But what is a Roth IRA, how does a Roth IRA work, and what types of assets can you invest in through your account? Our crash course on Roth IRA account options will help you learn more.

What is a Roth IRA?

A Roth IRA is an individual retirement account that allows individuals to save for retirement while avoiding taxes on their earnings and withdrawals. Opening a Roth IRA is relatively simple, and you can invest in many of the same assets as a 401(k) account. Roth IRAs also have tax benefits like a 401(k), and you can maintain both accounts simultaneously.

How does a Roth IRA work?

The Roth IRA, named after Senator William Roth Jr., is a powerful tool for building retirement savings. But how does it work, and is it right for you? Let's investigate the fundamentals and see if you should open a Roth IRA.

Eligibility and contribution limits

Unlike traditional IRAs, which offer immediate tax deductions for contributions, Roth IRAs utilize a different approach. You contribute with post-tax dollars, meaning there is no upfront tax benefit. However, this seemingly disadvantageous strategy unlocks a powerful perk, the perk of tax-free withdrawals in retirement. This can significantly boost your retirement nest egg compared to taxable accounts.

You must meet specific income requirements and have earned income to contribute to a Roth IRA directly. In 2024, the contribution limit for individuals under 50 is $7,000, rising to $8,000 for those 50 and above. For 2024, the income limits are different. Single filers are ineligible to contribute to a Roth IRA if their income is above $161,000, and joint filers are ineligible if their income is above $240,000.

If your income exceeds the direct contribution threshold, consider the "backdoor Roth IRA" strategy. This involves first contributing to a traditional IRA, which may be tax-deductible depending on your income and then converting it to a Roth IRA after a five-year waiting period. This allows you to benefit from tax-free growth and withdrawals even if your income disqualifies you from direct contributions. However, consulting a tax professional is crucial to ensure this strategy aligns with your financial situation and tax implications.

Tax-free growth and withdrawals

Roth IRAs offer a unique advantage: tax-deferred growth. Unlike traditional IRAs, where your earnings are taxed upon withdrawal, Roth IRAs allow your money to compound tax-free, significantly boosting your retirement nest egg.

The magic of the Roth IRA becomes apparent once you reach the age of 59 1/2 and have held your Roth IRA for at least five years. You can access both your contributions and accumulated earnings, all tax-free. This provides exceptional flexibility and freedom, allowing you to tap into your retirement savings without tax burdens.

However, be mindful of early withdrawals before reaching 59 1/2. While exceptions exist for qualified expenses like first-time home purchases or unforeseen medical needs, premature withdrawals generally incur penalties and taxes on earnings. Treat your Roth IRA like a dedicated retirement fund and let your money work its tax-free magic until you reach that withdrawal age.

Roth vs. traditional IRA: Choosing the right fit

Traditional IRAs offer immediate tax gratification because contributions reduce your taxable income in the year you make them, effectively lowering your current tax burden. However, this comes at the cost of deferred taxation because your retirement withdrawals will be taxed as income.

Roth IRAs, on the other hand, embrace a "pay now, reap later" philosophy. Contributions are made with post-tax dollars, offering no immediate tax benefit. However, the magic lies in the tax-free growth and withdrawals in retirement. This can be incredibly advantageous if you anticipate your tax bracket being higher in the future. Think of it as prepaying your taxes at a potentially lower rate, allowing your retirement savings to grow unfettered by future tax burdens.

Ultimately, the optimal choice depends on your circumstances and tax projections. Traditional IRAs are ideal if you're in a high tax bracket now and expect to be in a lower bracket in retirement. Conversely, Roth IRAs shine for those who anticipate higher tax brackets later or simply desire tax-free access to their retirement funds.

Who benefits most from a Roth IRA?

Roth IRAs excel in specific situations, making them attractive to certain investor profiles. Here's a breakdown of who stands to benefit most:

- Young earners: For those in the early stages of their careers with anticipated income growth, Roth IRAs are a potent tool. Locking in tax-free growth now can significantly boost their retirement nest egg compared to a taxable account. The longer their money compounds tax-free, the greater the advantage.

- High earners: Individuals already in a high tax bracket can leverage Roth IRAs to secure tax-free growth and withdrawals in retirement. This effectively prepays taxes at their current, potentially higher rate, allowing their retirement savings to flourish unburdened by future tax increases.

- Long-term investors: Roth IRAs shine for those committed to a long-term investment horizon. While the immediate tax benefit is absent, the tax-free growth and withdrawals down the line provide substantial advantages. Remember, patience is vital as the magic of tax-free compounding unfolds over time.

Roth IRAs provide a powerful tool for strategic investors seeking to maximize their retirement savings. By understanding the tax implications and aligning them with your circumstances and financial goals, you can unlock the true potential of this valuable retirement vehicle.

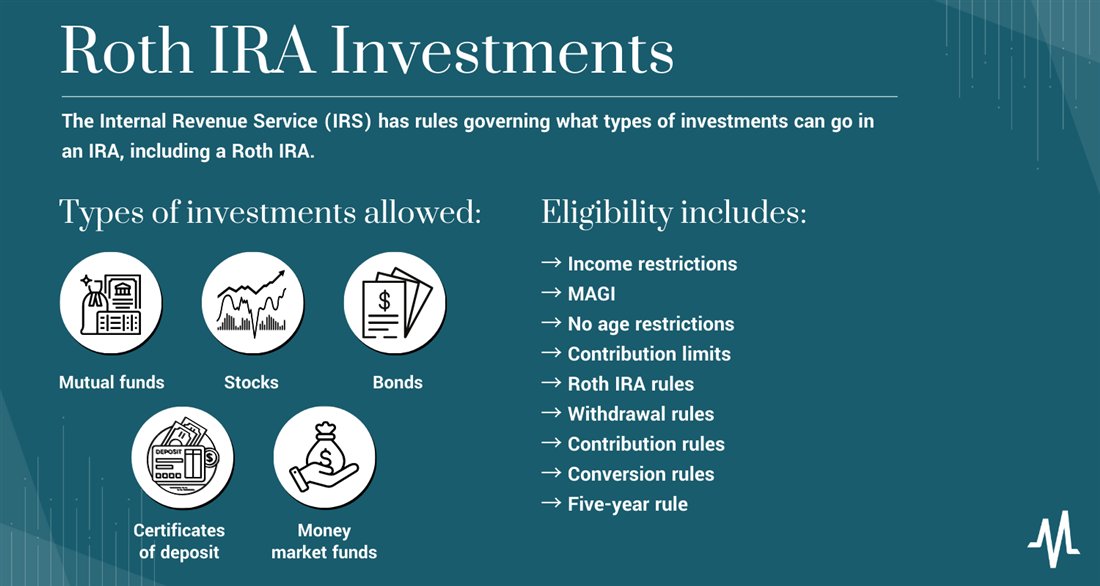

Types of investments allowed in a Roth IRA

The Internal Revenue Service (IRS) has rules governing what kinds of investments can go in an IRA, including a Roth IRA. In addition to IRS rules, individual custodians may also have Roth IRA investment restrictions. The following are some of the most common assets you can invest in after learning how to open a Roth IRA.

Mutual funds

A mutual fund is an investment vehicle that pools money from multiple investors to purchase a portfolio of stocks, bonds or other securities. A professional portfolio manager manages the funds, investing the money according to the fund's goal.

Stocks

Stocks are individual company ownership shares trading on major exchanges. Some Roth IRA account providers allow you to invest in individual shares of stock through your IRA rather than through a mutual fund investment. While buying shares of stock doesn't include the fees you'll see with mutual funds, it also exposes your retirement funds to additional risk.

Bonds

A bond is a fixed-income investment in which an investor loans money to a borrower (like a company or government entity) for a set period. In exchange, the borrower pays the investor interest at a predetermined rate and promises to repay the principal (the loan's original amount) when the bond matures. Bonds are more stable Roth IRA investments when compared to mutual funds and stocks because they hold a guaranteed value.

Certificates of deposit (CDs)

When comparing an IRA to a CD, it is important to understand the difference between the two. A CD is a savings account that typically offers a fixed interest rate and a fixed investment term. When you open a CD, you agree to keep your money deposited in the account for a period ranging from a few months to several years. In exchange, the CD provider releases the CD with interest when it matures. CDs are another option for a low-risk investment, as they are FDIC-insured up to $250,000 per depositor per insured bank.

Money market funds

Money market funds are mutual funds that invest in short-term, low-risk securities, such as government bonds, certificates of deposit and commercial paper. A money market fund aims to provide investors with a stable, low-risk investment option that offers higher returns than a traditional savings account or checking account.

|

Account type

|

Traditional IRA

|

Roth IRA

|

|

Maximum contribution for 2024

|

$7,000 with $1,000 in catch-up contributions

|

$7,000 with $1,000 in catch-up contributions

|

|

Tax benefits

|

Deduct contributions the year you make them from federal income

|

Take distributions tax-free

|

|

Required distributions

|

Begin at age 73

|

None

|

Eligibility for a Roth IRA

To be eligible to contribute to a Roth IRA, you must meet certain income requirements. If you do not meet the requirements to open a Roth IRA because your income is too high, you may be able to use a backdoor Roth IRA to circumvent income limitations.

Income restrictions

Roth IRA income limits for 2024 are based on your household's modified adjusted gross income (MAGI). Your MAGI is your annual gross income with select tax credits and deductions applied.

If your MAGI is less than $146,000 as a single filer, you can contribute up to the total amount to your Roth IRA, up to $7,000 or $8,000 if you're age 50 or older. You can only contribute a partial amount if your MAGI is between $146,000 and $161,000. Beyond $161,000, you are no longer eligible to open a Roth IRA. Beyond $161,000, you are no longer eligible to open a Roth IRA. However, you can still use a traditional IRA to gain immediate tax benefits.

|

MAGI

|

Roth IRA contribution eligibility

|

|

Less than $146,000

|

Fully eligible

|

|

$146,000 to $161,000

|

Partial contribution

|

|

Greater than $161,000

|

Not eligible

|

You may circumvent IRA income limits using a backdoor Roth IRA strategy. During a backdoor Roth transaction, an investor opens a traditional IRA, makes deposits into the account and then converts the account to a Roth IRA. There may be penalties associated with opening a backdoor Roth IRA, so consult with a professional versed in your financial situation before opening an account.

No age restrictions

There are no age restrictions on Roth IRAs, nor are you required to take money from the account at any point. Unlike traditional IRAs, which have a requirement to start taking distributions at age 72, Roth IRAs have no age limit for contributions or withdrawals.

Contribution limits

Contribution limits on Roth IRAs are the same as traditional IRAs. You will qualify to contribute up to $7,000 annually if you're under 50 and up to $8,000 past age 50. Your contribution limit will reduce proportionally if your MAGI is more than $146,000 annually for single filers or $230,000 for married filing jointly. You can use this Roth IRA calculator from MarketBeat to estimate your Roth returns over time.

Roth IRA rules

Tools like our MarketBeat retirement calculator can help you calculate the amount of money to divert to each tax-advantaged account to get the most out of your retirement funds. Before you learn how to start a Roth IRA and start allocating funds to each investment, familiarize yourself with the following IRA contribution and withdrawal rules and regulations.

Withdrawal rules

Unlike a traditional IRA, you do not have to take withdrawals from your Roth IRA past age 73. However, you will face penalties similar to those of a traditional IRA if you withdraw from your account early.

When you turn 59 1/2, you can begin taking withdrawals from your account without penalties. If you withdraw money before this age, you may pay an early withdrawal fee of up to 10%.

Contribution rules

There are few contribution rules when choosing assets for an IRA. Depending on the account's custodian, you can invest in everything from stocks trending in the media to mutual funds and even gold with specialized providers. Note these asset options before you decide where to open your IRA.

Conversion rules

An IRA conversion involves transferring funds from a traditional IRA or a pre-tax retirement account, like a 401(k), into a Roth IRA. Converting these funds will allow you to avoid paying taxes when you make withdrawals according to IRA rules. Remember, anything converted will be taxed as normal income.

No income limits exist on converting a traditional to a Roth IRA. However, if you are converting funds from a pre-tax retirement account, you must meet the eligibility requirements for contributing to a Roth IRA. There is also no limit on the total amount of funds you can convert if you prepare for the tax implications. Consider consulting with a tax professional to learn more about how you'll save in retirement versus converting funds now.

Five-year rule

The five-year rule determines whether you qualify for tax-free distributions from a Roth IRA. To qualify, both of the following must be true:

- You're at least age 59 1/2

- Your first contribution to the account was at least five years ago

Consider the five-year rule when determining whether to open a Roth or traditional IRA.

How to open a Roth IRA

Are you ready to unlock the tax-free magic of a Roth IRA? Let’s review a roadmap on how you can get started.

Step 1: Choose your financial institution.

The first and most crucial step in opening your Roth IRA involves choosing the right financial institution. This decision will shape your investment experience and ultimately impact your retirement savings potential. Consider these options:

- Online brokers: Powerhouses like Vanguard, Fidelity and Charles Schwab provide extensive investment choices and competitive fees, making them attractive for active investors.

- Traditional banks: Local banks offer a familiar touch for those seeking personalized service and comfort with brick-and-mortar interactions. While their investment options may be less diverse, they can provide valuable guidance and support, particularly for first-time investors.

- Robo-advisors: These automated platforms take the wheel, managing your portfolio for a fee. Ideal for hands-off investors or those seeking a set-and-forget approach, robo-advisors can simplify the investment process and ensure your portfolio aligns with your risk tolerance and goals.

The optimal choice depends on your individual preferences, investment experience and desired level of involvement. Research each option thoroughly, compare fee structures and consider your long-term financial objectives before selecting your financial home for your Roth IRA.

Step 2: Gather your documents.

Before starting your tax-free retirement journey, certain key documents will be required to unlock the doors to your Roth IRA. These pieces act as your passport, verifying your identity, ensuring accurate tax reporting and smoothing the path to your first contribution. Let's gather the essentials:

- Social Security number: Your financial fingerprint confirms your identity and ensures seamless integration with government databases for tax purposes.

- Proof of income: W-2s or tax returns act as your financial statement, demonstrating your contribution eligibility and establishing your tax bracket for future reference.

- Funding source details: Think of this as your financial bridge. Provide your bank account or routing number, allowing you to transfer funds and kick-start your Roth IRA contributions seamlessly.

Step 3: Open your account.

With your chosen financial institution in place, it's time to officially open your Roth IRA and activate your tax-free savings haven. Most institutions offer convenient online applications, making it a swift and straightforward process. Here's what to expect:

- Formalities first: Diligently fill out the application forms, providing accurate personal and financial information.

- Choosing your path: Select the Roth IRA type that suits your needs – individual or spousal.

- Navigating the investment landscape: This is where you personalize your savings journey. Choose your investment options, whether you prefer diversified mutual funds, individual stocks, or a blend tailored to your risk tolerance and retirement goals.

Bonus tip: Remember, your chosen investments will determine how your money grows tax-free within your Roth IRA. Bridge any knowledge gaps and empower informed investment decision-making by utilizing MarketBeat's investor glossary. Curated by financial specialists, this authoritative resource provides precise definitions through articles that simplify complex financial concepts.

Step 4: Make your initial deposit.

With your Roth IRA account opened and your investment path chosen, it's time to inject your financial engine with its first fuel injection. Your initial deposit signifies the start of your tax-free retirement journey. While minimum amounts for initial deposits vary by institution, they are typically as low as a symbolic $1 to $50.

Supercharge your retirement nest egg with the power of consistent contributions. Set your Roth IRA on autopilot with recurring deposits and witness the magic of tax-free compounding unfold. The earlier you start and the more consistently you feed it, the greater the potential for your retirement savings to blossom into a secure future. Curious about the potential impact? MarketBeat's Roth IRA calculator lets you personalize your goals and filters to see how your contributions can grow over time.

Bonus Step: Unleash the potential of existing accounts

A strategic maneuver exists for those with existing retirement accounts like a traditional IRA. You can take those IRAs and roll them over to your Roth IRA. This allows you to convert your pre-tax funds, currently subject to future taxation, into the tax-free haven of your Roth. While it's a decisive move, remember that it carries tax implications.

Ultimately, making your initial deposit and considering future contributions are critical steps in powering up your Roth IRA. By starting early, contributing consistently and strategically leveraging existing accounts, you can unlock the full potential of your tax-free retirement haven. Remember, even small, regular contributions can grow significantly with the magic of compound interest, paving the way for a secure and prosperous retirement.

Investment strategies for Roth IRA

With its tax-free growth, your Roth IRA offers a powerful tool for building a secure retirement. But the question remains, “How do you invest your contributions for optimal growth within this tax-advantaged haven?” Let’s take a few minutes and review some key strategies to guide your journey.

The foundation of your portfolio

Consider that your Roth IRA is like a diversified orchard. As you would not plant only apple trees, you should not put all your eggs in one investment basket. Your asset allocation should involve distributing your contributions across various asset classes, such as stocks, bonds and real estate, to manage risk and optimize returns. A well-balanced portfolio will help minimize the effects of market fluctuations and ensure that your retirement savings are protected during good and bad economic times.

Spreading the seeds of growth

Within each asset class, diversification is equally crucial. Don't limit yourself to just one stock or sector. Spread your investments across different companies, industries and even geographic regions. This reduces exposure to any single risk factor and increases the chances of consistent growth over time.

Let time be your ally

The magic of your Roth IRA will reveal itself over time. Unlike a traditional IRA, which is subject to taxes at retirement, your Roth IRA allows your money to grow tax-free and compound year after year. This means even small contributions, invested wisely and allowed to grow over decades, can blossom into a substantial retirement nest egg.

Finding your investment sweet spot

Your risk tolerance is a crucial factor in your investment selection. Younger investors with a longer time horizon can tolerate higher risk for potentially higher returns. Consider investing in growth-oriented assets like stocks or real estate investment trusts (REITs). Conversely, individuals nearing retirement may prioritize income and stability. Opting to add bonds and dividend stocks with your Roth IRA can provide a steadier income stream while preserving your capital.

With many investment options available, choosing the right ones can be overwhelming. Consider mutual funds, offering diversified exposure to various asset classes, or exchange-traded funds (ETFs) for lower fees and broader market coverage. For those seeking individual stock selection, thorough research and understanding your chosen companies are crucial. Don't just chase the latest trends; invest in companies you believe in and whose long-term prospects align with your retirement goals.

Bonus tip: Seek professional guidance

While navigating the investment landscape can be empowering, consulting a financial advisor can provide valuable insights and tailored strategies based on your unique circumstances. Their expertise can help you refine your asset allocation, select suitable investments and ensure your Roth IRA remains on track to achieve your retirement goals.

Pros and cons of IRAs

IRAs provide a range of benefits and drawbacks when deciding how to invest your limited capital. Calculate Roth IRA potential returns before choosing which type of account to open and familiarize yourself with both pros and cons.

Pros

IRAs offer a customizable way to save on taxes while investing more toward your future.

- Tax advantages: One of the biggest benefits of IRAs is their tax advantages. Traditional IRAs offer tax advantages the year you make contributions, while Roth IRAs offer tax-free growth.

- Flexibility: IRAs offer flexibility regarding investment options, allowing you to choose from a wide range of stocks, bonds, mutual funds and other assets.

- Additional benefits: You can hold an IRA in addition to a 401(k), making it an excellent choice for those who regularly max out their employer-sponsored IRAs.

Cons

While IRAs offer tax benefits, there may be better choices for anyone needing liquid funds access:

- Early penalty fees: If you deduct money from your IRA before age 59 1/2, you may face an early withdrawal fee of up to 10%.

- Income limitations: While traditional IRAs do not have income limits, Roth IRAs do.

Common mistakes to avoid

With its tax-free growth and withdrawal flexibility your Roth IRA is a retirement haven. But even in paradise, pitfalls lurk. Let's navigate the common mistakes to avoid and ensure your Roth IRA journey is smooth sailing all the way.

Overstepping the contribution limit

Exceeding the annual contribution limit is a costly slip-up. Remember, in 2024, it's $7,000 for individuals under 50 and $8,000 for those 50 and above. Going beyond these thresholds incurs penalties and potential tax implications. Track your contributions diligently to avoid this costly misstep avoiding the penalty for excess IRA contributions.

Miscalculating your asset allocation

Improper asset allocation can leave your portfolio vulnerable to excessive risk or insufficient growth. Young investors with a long time horizon can handle higher risk for potentially higher returns, while those nearing retirement may prioritize income and stability. Tailor your asset allocation to your risk tolerance and retirement goals.

Chasing the latest investment craze

Don't let shiny objects distract you from your long-term goals. Jumping on the latest investment bandwagon based on hype or FOMO can lead to impulsive decisions and potential losses. Stick to your investment strategy, focusing on companies and assets with solid fundamentals that align with your retirement objectives.

Forgetting about rebalancing

Your ideal asset allocation won't stay static as markets change. Periodic rebalancing ensures your portfolio remains aligned with your risk tolerance and goals. Rebalance annually or when significant deviations occur to maintain your desired risk profile.

Misunderstanding eligibility

Not everyone qualifies for a Roth IRA directly. Income limits exist and exceeding them disqualifies you from direct contributions. However, strategies like backdoor Roth IRAs can still offer tax-free benefits. Consult a financial advisor to determine your eligibility and explore alternative strategies if necessary.

Ignoring the power of time

Remember, the magic of your Roth IRA unfolds over time. Don't get discouraged by short-term market fluctuations. Stay invested and let your contributions compound tax-free. Patience is your ally in the Roth IRA game.

Neglecting regular contributions

Don't let your Roth IRA become a forgotten treasure chest. Even small, regular contributions can grow significantly over time thanks to compound interest. Set up automatic transfers to ensure consistent growth and reach your retirement goals faster.

Lacking a withdrawal strategy

While you can access contributions penalty-free from your Roth IRA at any time, early withdrawals of earnings may incur taxes and penalties. Develop a withdrawal strategy aligned with your overall retirement plan to avoid unnecessary tax burdens.

By avoiding these common pitfalls and staying informed, you can maximize the potential of your Roth IRA and build a secure, tax-free retirement haven. Remember, with careful planning and smart investment choices, your Roth IRA can blossom into a powerful tool for your financial future.

Planning for a tax-free retirement

The Roth IRA is a potent instrument for tax-optimized retirement planning. Its tax-deferred growth and flexible withdrawal provisions create a path toward financial security in your post-employment years. However, effective deployment of this tool requires a strategic, long-term approach to maximize its value and ensure your retirement portfolio’s future of tax-free withdrawals.

Orchestrate your income streams

Start by understanding your guaranteed income sources, such as pensions and Social Security. Analyze their tax implications and factor them into your Roth IRA withdrawal strategy. Aim to supplement these streams with tax-free withdrawals from your Roth IRA, effectively lowering your overall taxable income and stretching your retirement nest egg further.

Don't rely solely on your Roth IRA for income. Diversify your portfolio across taxable and tax-advantaged accounts like traditional IRAs and 401(k)s. This allows you to control your annual taxable income by strategically drawing from each source, optimizing your overall tax burden in retirement.

Consider incorporating side hustles or consulting gigs into your retirement income mix. Analyze the tax implications of these additional streams and adjust your Roth IRA withdrawals accordingly. Remember, the goal is to orchestrate a harmonious flow of income, minimizing taxes and maximizing your financial security.

Minimize taxable events

While your Roth IRA offers a tax-free haven, minimizing the overall tax burden in retirement requires a strategic counterpoint. The earlier you start contributing to your Roth IRA, the longer your money enjoys the magic of tax-free compounding. Consistent contributions throughout your career, even modest amounts, can significantly boost your retirement nest egg thanks to the exponential growth potential.

Do you have pre-tax retirement accounts like traditional IRAs or 401(k)s? Consider converting them to Roth IRAs. While this incurs upfront taxes, it effectively prepays the taxman, allowing you to enjoy tax-free withdrawals later in retirement. This strategy can be particularly beneficial if you anticipate higher tax brackets in the future.

Don't forget your tax-advantaged accounts like Health Savings Accounts (HSAs) and 529 plans. These instruments allow you to earmark funds for specific expenses like healthcare or education, reducing your taxable income while your money grows tax-free.

Leverage Roth IRA flexibility across life stages

Your Roth IRA's flexibility will shine throughout your financial journey. You can adapt it to your evolving needs in each life stage. Here's how to leverage its potential at every step:

- Early career: Prioritize consistent contributions, even small amounts. Remember, compounding magic works best over time. The tax-free growth within your Roth IRA becomes a powerful ally, supplementing your future income and building a secure retirement haven.

- Pre-retirement: Consider strategic Roth conversions. Moving pre-tax funds to your Roth IRA incurs upfront taxes, but it unlocks tax-free access later. This flexibility allows you to manage your taxable income in retirement and enjoy more financial freedom without future tax burdens.

- Retirement: Treat your Roth IRA as a tax-free income stream. Utilize it to supplement your guaranteed income sources like pensions and Social Security. By strategically drawing from various sources, you can further optimize your overall tax burden and stretch your retirement nest egg.

Planning for a tax-free retirement is a dynamic process. Regularly review your income sources, tax implications and withdrawal strategies. Adapt your approach as your circumstances and financial goals evolve.

Is a Roth IRA right for you?

Roth IRAs are an exceptionally useful tool that allows you to save more towards retirement and customize your benefits. However, it's important to remember that Roth IRAs have rules and restrictions, such as contribution limits and withdrawal rules. Consider both the pros and cons of both major types of accounts thoroughly and consult with a tax professional to learn more about the most beneficial option for you.

FAQs

Before leaving to browse a media sentiment stocks list or a list of major cap companies, get these last-minute answers to common Roth IRA questions.

What is better, a 401(k) or Roth IRA?

A 401(k) can be beneficial if your employer offers matching contributions and you want to lower your taxable income. A Roth IRA may be better if you want tax-free withdrawals in retirement or if you think your income will be higher when you retire. However, you can have both types of accounts as a single investor. Learn more about other niche IRAs, like gold IRAs, before you invest.

How does a Roth IRA work?

A Roth IRA is a type of individual retirement account that allows you to save money for retirement on a post-tax basis. This means that you contribute money to your Roth IRA with after-tax dollars, and your contributions and earnings grow tax-free. Once you reach age 59 and a half, you can make withdrawals from the account without paying taxes.

What is a disadvantage of a Roth IRA?

One disadvantage of a Roth IRA is its early withdrawal fees. If you withdraw money from your Roth IRA before age 59 and a half, you may face penalties of up to 10%.

Before you consider Vanguard S&P 500 ETF, you'll want to hear this.

MarketBeat keeps track of Wall Street's top-rated and best performing research analysts and the stocks they recommend to their clients on a daily basis. MarketBeat has identified the five stocks that top analysts are quietly whispering to their clients to buy now before the broader market catches on... and Vanguard S&P 500 ETF wasn't on the list.

While Vanguard S&P 500 ETF currently has a Hold rating among analysts, top-rated analysts believe these five stocks are better buys.