Paychex's NASDAQ: PAYX stock price declined following its fiscal Q4 earnings report, as macroeconomic headwinds, hiring woes, cautious guidance, and acquisition hurdles weighed on the price action.

However, those same macroeconomic headwinds and hiring woes have yet to be reflected in the jobs data, which is a leading indicator for Paychex's business. Labor market trends, including the non-farm payrolls report and weekly jobless claims, suggest that labor markets are not only improving compared to last year but also accelerating as the year progresses.

Paychex Today

$97.62 +1.33 (+1.38%) As of 02:32 PM Eastern

This is a fair market value price provided by Massive. Learn more. - 52-Week Range

- $85.45

▼

$148.76 - Dividend Yield

- 4.88%

- P/E Ratio

- 21.51

- Price Target

- $105.67

If this strength continues, Paychex's business quality is all but assured, suggesting its high-yielding dividend and share buybacks are safe and reliable for long-term buy-and-hold investors. Trading near long-term lows, Payx stock offers a historically high yield of nearly 5%, compounded by share buybacks.

Share buybacks are aggressive, offsetting the cost of annual increases in distributions with quarterly reductions in the share count. Trailing 12-month activity reduced the count by an average of 1.1% as of fiscal Q2, a pace that is expected to continue.

There is some risk with the dividend payment, as it is a relatively high percentage, approximately 85% of the earnings. However, the more significant metric is cash from operations, which more than covers the distributions and share buybacks, leaving room for reinvestment and balance sheet maintenance.

The balance sheet is healthy, though it reflects the impact of last year’s debt-financed Paycor acquisition. Positive cash flow will enable debt reduction over time, though, and the Paycor acquisition underpins the growth outlook.

Paychex Fiscal Q2: Stronger Than It Looks

Paychex had a solid fiscal Q2, with revenue growing by more than 12.5% to over $1.60 billion. The as-expected figure appears to be a tepid showing. However, with nearly 100% of analysts lowering the targets after the prior report, the bar was set low.

Paychex results were better than the low end, where whisper targets were set. Within this, the core Management Solutions segment led, up 14%, including an 8% acquisitional impact, while the PEO segment increased by 8%. Strength was underpinned by increased headcounts and money per end-user employee.

Margin news was also good, despite the tepid comp to consensus estimates. The company improved margin throughout its stack, driving a 17% increase in adjusted operating earnings. Critical details included earnings per share, which came in at $1.32, slightly above the consensus forecast and 75 bps above expectations.

Guidance was another mixed bag, with revenue expected to align with consensus. However, at 5.5%, revenue growth is present and will be compounded by accelerated earnings growth. Adjusted earnings are forecasted to grow by 8%, and may come in above forecasts.

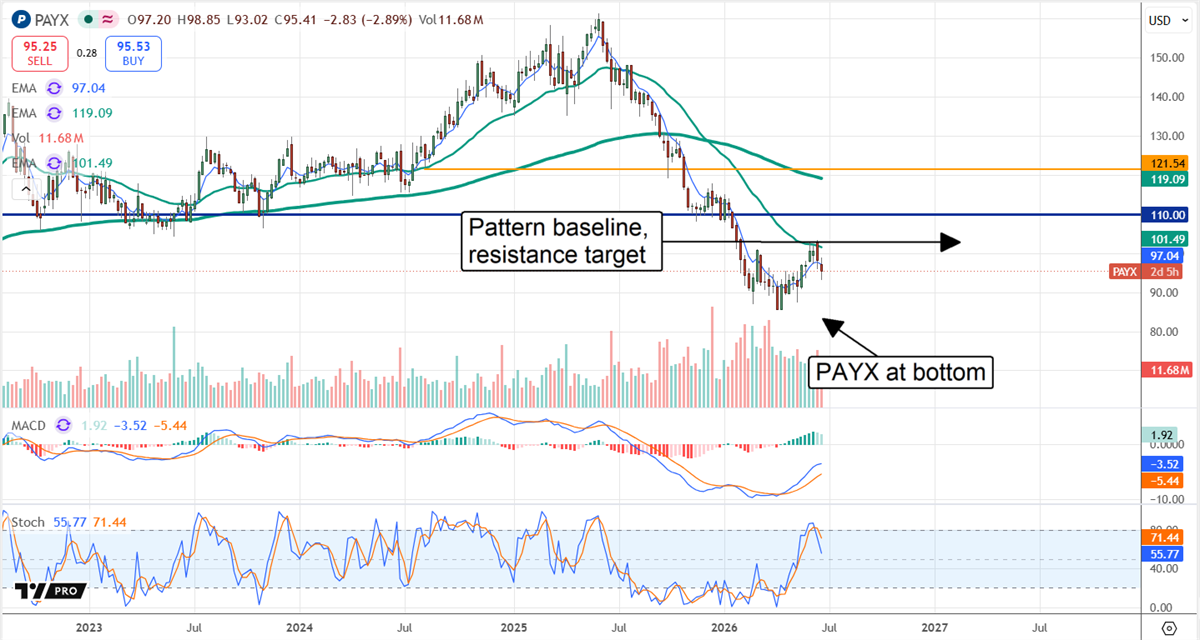

Institutional Activity Underpins Paychex Stock Price Bottom

2026’s chart price action reflects potential for a bottom, also seen in the institutional data. Price action aligns with a Head & Shoulders pattern, while institutions, which collectively own nearly 85% of the stock, have been accumulating shares and ramping up activity. The likely outcome is that they continue to support this market at its current levels, setting the stage for a complete market reversal later this year.

Analysts are among the catalysts for this stock, with the group's trends contributing to the stock price decline over the trailing 12 months, including significant reductions in price targets. The risk is that they continue to pressure the market lower, but that seems unlikely, given the institutional activity. The more likely scenario is that analyst trends, which peg the stock as a consensus Hold, remain steady, limiting downside as the year progresses. As it stands, the consensus of 17 analysts is just over $105, sufficient to place this market above its critical resistance target.

The critical resistance target is just under $103. It aligns with the latest high, the baseline for this pattern. Assuming a new high is set and sustained, the next move will be upward, potentially reaching the $117 level in the near term. Long-term, this stock should see a full price recovery. The low price discounts a healthy growth outlook, putting it at pennies on the dollar relative to its 2030 forecast.

Before you consider Paychex, you'll want to hear this.

MarketBeat keeps track of Wall Street's top-rated and best performing research analysts and the stocks they recommend to their clients on a daily basis. MarketBeat has identified the five stocks that top analysts are quietly whispering to their clients to buy now before the broader market catches on... and Paychex wasn't on the list.

While Paychex currently has a Hold rating among analysts, top-rated analysts believe these five stocks are better buys.

View The Five Stocks Here

Enter your email address and we’ll send you MarketBeat’s list of ten stocks set to soar in Summer 2026, despite the threat of tariffs and what's happening in Iran. These ten stocks are incredibly resilient and are likely to thrive in any economic environment.

Get This Free Report