Using the MarketBeat Retirement Calculator

Every investor's goal is a comfortable retirement. The MarketBeat retirement calculator is a dynamic tool that you can use to calculate how much you'll need to invest each year to meet your retirement goals based on current investments. If you still need to start investing for retirement, the retirement savings calculator can also tell you how much you'll need to save to catch up based on your goals.

How the Retirement Calculator Works

The MarketBeat calculator uses a series of data points to assess current savings and decide how you'll need to invest to achieve your goals.

Begin by inputting a few personal details about your age, the age you wish to retire and how much you can afford to invest a month. You'll also input data on your current investments, the average annual rate of return on the investments you select and withdrawal rates during retirement. The MarketBeat calculator allows you to input unique values or use the standard average 6% annual return and 4% annual withdrawal rate during retirement.

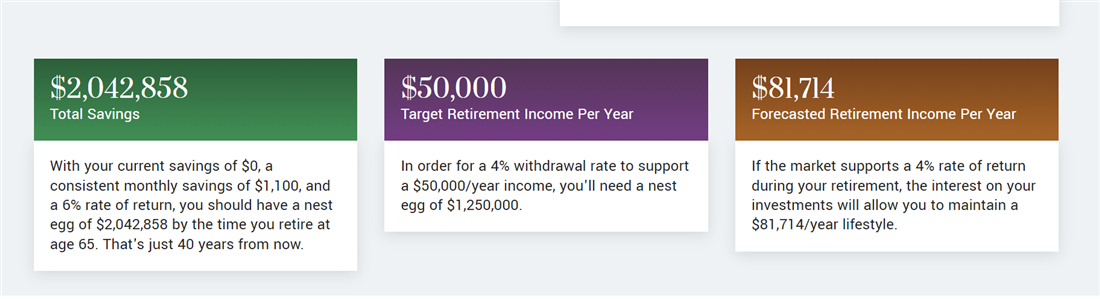

Examples of Retirement Calculations

Let's use the MarketBeat retirement calculator to help you answer the question, "How much do I need for retirement?" Imagine you're 25 and want to retire at 65 with $2 million in assets. Assuming standard returns and use of funds, the retirement calculator tells us you'd need to invest at least $1,100 monthly throughout your career to reach your goal.

Image text: Investing $1,100 a month as a 25-year-old will leave you with about $2 million in assets by the time you reach retirement age.

To illustrate the importance of investing early, let's calculate how much a 45-year-old employee will need each month to meet the same goal. With no savings or investments, this employee has 20 fewer years to invest than the person in our previous example. You'd need to invest $4,500 per month at this age to retire at age 65, and you'd still have more than $40,000 less than the younger investor by the time you stop working.

Image text: A 45-year-old investor will need to invest at least $4,500 per month to retire with $2 million in assets.