As an investor, you already know what stocks are and how they work. But when you buy stock in a particular company, did you know that you sometimes have a choice between what type of stock to buy?

So what is the difference between common stock and preferred stock, anyway, and what is preferred stock? Preferred stock provides certain benefits as a shareholder that common stock doesn't.

By the end of this article, you should understand what preferred stocks are and how they differ from common stocks.

What is Preferred Stock?

Preferred stock is a capital stock issued by a corporation with a higher claim on assets and dividends than common stocks.

Unlike common stock, preferred shares typically do not carry voting rights, and their dividends are usually paid at a set rate, although they can be subject to some adjustment. In the event of liquidation, preferred stockholders have priority over the common stockholders in terms of claims on assets. So what are preferred securities? The terms "preferred shares," "preferred stock" and "preferred securities" are often used interchangeably.

How Does Preferred Stock Work?

Preferred stock provides investors with certain advantages that common stock does not. Unlike common stock, preferred shares usually have a fixed dividend rate paid before the dividends of common stockholders. The dividend rate also doesn't fluctuate with the market and can be higher than the dividend rate of common stocks. Preferred shareholders will also have priority over common shareholders in terms of claims on assets in the event of liquidation. They typically don't have voting rights but can sometimes receive voting privileges if certain conditions are met. Because of these benefits, preferred stocks generally trade at a premium compared to common stocks of the same company, which makes them a more secure investment option if you're seeking a lower level of risk.

However, some drawbacks are associated with investing in preferred stocks since they tend to be more expensive than common stocks and come with less liquidity (it can be difficult to sell them when needed).

And suppose company management decides it needs additional funds for operations or expansion projects. In that case, it usually has the right to redeem outstanding shares of its preferred stock without prior notification or approval.

Why Do Companies Issue Preferred Shares?

Preferred shares provide companies with several advantages. First, by issuing preferred stock, a company can raise money without increasing its debt load by selling bonds or other debt instruments. Preferred stockholders are typically entitled to regular dividend payments, which can help attract investors. For the company, since dividend payments must be paid out before any money can go to shareholders with common stock, it ensures that debt and other obligations will be taken care of first.

Types of Preferred Stock

Preferred stock is classified into two categories: prior and preference preferred. Within those categories, preferred stock can have other characteristics.

Prior Preferred Stock

Prior preferred stockholders are the most senior class of equity and have priority within a company's capital structure, meaning they will be paid ahead of other classes of securities if the company goes bankrupt. Preference preferred stocks usually come with special privileges such as the right to convert their shares into common shares. They also have rights to additional payments from the corporation before common shareholders receiving any distributions.

Preference Preferred Stock

Preference preferred stockholders are higher in the pecking order than common shareholders but lower than prior preferred shareholders.

Convertible Preferred Stock

Convertible preferred stock allows the holder to exchange their shares for a different type of investment, usually common stock at any time. In a way, this makes them the opposite of callable shares, which gives the offering company the option to buy back the shares at a fixed price. The conversion ratio determines how many common shares are given in exchange for each convertible preferred share. This ratio is usually set at the time of the initial issuance but can be changed by the company later on.

Cumulative Preferred Stock

Cumulative preferred stock guarantees holders will receive any missed dividends before common stockholders if the company does not distribute enough funds to pay all investors in full. For example, suppose a shareholder holds preferred shares that guarantee a $6 dividend.

Still, the company does not pay the dividend for three consecutive years, in the fourth year when the company is in a position to issue a dividend. In that case, these shareholders must be paid $24 ($6 x 4) before any dividend goes to common stockholders.

Noncumulative Preferred Stock

Noncumulative preferred stocks are similar to cumulative stocks, except they don't guarantee holders will receive any missed dividends before common shareholders receive theirs if there isn't enough money available for distribution. Noncumulative holders still have priority over common holders when receiving payments in bankruptcy or liquidation scenarios.

Participating Preferred Stock

If certain performance-related targets are met, such as revenue or profitability goals, participating preferred stockholders may be entitled to extra dividends, even if the company cannot afford to pay dividends to other shareholders.

How is Preferred Stock Different from Common Stock?

Common stock is strictly an equity investment. The value of a common share is based exclusively on the market. The dividend yield is also subject to fluctuation if the stock pays dividends. Owners of common stock have voting rights at shareholder meetings.

By contrast, preferred stock has equity elements but behaves more like a bond. For example, every share of preferred stock has a face value like a bond. The dividend yield of preferred stock, generally higher than that of common shares, is a percentage of this face value. In this way, the market value of a preferred stock share only reflects the stock's value in the marketplace. So preferred stock may have a higher face value than its market value. In exchange for this guaranteed dividend payment, preferred stock owners often forfeit voting rights in most scenarios.

Examples of Preferred Stock

Nowadays, preferred stocks are more commonly issued by banks (such as some of those on the list below) than by other industries since they tend to be highly regulated and require constant access to capital markets to operate effectively.

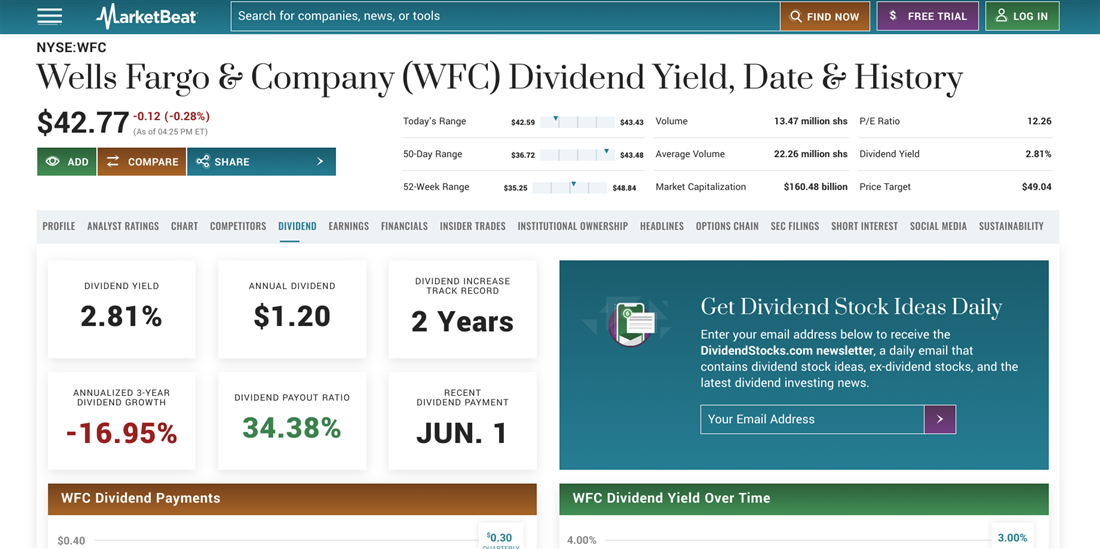

It is noncumulative and perpetual, meaning that the dividends will continue unless suspended by the company. The shares boast a liquidation preference of $1,000 per share. Each Series L Preferred Stock share can convert into 32.0513 Wells Fargo common stock shares. Shareholders have no voting rights except under a few limited conditions.

Suppose the closing price of the common stock exceeds 130% of the conversion price for 20 trading days during any consecutive 30-trading-day period, including the last day of such period. In that case, the company may convert some or all of the preferred stock to common stock.

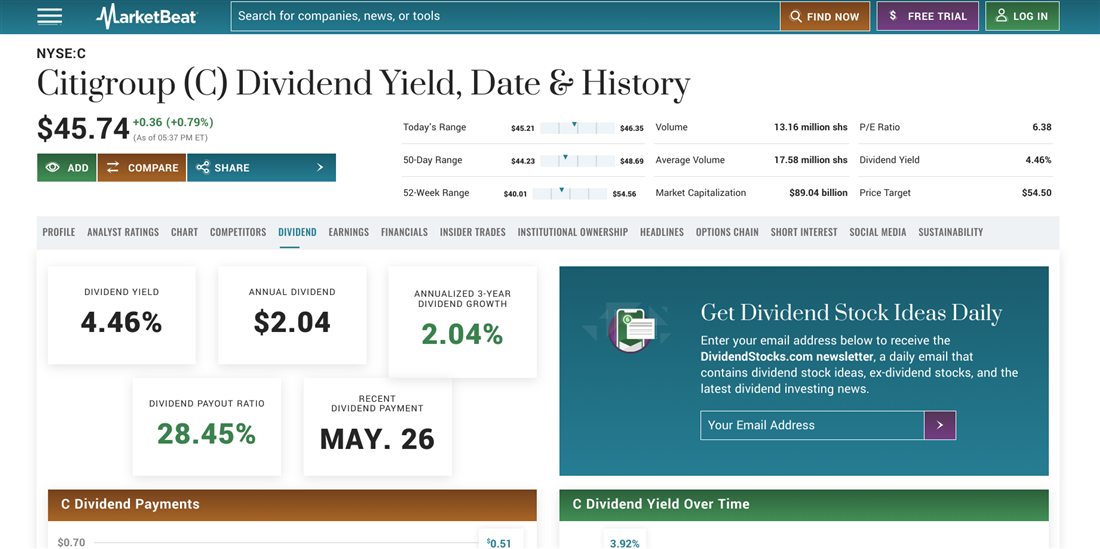

Citigroup Inc. NYSE: C also offers multiple types of preferred stock, such as a perpetual 5.950% Fixed Rate/Floating Rate Noncumulative Preferred Stock, Series A. The stock has a liquidation preference of $25,000 per share. Citigroup will pay quarterly Citigroup dividends at a rate of 5.950% for the first ten years and, after that, an annual rate equal to the three-month London Interbank Offered Rate (LIBOR) plus 4.068%. This is also higher than the dividend for common stock, shown below.

The shares are callable after 10 years at the company's preference. Stockholders don't have voting rights except in limited circumstances.

Who Should Invest in Preferred Stock?

Institutional investors purchase almost all preferred stock. The primary reason is that the Internal Revenue Service offers United States corporations a dividend received deduction. That said, preferred stock options might be a suitable investment if you're looking for a steady stream of income but aren't interested in taking on the risk of common stocks. Preferred stock offers reliable, predetermined dividend payments and the potential for capital gains. This makes it appealing if you want to diversify your portfolio and generate passive income.

If you have a lower appetite for risk, you might gravitate toward preferred stock, as its dividends are often higher than those offered by bonds, and its price tends to remain relatively stable. Furthermore, preferred stocks can come with various perks and privileges. However, preferred stock can be tougher to sell, or it may be able to be called by a company. Another thing to remember is that corporations typically issue preferred shares on either end of the credit spectrum.

If you're buying from a company with an excellent credit rating, there is less risk of not receiving your dividend payment. However, if a company has a poor credit rating, you could find your expected dividend payments suspended indefinitely.

Preferred Stock: A Choice Preferred by Some

Preferred stock is one of many options companies have to raise capital. Though preferred stock differs from common stock in certain ways, including priority in claims against assets and fixed dividend payments, it still offers many advantages and risks associated with owning stakes in a company. It can also offer attractive yields even during low-interest rate environments, which may make it the right option for you, depending on your circumstances.

FAQs

To help you with any further questions, we've compiled a list of FAQs to help answer some common concerns regarding preferred stock.

What is preferred stock in simple terms?

What is a preferred stock, exactly? The preferred stock definition is that it's a type of equity security that has features of both stocks and bonds. It allows you as an investor to have partial ownership in a company and gives you the right to receive dividends and the potential for capital gains or losses. It typically has a higher priority than common stock regarding dividend payments. As a holder, you may even be able to convert preferred shares into common stock.

Is it better to buy common or preferred stock?

Some investors like preferred stock more than common stock. The greatest advantage of owning preferred stock is its relative stability compared to common stocks, which are less impacted by market volatility.

However, it tends to be more expensive than common stock since the value of the dividend payments usually offsets most price fluctuations. Also, depending on the issue's terms, company management may have the right to redeem outstanding shares without prior notification or approval, which could result in a loss of income or capital gains. And since the market for preferred stock is relatively small, it is considered a less-liquid investment. Always research or consult a financial advisor before making any stock purchase.

What is preferred stock with an example?

Preferred stock is a type of equity security with stocks and bonds features. One example of a company that issues preferred stock is Wells Fargo. This stock offers you the chance to acquire ownership stakes in the company by purchasing preferred shares, which offers you the right to receive dividend payments at a set rate and first claim to assets in the case of bankruptcy.

Continue following MarketBeat

Add MarketBeat as your preferred source on Google to see our latest stories in your feed.

Before you make your next trade, you'll want to hear this.

MarketBeat keeps track of Wall Street's top-rated and best performing research analysts and the stocks they recommend to their clients on a daily basis.

Our team has identified the five stocks that top analysts are quietly whispering to their clients to buy now before the broader market catches on... and none of the big name stocks were on the list.

They believe these five stocks are the five best companies for investors to buy now...

See The Five Stocks Here

Click the link to see MarketBeat's list of seven stocks and why their long-term outlooks are very promising.

Get This Free Report

Like this article? Share it with a colleague.

Link copied to clipboard.