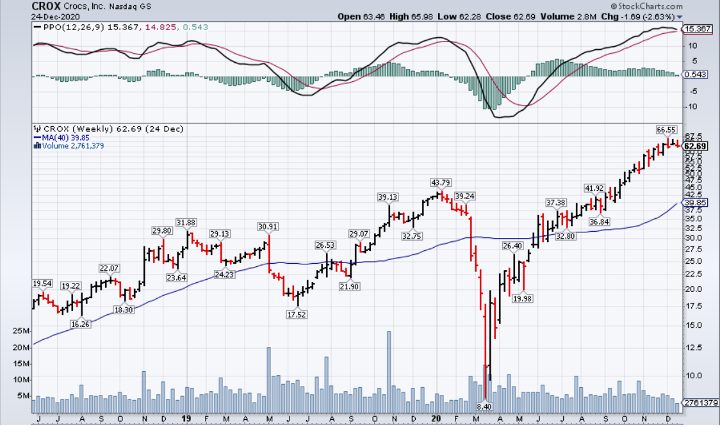

NASDAQ: CROX, a footwear company best known for selling foam clog shoes, was trading at $38 a share in mid-February. Fears of a pandemic-induced slowdown sent shares down to $8 by mid-March.

But Crocs roared all the way back to over $30 a share by late-May and has been basing between $30 and $36 over the past month.

Retailers have been particularly hard-hit by the pandemic. Physical stores have been closed in COVID hot spots, and a combination of social distancing requirements and fear have led to reduced foot traffic in open stores.

But Crocs has been able to buck the trend. NPD Group, a market research firm, tracks 30 footwear brands. Crocs was the only one to grow sales in March 2020 and one of only two that grew sales in April 2020.

So how has Crocs managed to pull this off?

Online Presence

Crocs has invested in its e-commerce business for years, and that investment has paid off with people opting to (or forced to) shop online.

During the Q1 2020 earnings call, CFO Anne Mehlman said, “We continued to see strong double-digit e-commerce sales growth of 15.8% on top of 16.5% growth last year. This represents our 12th consecutive quarter of double-digit e-commerce growth. Digital revenue as a percentage of total revenue, which includes crocs.com and marketplaces reported as e-commerce and our e-tail revenue included in our wholesale channel, was 30.1% in the first quarter, as compared with 25.4% in the same period last year.”

Another indication of Crocs’ strong online presence – April Google searches of the brand hit a 15-year high.

While Crocs’ online business remains strong, the company has been a mixed picture regionally.

Americas and Asia

Overall, Crocs had Q1 2020 sales of $281.2 million, down 5% yoy and down 3.3% on a constant-currency basis.

Weakness in Asia was largely responsible for the decrease, as Asia revenues were $65.5 million, down 28.1% yoy. But on the Q1 earnings call, the company pointed out that China and Korea sales are improving week-over-week, providing optimism for Q2 and beyond.

A strong performance in the Americas was able to partially offset the weakness in Asia. Q1 revenue was $147.7 million, up 14.4% yoy. Retail comps were up 23.3% prior to the shutdown in March, which bodes well in a post-pandemic environment (whenever that happens).

Cutting Costs

Forced closures, social distancing requirements, and a reluctance to go into public areas has put pressure on Crocs’ 367 physical locations.

To blunt the impact of declining revenue, Crocs has made moves to cut costs.

The company has reduced salaries, hiring, marketing programs, and discretionary expenses for 2020. It now expects SG&A to be $440 to $460 million for the year. This is $30 to $50 million lower than 2019, and $100 million lower than originally planned for 2020.

Furthermore, Crocs is carefully managing its working capital, evaluating existing inventory and future orders for potential savings. The company cut expected capital expenditures to around $30 million, roughly half of its previous guidance.

Valuation

With all of the coronavirus-related uncertainty, Crocs is not providing full guidance for the remainder of 2020. However, investors shouldn’t be too spooked, as Crocs’ e-commerce business should enjoy continued strength in the “new-normal” environment. Revenue at brick-and-mortar locations is more of a question mark, but the worst of the pandemic seems to be behind us, and Crocs’ global presence should allow it to withstand a slowdown in areas where cases flare up.

Crocs trades at around 22x 2021 projected earnings, an attractive valuation for a growing company, particularly in the current market.

But is now the right time to get into Crocs?

Technicals

As mentioned earlier, Crocs has made some very sharp moves over the past few months. Over the past month, it has been range-bound between ~$30 and ~$36 a share. Shares have had low volatility within this range and volume has been light, a good sign after such a big price move.

You have two potential entry points:

- A pullback to the low $30s on light volume would bring shares to the 200-day moving average. The 50-day moving average could be on the verge of a cross-over by the time that happens, a bullish signal. On top of that, the low $30s represent support as the bottom of the current base.

2. A breakout above $36 on high volume would also be a good buying opportunity. For this scenario, I’d like to see the stock consolidate for a little longer at these levels. Shares may need more time to digest

Before you make your next trade, you'll want to hear this.

MarketBeat keeps track of Wall Street's top-rated and best performing research analysts and the stocks they recommend to their clients on a daily basis.

Our team has identified the five stocks that top analysts are quietly whispering to their clients to buy now before the broader market catches on... and none of the big name stocks were on the list.

They believe these five stocks are the five best companies for investors to buy now...

See The Five Stocks Here

Click the link to see MarketBeat's list of seven stocks and why their long-term outlooks are very promising.

Get This Free Report