Home Depot reported revenue and EPS growth this morning and yet shares are down more than -5.0%. The home improvement company beat consensus for EPS but missed revenue estimates by a small margin. Even so, it was not the top and bottom lines that have the stock on the move. Home Depot reported weak comps and gave a poor outlook for the 4th quarter and that has investors flocking to the doors. With Lowes on deck to report earnings on Wednesday, the Home Depot results raise a serious question about what investors can expect.

Home Depot; The Good, The Bad, and The Ugly

While the news did not please investors, the Home Depot report isn't all bad. The problem with the stock is a case of over-zealous expectations in a market desperate for growth.

Home Depot, The Good – The good parts of Home Depot's Q3 report include revenue growth, comp store growth, transaction growth, and ticket average growth. The company says revenue grew 3.5% over the last year and driven by a 3.6% increase in comp-store sales. Comp-store sales were impacted by a 1.5% increase in transactions compounded by a 1.9% increase in ticket average. The addition of four new stores is also a plus.

Home Depot, The Bad – While revenue and comps increased the company still fell shy of estimates. The 3.5% revenue growth missed by more than 100 basis points due to lower than expected comp-store growth and rising costs. Home Depot's 3.6% increase in comp-store sales is a full 100 bps below consensus and that weakness is compounded by tighter margins. Gross margin fell -30 bps and operating margins 20 bps as lumber-price weakness cuts into profitability.

Home Depot, The Ugly – The 3Q results are not so bad until you factor in how they will impact the full-year results. According to Home Depot's management, that impact will not be good. The company lowered its full-year guidance for the second time due to the 3Q weakness. Revenue growth is now expected in a range near 1.8%, down 50 bps from last quarter and 150 bps from earlier this year. At the same time, comps are now expected in the range of 3.5%, down from 4% last quarter and 5.0% earlier in the year.

What Home Depot's Results Mean For Lowe's

The lackluster results at Home Depot point to weakness in Lowe's results too. This is especially important to note because both home improvement retailers received a number of positive analysts’ calls in the two weeks prior. A miss for Lowe's could spell doom for the stock price.

Oppenheimer

"As we consider carefully forthcoming Q3 reports from HD and LOW, we very much expect results and commentary to increasingly reflect a building benefit of now lower mortgage rates. HD represents one of the world's best-run retailers. We tend to prefer the LOW investment story, given an opportunity for margin improvement under new leadership."

Credit Suisse

"We believe that LOW offers a compelling risk/reward over the next 12 months, with relative valuation vs. its closest peer near its trough level, low near-term expectations, modestly improving industry demand and multiple sales/margin levers,"

Barclays

Barclays raised Lowe's to Overweight from Equal Weight citing increased confidence the company will build on its momentum going into 2020. The new price target is $125.

Piper Jaffrey

Analyst Peter Keith upgraded Lowe's to Outperform from Neutral with a price target of $130 or 12% upside from current levels. Keith says the company's fundamentals looked poised to accelerate in the 2nd half yet “expectations seem modest”.

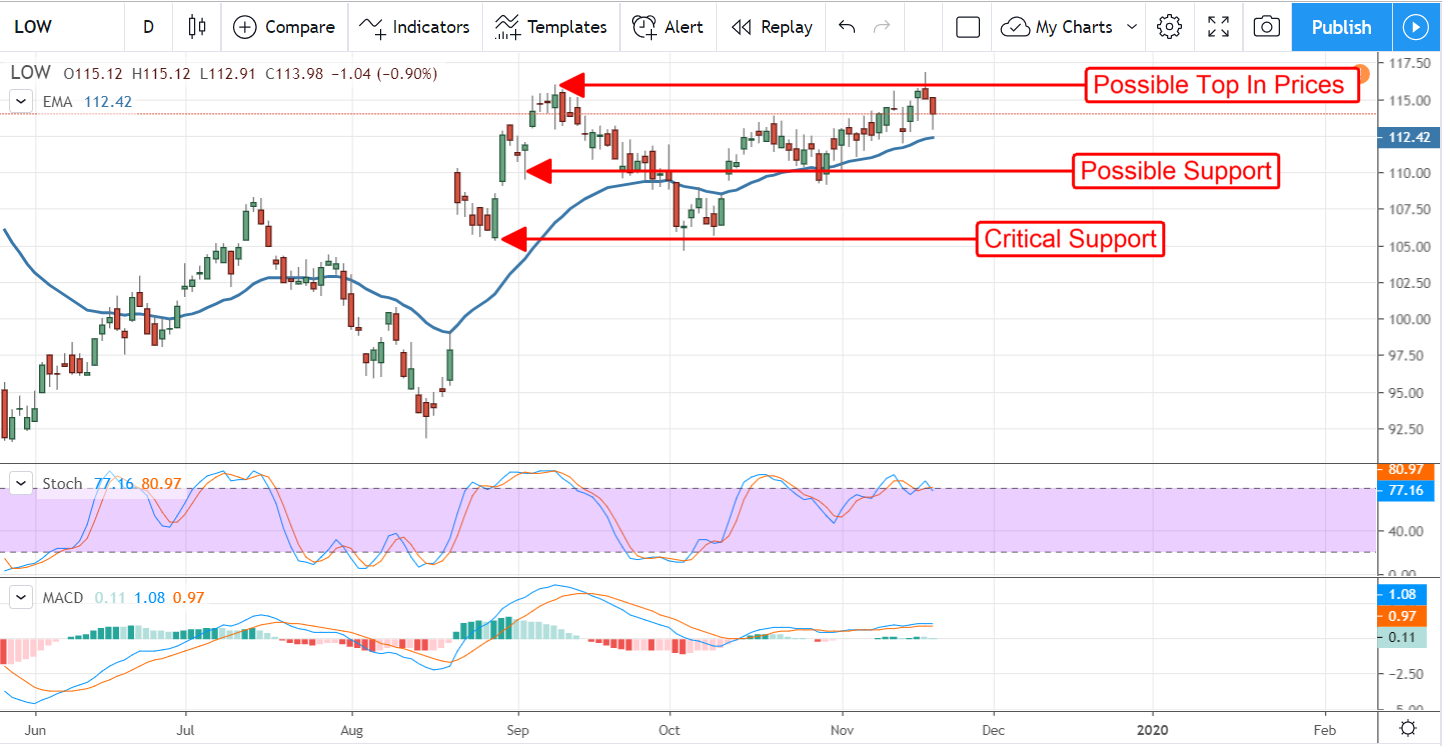

The Technical Outlook Is Mixed

To say the technical outlook is mixed is an understatement. The analysts seem to think that Lowe's is going to outperform in the 2nd of the year and yet results from Home Depot point to less-than-stellar results. The chart set up echoes this uncertainty with shares of LOW struggling with resistance at the $115 level. A look at the chart shows a stock on the brink of reversal, a reversal that may begin in earnest following Lowe's 3Q earnings release on Wednesday morning.

Investors looking to get into the Lowe's momentum story may find it advantageous to wait until after earnings are released. A miss is likely to provide a cheaper entry-point into this 1.9% yielding Dividend Aristocrat. Support targets at $110 and $105 appear to have strength, a fall below $105 could see this stock plummet another 20%.

Before you make your next trade, you'll want to hear this.

MarketBeat keeps track of Wall Street's top-rated and best performing research analysts and the stocks they recommend to their clients on a daily basis.

Our team has identified the five stocks that top analysts are quietly whispering to their clients to buy now before the broader market catches on... and none of the big name stocks were on the list.

They believe these five stocks are the five best companies for investors to buy now...

See The Five Stocks Here

Wondering what the next stocks will be that hit it big, with solid fundamentals? Click the link to see which stocks MarketBeat analysts could become the next blockbuster growth stocks.

Get This Free Report

Like this article? Share it with a colleague.

Link copied to clipboard.