Good News In Darden Restaurant’s Q4 Report

Darden Restaurants (NYSE: DRI) is far from being a pandemic winner but it is on track to be a recovery winner and the Q4 results prove it. While business is still hurting, there are numerous signs within the report that business is improving, accelerating, and about to return to growth. What we find most interesting, however, is the mix between eat-at-home and eat-away spending. The number of eat-at-home customers is holding fairly steady across the company’s network while the number of eat-away customers continues to grow. If this trend holds up over the next year Darden Restaurants could easily see its volume return to pre-COVID levels and more.

Darden Revenue Accelerates, Guidance Is Positive

Darden Restaurants is the parent company of Olive Garden, Longhorn Steakhouse, Cheddar’s Scratch Kitchen and a handful of smaller brands with restaurants across America. Revenue in the FQ3 period, calendar December 2020 through February 2021, came in at $1.76 billion or down about 26.4% but it beat the consensus by a wide margin. The 600 basis point beat was driven by better than expected comps, down 26.7% versus 31.2%, aided by the addition of new stores. On a brand basis, Olive Garden fell -25%, Longhorn fell 12%, the fine dining establishments fell 45%, and Other fell 37%.

Moving down the report, the margin was hurt by COVID-related costs and many of them are going to stick. The company is not only issuing bonuses for its workers but wage increases are going to be kept and accelerated over the next several years. Regardless, the $0.98 is down 48% from last year but beat the consensus by more than a quarter proving just how resilient the business is. Because this is the fourth quarter since the pandemic began affecting the company the comps will get better as we move forward.

The guidance is also very encouraging. The company is expecting revenue to accelerate again, to $2.1 billion, bringing the volume back to near-pre-COVID levels and up 65% from last year. Earnings are expected in the range of $1.60 to $.170 versus the $1.25 expected and we think both the revenue and EPS estimates are cautious. The rebound isn’t fully underway but it will be soon, once it begins in earnest we think that economic activity is going to erupt. The QTD results underscore that idea. Comp-store sales turned positive across the network before the end of the first month. Comps are led by LongHorn Steakhouse which not only went positive first but is up 23% the week ending 3/21.

Darden Resumes Dividend Payments, Starts Buyback

Darden Restaurants resumed paying a dividend only a quarter after cutting it out but the initial payouts were small. The newly declared distribution is $0.88 per share or equal to the pre-COVID level putting the company back on track as a dividend-grower. The $0.88 payout is worth 2.4% with shares trading at $146 and may get increased again next year, if not sooner. The payout ratio is 90% of F2021 earnings which is a small bother but that’s only on a rear-looking basis. The forward outlook is much better at only a 50% payout ratio and this may be a high-ball estimate if the company is able to outperform this year. In addition to the dividend increase, the company also initiated a $500 million buyback program worth about 3.0% of the market cap.

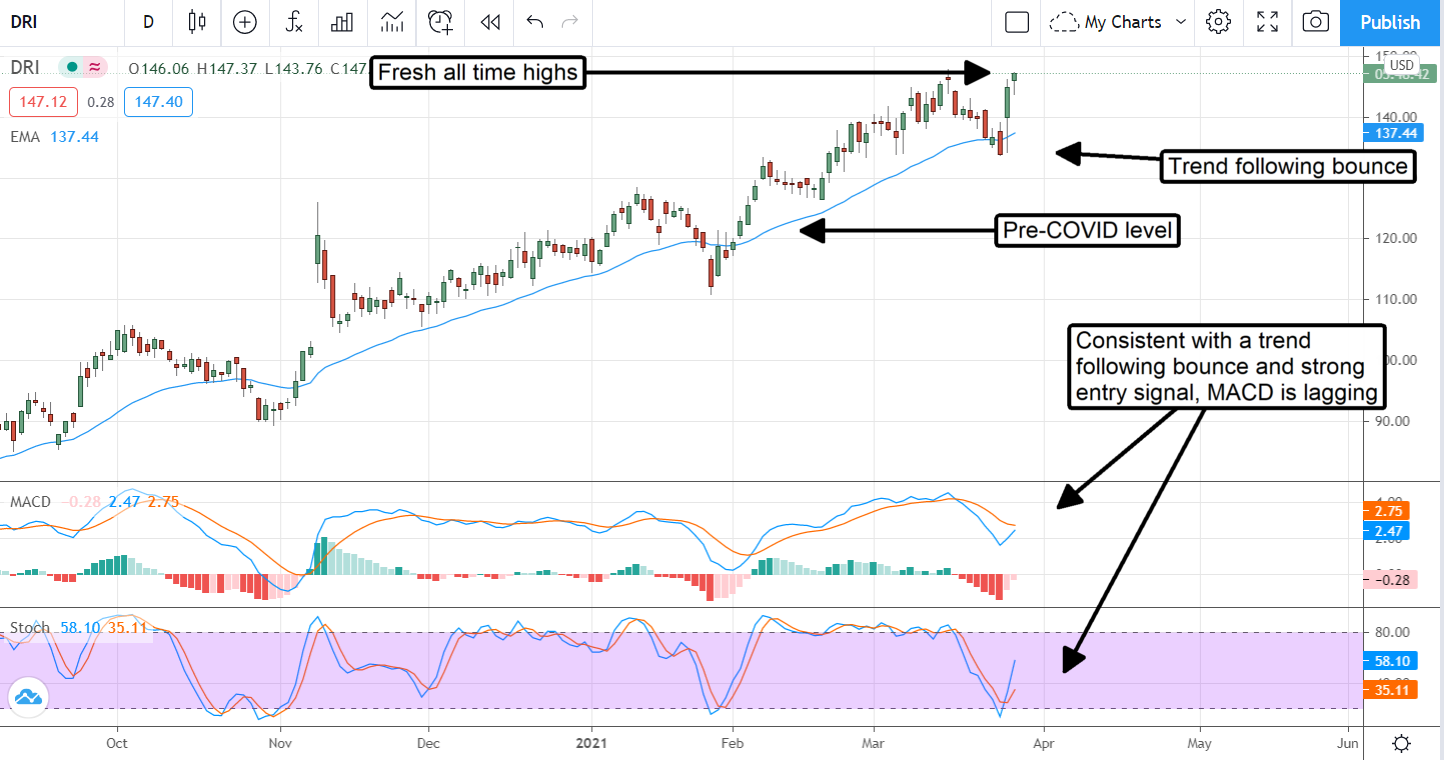

The Technical Picture: Darden Restaurants Ready To Break Out

Darden Restaurants has been able to stage a pretty decent rebound despite the tough headwinds for business. Now the stock is trading up against resistance at what happens to be an all-time high and looks ready to break out. A break to new highs would be very bullish and could take the stock up as much as 10% to 35% over the next quarter.

Before you consider Darden Restaurants, you'll want to hear this.

MarketBeat keeps track of Wall Street's top-rated and best performing research analysts and the stocks they recommend to their clients on a daily basis. MarketBeat has identified the five stocks that top analysts are quietly whispering to their clients to buy now before the broader market catches on... and Darden Restaurants wasn't on the list.

While Darden Restaurants currently has a Moderate Buy rating among analysts, top-rated analysts believe these five stocks are better buys.

View The Five Stocks Here

Discover the next wave of investment opportunities with our report, 7 Stocks That Will Be Magnificent in 2026. Explore companies poised to replicate the growth, innovation, and value creation of the tech giants dominating today's markets.

Get This Free Report

Like this article? Share it with a colleague.

Link copied to clipboard.