Foot Locker NYSE: FL

Foot Locker NYSE: FL is set to report its Q3 earnings on Friday, and some people are wondering:

Can the footwear retailer match its Q2 growth rates?

In Q2, revenue was up 17.5% yoy to $2.08 billion.

I’ll save you the suspense: Foot Locker almost certainly will fall short of 17.5% revenue growth in Q3 (and Q4, for that matter). But the market has priced in lower expectations – roughly flat revenue growth in Q3 and Q4.

Let’s start by analyzing why Q2 was so strong, before determining whether Foot Locker can clear lower bars in Q3 and Q4.

Q2 Had Three Short-Term Tailwinds

On the Q2 earnings call, Foot Locker noted that “pent-up demand” and “fiscal stimulus” were largely responsible for the high growth rates. Furthermore, The Last Dance documentary was released in late Q1 / early Q2, which connected the Jordan Brand to a “new generation of consumers and really drove maximum impact.”

It’s nice that Foot Locker benefited from the three tailwinds, but they aren’t sustainable. Let’s look at them one-by-one:

- Pent-up demand was due to store closures and lockdowns. That may not happen again. And if it does, there will be a corresponding and roughly equivalent slowdown in another quarter.

- There may be more fiscal stimulus on the way – more on that later – but $1,200 checks aren’t about to start coming consistently.

- The Jordan documentary could lead to a sustained level of interest in the greatest basketball player of all time (there, I said it), but I don’t see the documentary elevating the brand by enough to really make a difference for Foot Locker.

These tailwinds weren’t too hard to predict early in Q2, but Foot Locker still deserves props for its inventory management. Inventory was down just 2.7% compared to the double-digit sales growth. Countless retailers have struggled with inventory management since the onset of the pandemic.

Foot Locker’s inventory levels positioned the retailer well for Q3, and will be even more important as we move into the holiday season.

Q3 and Q4 Performance Hinge on Long-Term Drivers

You didn’t want to buy companies that relied on mall traffic before the pandemic. So, even if the vaccine does come through, you still won’t want to own companies that rely on mall traffic post-pandemic.

Foot Locker still derives a lot of its business from malls, but it is taking steps to reduce that reliance. On the Q2 call, CEO Richard Johnson said, “In short, we believe we are well-positioned to capitalize on evolving customer shopping behaviors through a sustained emphasis on digital as well as evaluating a further pivot off-mall, including through our Power Store offense. We believe our Power Store concept and community focus is the right offense to offset mall-related pressures.”

The digital business has been particularly impressive, growing at a triple-digit rate even as Foot Locker reopened stores.

Then, there’s basketball. Yes, the Jordan documentary was a short-term tailwind. But that doesn’t change the fact that basketball is a massively popular sport. Men’s basketball recorded a double-digit increase in Q2, and with the NBA set to start back up next month, that interest won’t have much of a chance to die down.

Finally, there’s the potential for another round of stimulus. Again, this won’t be a long-term tailwind, but it could provide a boost for either Q4 or Q1. I continue to believe that it will come – eventually.

The Verdict

I think that mid-single-digit revenue growth is realistic in Q3 and Q4, and that would exceed expectations.

Also, a number of firms have raised their price targets over the past week, but the numbers are still conservative:

- UBS NYSE: UBS from $30 to $36.

- Morgan Stanley NYSE: MS from $31 to $36.

- Raymond James NYSE: RJF from $35 to $50.

- Wedbush from $37 to $44.

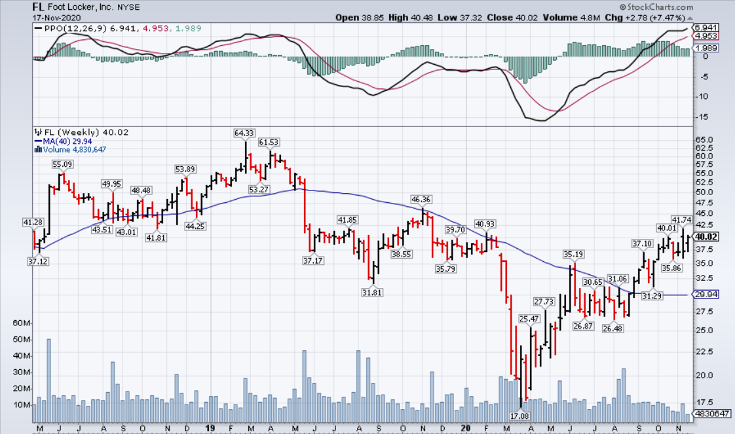

Foot Locker is currently trading at just over $40 a share, so a beat on Friday could easily lead to a barrage of higher price targets. Though FL remains well below its all-time highs, a strong report could take it to 52-week highs, clearing the way for another leg-up.

I’d look to get in ahead of a potential move to ensure that you don’t get left behind.

Before you consider Foot Locker, you'll want to hear this.

MarketBeat keeps track of Wall Street's top-rated and best performing research analysts and the stocks they recommend to their clients on a daily basis. MarketBeat has identified the five stocks that top analysts are quietly whispering to their clients to buy now before the broader market catches on... and Foot Locker wasn't on the list.

While Foot Locker currently has a Hold rating among analysts, top-rated analysts believe these five stocks are better buys.

View The Five Stocks Here

The AI wave will soon hit public markets with Anthropic and OpenAI set to go public later this year. However, you don't have to wait to invest. This report shows seven AI stocks that you can buy today while the big model providers get ready to go public.

Get This Free Report

Like this article? Share it with a colleague.

Link copied to clipboard.