Retail department store chain

Kohl’s Corporation (NYSE: KSS) stock disappointed investors by falling short on both earnings and guidance on its fiscal Q1 2022 earnings report. Shares of the

retailer had previously remained at a premium as the Company has stated its intent to explore strategic alternatives and rumors of a $62 buyout price have been floating around. However, the nasty fiscal Q1 2022 earnings performance caused shares to

collapse as interest from suitors appears to have been diminished temporarily largely due to lack of financing.

Simon Property Group NYSE: SPG has squashed any rumors of its interest in a buyout. The retailer has suffered from

supply chain disruption, logistics, and

inflationary pressures as sales growth went negative in the quarter. Shares are trading at less than 6.5X forward earnings with a 5%

dividend yield. The Company has noted that

sales demand has improved in May and is still awaiting fully financed binding proposals from potential suitors in the coming weeks. Prudent investors that have been patiently waiting for opportunistic pullback levels can watch to scale into a position down here with a potential for acquisition as an added bonus.

Q1 Fiscal 2021 Earnings Release

On May 19, 2022, Kohl’s released its fiscal first-quarter 2022 results for the quarter ending April 2022. The Company reported an adjusted earnings-per-share (EPS) profit of $0.11 excluding non-recurring items versus consensus analyst estimates for a profit of $0.70, missing estimates by (-$0.59). Revenues fell by (-4.4%) year-over-year (YOY) to $3.71 billion beating analyst estimates for $3.69 billion. Kohl’s CEO Michelle Gass stated, “The year has started out below our expectations. Following a strong start to the quarter with positive low-single digits comps through late March, sales considerably weakened in April as we encountered macro headwinds related to lapping last year’s stimulus and an inflationary consumer environment. We remain committed to our long-term strategy and are encouraged that our updated store experience, with Sephora at Kohl’s shops, delivered positive comparable store sales across these 200 locations for the quarter. We continue to expect our business to improve as the year progresses, with growth in the second half as we benefit from the roll out of 400 additional Sephora stores, enhanced loyalty rewards and further investment in our stores.”

Strategic Alternatives

The board will continue to explore strategic alternatives. CEO Gass commented, ““Regarding our review of strategic alternatives, we continue to engage with multiple interested parties. We have formally communicated the specific procedures for the submission of actionable bids due in the coming weeks. We continue with our detailed diligence phase and are pleased with the number of parties who recognize the value of our business and plan.”

Lowered Full-Year 2023 Guidance

Kohl’s raised its fiscal full-year 2023 EPS guidance to $6.45 to $6.85 versus $7.15 consensus analyst estimates, down from prior guidance range of $7.00 to $7.50. The Company sees revenue growth of 0 to 1% YoY growth, down from 2% to 3% or $18.47 billion to $18.66 billion versus $18.92 billion analyst estimates.

Conference Call Takeaways

CEO Gass started off addressing the “unusual amount of attention and speculation” in regard to potential acquisition from suitors. She underscored the commitment of the Board to run the sales process with the shareholders’ best interest in mind. The Board is awaiting fully financed binding proposals with multiple engaged parties in the coming weeks. She noted how the quarter started off strong but fell sharply due to macro headwinds from inflationary pressures as last years stimulus was lapped. However, they have seen trends improve in May as weather turned favorable to accelerate demand for its spring products. The first quarter suffered a (-5%) sales decline led by Children’s and Home businesses. The Home business was a top benefactor during the pandemic, so a reversion can be expected. While Home business was up 30% last year, it declined (-17%) in the quarter and accounts for 15% of total sales. The Company expects demand to continue to be weak but will continue to leverage its pricing elasticity to remain competitive. The Childrens business is expected to recover through the year as seasonal weather resumes. The Sephora store within a store partnership is strong and as the Company expects to expand them to 600 locations. The Company expects sequential improvements in Q2 and positive growth to resume in the second half of 2022.

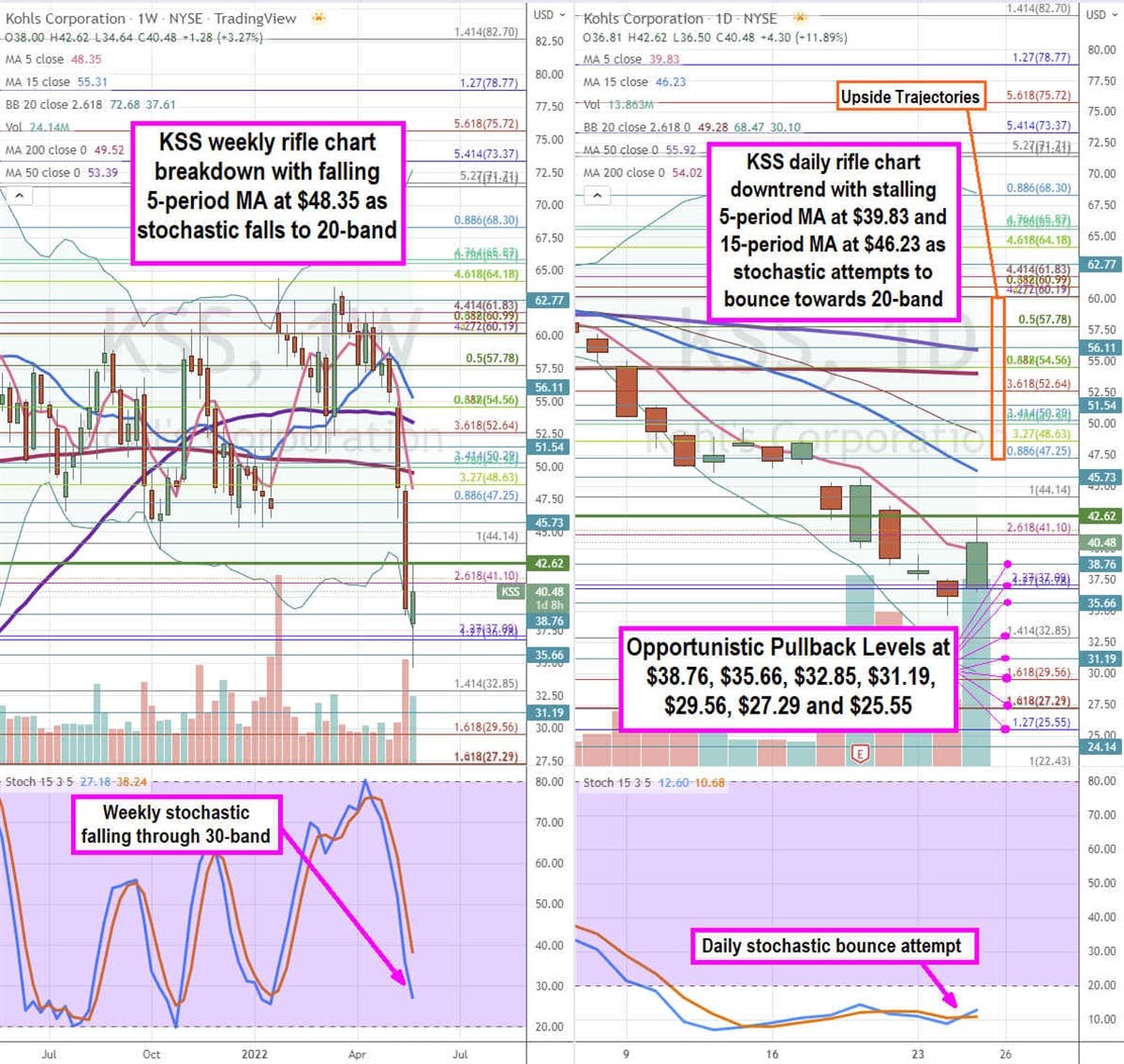

KSS Opportunistic Pullback Levels

Using the rifle charts on the weekly and daily time frames provides a precision view of the landscape for KSS stock. The weekly rifle chart peaked out around the $64.18 Fibonacci (fib) level. Shares collapsed through the weekly lower Bollinger Bands (BBs) at $37.61 on the earnings release. The weekly downtrend has a falling 15-period moving average (MA) at $48.25 under the 200-period MA at $49.52 and 50-period MA at $53.39 followed by the 15-period MA at $55.31. The weekly stochastic oscillation is falling below the 30-band. The daily rifle chart has a downtrend with a flattening 5-period MA at $39.83 and 15-period MA falling at $46.23 with daily 200-period MA flat at $54.02. The daily stochastic is attempting to coil back up again off the 10-band. The daily market structure low (MSL) buy triggers above $42.62 breakout. The daily lower BBs sit at $30.10. Prudent investors can look for opportunistic pullback levels at the $38.76, $35.66, $32.85 fib, $31.19, $29.56 fib, $27.29 fib, and the $25.55 fib level. Upside trajectories range from the $47.25 fib level up towards the $60.19 fib level.

Before you make your next trade, you'll want to hear this.

MarketBeat keeps track of Wall Street's top-rated and best performing research analysts and the stocks they recommend to their clients on a daily basis.

Our team has identified the five stocks that top analysts are quietly whispering to their clients to buy now before the broader market catches on... and none of the big name stocks were on the list.

They believe these five stocks are the five best companies for investors to buy now...

See The Five Stocks Here

The AI wave will soon hit public markets with Anthropic and OpenAI set to go public later this year. However, you don't have to wait to invest. This report shows seven AI stocks that you can buy today while the big model providers get ready to go public.

Get This Free Report

Like this article? Share it with a colleague.

Link copied to clipboard.