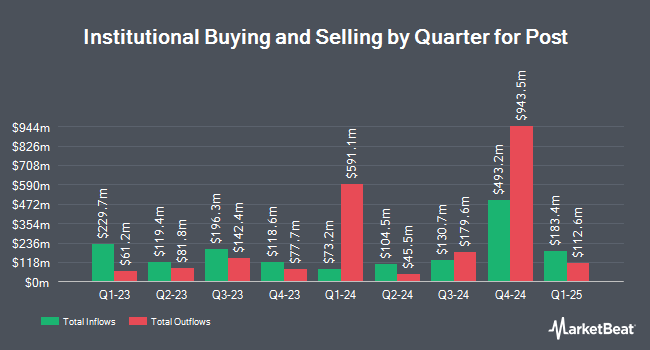

Artemis Investment Management LLP decreased its position in shares of Post Holdings, Inc. (NYSE:POST - Free Report) by 37.8% in the fourth quarter, according to its most recent Form 13F filing with the Securities & Exchange Commission. The firm owned 178,893 shares of the company's stock after selling 108,680 shares during the quarter. Artemis Investment Management LLP owned 0.35% of Post worth $17,719,000 as of its most recent SEC filing.

Other institutional investors and hedge funds have also recently modified their holdings of the company. Royal Bank of Canada boosted its position in Post by 74.2% in the 1st quarter. Royal Bank of Canada now owns 57,535 shares of the company's stock worth $6,694,000 after purchasing an additional 24,514 shares in the last quarter. Empowered Funds LLC raised its stake in shares of Post by 12.3% during the 1st quarter. Empowered Funds LLC now owns 4,436 shares of the company's stock worth $516,000 after buying an additional 487 shares during the period. Focus Partners Wealth raised its stake in shares of Post by 11.1% during the 1st quarter. Focus Partners Wealth now owns 3,287 shares of the company's stock worth $382,000 after buying an additional 328 shares during the period. Intech Investment Management LLC raised its stake in shares of Post by 181.1% during the 1st quarter. Intech Investment Management LLC now owns 11,771 shares of the company's stock worth $1,370,000 after buying an additional 7,583 shares during the period. Finally, Russell Investments Group Ltd. raised its stake in shares of Post by 3.9% during the 2nd quarter. Russell Investments Group Ltd. now owns 13,289 shares of the company's stock worth $1,449,000 after buying an additional 494 shares during the period. Institutional investors and hedge funds own 94.85% of the company's stock.

Key Stories Impacting Post

Here are the key news stories impacting Post this week:

- Positive Sentiment: Post’s most recent reported quarter showed an EPS beat and revenue growth (EPS topped estimates and revenue rose ~10% year‑over‑year), giving investors confidence in underlying demand and margin recovery. (Company Q1 results referenced in summary)

- Positive Sentiment: Wall Street is expecting earnings growth in Post’s next report, which creates upside if management repeats or raises guidance. Post Holdings: Zacks preview

- Neutral Sentiment: U.S. equity benchmarks are at or near record highs on strong earnings, a backdrop that can support cyclical consumer names but is tech‑led and not uniformly beneficial to all food/packaged‑goods stocks. S&P/Nasdaq record highs

- Negative Sentiment: Geopolitical headlines and ongoing conflict-related news have lifted volatility and generated periodic pressure on commodity/energy prices and transportation costs — factors that inflate COGS and distribution expenses for food manufacturers like Post. (Macro risk summarized from recent market coverage)

- Negative Sentiment: Balance-sheet leverage is a structural risk: Post’s reported debt-to-equity is elevated, which can magnify investor concern if margins slip or raw‑material/transport costs rise; higher leverage increases sensitivity to any guidance misses. (Company balance-sheet metrics referenced in summary)

Insiders Place Their Bets

In related news, Director Gregory L. Curl sold 6,983 shares of Post stock in a transaction on Monday, February 9th. The shares were sold at an average price of $114.31, for a total value of $798,226.73. Following the transaction, the director directly owned 21,293 shares in the company, valued at $2,434,002.83. This trade represents a 24.70% decrease in their position. The transaction was disclosed in a filing with the SEC, which is available at the SEC website. 14.05% of the stock is currently owned by company insiders.

Analyst Upgrades and Downgrades

Several research analysts recently commented on POST shares. Zacks Research raised Post from a "strong sell" rating to a "hold" rating in a research note on Monday, February 9th. JPMorgan Chase & Co. cut their target price on Post from $133.00 to $119.00 and set an "overweight" rating for the company in a research note on Monday, April 20th. Wall Street Zen raised Post from a "hold" rating to a "buy" rating in a research note on Saturday, February 7th. Wells Fargo & Company lowered their price target on Post from $120.00 to $110.00 and set an "equal weight" rating for the company in a report on Wednesday, April 8th. Finally, BTIG Research started coverage on Post in a report on Monday, April 13th. They set a "neutral" rating for the company. Five analysts have rated the stock with a Buy rating and four have issued a Hold rating to the stock. According to data from MarketBeat, the company currently has a consensus rating of "Moderate Buy" and a consensus price target of $124.50.

Get Our Latest Stock Report on Post

Post Trading Down 1.5%

POST opened at $103.23 on Friday. The firm has a market cap of $4.94 billion, a price-to-earnings ratio of 19.08 and a beta of 0.44. Post Holdings, Inc. has a 52 week low of $94.13 and a 52 week high of $117.28. The business's 50 day moving average is $101.55 and its two-hundred day moving average is $102.36. The company has a quick ratio of 1.02, a current ratio of 1.90 and a debt-to-equity ratio of 2.15.

Post (NYSE:POST - Get Free Report) last released its earnings results on Thursday, February 5th. The company reported $2.13 earnings per share (EPS) for the quarter, beating analysts' consensus estimates of $1.66 by $0.47. Post had a return on equity of 12.37% and a net margin of 3.82%.The business had revenue of $2.17 billion for the quarter, compared to analyst estimates of $2.18 billion. During the same quarter in the previous year, the company posted $1.73 earnings per share. The company's revenue for the quarter was up 10.2% compared to the same quarter last year. On average, research analysts predict that Post Holdings, Inc. will post 7.24 EPS for the current year.

Post Company Profile

(

Free Report)

Post Holdings, Inc is a consumer packaged goods company that operates as a holding company for a diverse portfolio of food and beverage brands. The company's principal activities include the production, marketing and distribution of ready-to-eat cereal, refrigerated and frozen foods, and nutritional beverages. Through its operating segments—Post Consumer Brands, Foodservice, Refrigerated Side Dishes & Bakery, and Active Nutrition—Post Holdings delivers a broad array of products to retail grocers, convenience stores, foodservice operators and e-commerce channels.

The Post Consumer Brands segment features a variety of hot and cold cereals under names such as Honey Bunches of Oats, Shredded Wheat and Pebbles.

Featured Articles

Want to see what other hedge funds are holding POST? Visit HoldingsChannel.com to get the latest 13F filings and insider trades for Post Holdings, Inc. (NYSE:POST - Free Report).

This instant news alert was generated by narrative science technology and financial data from MarketBeat in order to provide readers with the fastest reporting and unbiased coverage. Please send any questions or comments about this story to contact@marketbeat.com.

Before you consider Post, you'll want to hear this.

MarketBeat keeps track of Wall Street's top-rated and best performing research analysts and the stocks they recommend to their clients on a daily basis. MarketBeat has identified the five stocks that top analysts are quietly whispering to their clients to buy now before the broader market catches on... and Post wasn't on the list.

While Post currently has a Moderate Buy rating among analysts, top-rated analysts believe these five stocks are better buys.

View The Five Stocks Here

We are about to experience the greatest A.I. boom in stock market history...

Thanks to a pivotal economic catalyst, specific tech stocks will skyrocket just like they did during the "dot com" boom in the 1990s.

That’s why, we’ve hand-selected 7 tiny tech disruptor stocks positioned to surge.

- The first pick is a tiny under-the-radar A.I. stock that's trading for just $3.00. This company already has 98 registered patents for cutting-edge voice and sound recognition technology... And has lined up major partnerships with some of the biggest names in the auto, tech, and music industry... plus many more.

- The second pick presents an affordable avenue to bolster EVs and AI development…. Analysts are calling this stock a “buy” right now and predict a high price target of $19.20, substantially more than its current $6 trading price.

- Our final and favorite pick is generating a brand-new kind of AI. It's believed this tech will be bigger than the current well-known leader in this industry… Analysts predict this innovative tech is gearing up to create a tidal wave of new wealth, fueling a $15.7 TRILLION market boom.

Right now, we’re staring down the barrel of a true once-in-a-lifetime moment. As an investment opportunity, this kind of breakthrough doesn't come along every day.

And the window to get in on the ground-floor — maximizing profit potential from this expected market surge — is closing quickly...

Simply click the link below to get the names and tickers of the 7 small stocks with potential to make investors very, very happy.

Get This Free Report

Like this article? Share it with a colleague.

Link copied to clipboard.