PepsiCo Today

$150.08 +5.37 (+3.71%) As of 04:00 PM Eastern

- 52-Week Range

- $127.60

▼

$177.50 - Dividend Yield

- 3.79%

- P/E Ratio

- 27.34

- Price Target

- $158.25

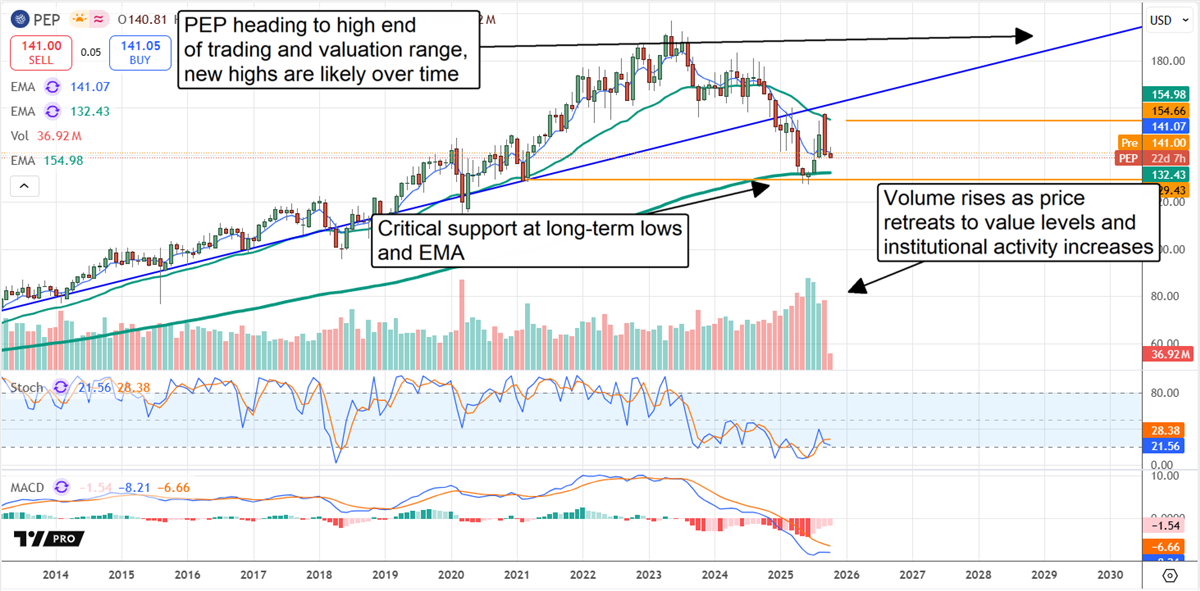

PepsiCo’s NASDAQ: PEP deep discount will soon evaporate because the stock price is disconnected from reality, and the FQ3 earnings report supports this.

Trading at approximately 17x the current year’s earnings outlook and 11x the 2035 forecasts, the stock is at the low end of its historical range and set up for a cyclical rebound that could more than double its price over the next few years.

Historical averages put PepsiCo stock closer to a 25x valuation, with the high-end above 30x, where it will likely reach before the upcoming cycle is completed.

This is a look at why.

PepsiCo’s Diversified Model Sustains Growth, Acceleration Expected

PepsiCo’s FQ3 results prove the strength and resiliency of its diversified model. The company posted 2.7% systemwide growth, outpacing MarketBeat’s consensus by a slim margin, with strength in the core beverage and international markets driving it. Segmentally, PepsiCo Foods North America was the weakest, with a 3% organic contraction, while most others posted low- to mid-single-digit organic growth. PepsiCo Beverages North America grew by 2%, led by a 5.5% and 4% gain in the EMEA and Latin America segments. Portfolio reshaping was also cited as a business driver.

The margin news is also favorable to shareholders and the stock price outlook. The company experienced margin pressure as expected, but not as severe as feared, leaving operating income down by only 1.5% and adjusted earnings down by 2%. The critical details are that the earnings and cash flow were sufficient to sustain the company’s financial health while returning capital to shareholders, and the guidance forecast is optimistic.

PepsiCo’s FQ4/FY guidance isn’t spectacular, forecasting only a low-single-digit organic revenue increase and slightly narrower margin, but it has two things going for it. The first is that the 2025 results align with the capital return outlook, which forecasts $8.6 billion in returns this year, and the second is that management is focused on accelerating growth, including increased pipeline innovation, improved operational quality, and ongoing portfolio optimization.

PepsiCo’s Capital Return Is Reliable for 2026

PepsiCo Dividend Payments

- Dividend Yield

- 3.80%

- Annual Dividend

- $5.69

- Dividend Increase Track Record

- 54 Years

- Dividend Payout Ratio

- 103.64%

- Recent Dividend Payment

- Sep. 30

PEP Dividend HistoryPepsiCo’s capital return includes its dividend and share repurchases. The dividend annualizes to over 4% in early October 2025 and is expected to grow annually.

PepsiCo is a Dividend King, with over 50 years of consecutive annual dividend increases. The risk for investors is that the pace of distributions increases or that share buybacks slow.

As it stands, the company runs a mid-single-digit distribution CAGR and reduces the share count by approximately 0.5% each year.

The balance sheet is in good shape, although debt is increasing in 2025. That aside, assets and equity are also growing, with equity up by nearly 8% year to date, and leverage remains low. Long-term debt is less than 2.5x the equity and 1x the assets, leaving the consumer staples business in a flexible financial position.

Institutions Have Been Buying PepsiCo in 2025, Setting It Up to Rebound

The institutional activity aligns with PepsiCo’s 2205 price action, suggesting a market bottom. Institutions have bought robustly each quarter of 2025, including the first week of Q4, netting well over $2 in shares for each $1 sold. They provide solid support due to this activity and the ownership rate, which exceeds 70% of the stock. Investors might expect this trend to continue through year-end, potentially not slackening until PEP moves above the $155 level and the mid-point of the long-term trading range.

The stock price action is bullish following the release, indicating support at the bottom of the long-term trading range. Assuming the market follows through on the signal, it is set to begin rebounding soon and is likely to enter an uptrend before the year’s end. The stock price will move up to the critical resistance level near $155 in this scenario and may continue to rise if the global economic outlook does not deteriorate.

Before you consider PepsiCo, you'll want to hear this.

MarketBeat keeps track of Wall Street's top-rated and best performing research analysts and the stocks they recommend to their clients on a daily basis. MarketBeat has identified the five stocks that top analysts are quietly whispering to their clients to buy now before the broader market catches on... and PepsiCo wasn't on the list.

While PepsiCo currently has a Hold rating among analysts, top-rated analysts believe these five stocks are better buys.

View The Five Stocks Here

Nuclear energy stocks are roaring. It's the hottest energy sector of the year. Cameco Corp, Paladin Energy, and BWX Technologies were all up more than 40% in 2024. The biggest market moves could still be ahead of us, and there are seven nuclear energy stocks that could rise much higher in the next several months. To unlock these tickers, enter your email address below.

Get This Free Report

Like this article? Share it with a colleague.

Link copied to clipboard.