Costco Wholesale Today

COST

Costco Wholesale

$956.32 -38.88 (-3.91%) As of 05/29/2026 04:00 PM Eastern

- 52-Week Range

- $844.06

▼

$1,096.50 - Dividend Yield

- 0.61%

- P/E Ratio

- 49.73

- Price Target

- $1,056.32

Costco Wholesale Corp. NASDAQ: COST reported its fiscal Q3 2026 results after the market closed on May 28, and at first glance, it appears the company produced another stellar quarter.

But the market reaction following the report was muted. The stock was down 4% shortly after the opening bell the next day, which seems underwhelming for a company that posted record revenue and has a potential tariff refund catalyst on the horizon.

As always, a deeper dive into the numbers reveals the reason for the reaction. While Costco’s long-term growth story remains intact, it's becoming more difficult to justify paying 50x earnings for the stock.

Inflation-Weary Consumers Turn to Costco Value Proposition

First, the good news.

Costco announced record revenue in fiscal Q3 2026, reporting $69.15 billion in sales and total revenue of $70.53 billion when including membership fees, which beat the $69.68 billion consensus. Earnings per share (EPS) of $4.93 was slightly under the anticipated $4.98 from analysts. Overall membership growth was up 4.1%, and the executive tier premium plan now boasts 41.2 million members.

Membership fees are the true engine of Costco’s margin growth, so these figures need to keep rising to offset merchandise and fuel costs.

Same-store sales, a key metric that strips out growth from new store openings, increased 9.8% year-over-year (YOY), the company’s highest figure in over two years. The Iran war, which has pushed gasoline prices to multi-year highs, drove much of the increase in memberships and same-store sales.

Costco Wholesale Dividend Payments

- Dividend Yield

- 0.61%

- Annual Dividend

- $5.88

- Dividend Increase Track Record

- 22 Years

- Annualized 5-Year Dividend Growth

- 12.75%

- Dividend Payout Ratio

- 30.58%

- Recent Dividend Payment

- May. 15

COST Dividend HistoryWholesale club retailers like Costco and BJ’s Wholesale Club Holdings Inc. NYSE: BJ are often beneficiaries of gas price spikes since they mark their prices between 10 and 30 cents lower than independent gas stations.

Gas prices are a very visible pressure point for consumers, and price spikes often entice consumers to "bite the bullet" and sign up for a wholesale club membership.

The numbers support this thesis: gas volumes from the last five weeks of the quarter were among the five highest totals the company has reported in such a span.

Costco expects to open 26 new warehouses during the fiscal 2026 calendar, and is targeting more than 30 openings in the coming years.

Income investors were also thrown a bone as the company increased its dividend 13% to $1.47 per share, and there’s reason to believe a special dividend could be in the works this year.

Overall, another strong earnings report, but not exactly the blowout investors were hoping to see.

Pricey Valuation Hovers Over Mixed Earnings Picture

The biggest red flag at Costco has always been the valuation. Investors are paying a tech-sector multiple for a retailer with margins more like those of a grocery store than a semiconductor foundry.

A few things from the report explain the less-than-enthusiastic reaction:

Gas Spike Oversells Same-Store Sales: The 9.8% figure looks impressive on its face, but it drops to a more modest 6.6% when adjusted for gas and currency effects. The adjusted figure is more of a "real" number, since it removes variables like fuel inflation and accounts only for extra units sold. The 6.6% is a middle-of-the-pack result compared to the last two years, so the headline number didn’t factor into the stock reaction.

Low-Quality Earnings Beat For an Expensive Stock: When factoring in the gap between headline and adjusted same-store sales and the slight EPS miss, there wasn’t much upside to celebrate in this report. The stock is already hovering around all-time highs and trades around 47x forward earnings, so an earnings smash is needed to create a big upward move. Fiscal Q3 2026 would qualify as "good but not great," which isn’t going to move a stock with a lofty valuation.

Tariff Refund Uncertainty: One potential catalyst for Costco is the reversal of the Trump administration’s IEEPA tariffs, but the refund process has been murky. Additional temporary tariffs have been levied in the meantime, and management remains burdened by uncertainty in this area. Costco said it has started submitting claims through U.S. Customs and Border Protection and expects approved refunds on a rolling basis, but management also noted that the return process depends on refund timing and litigation developments.

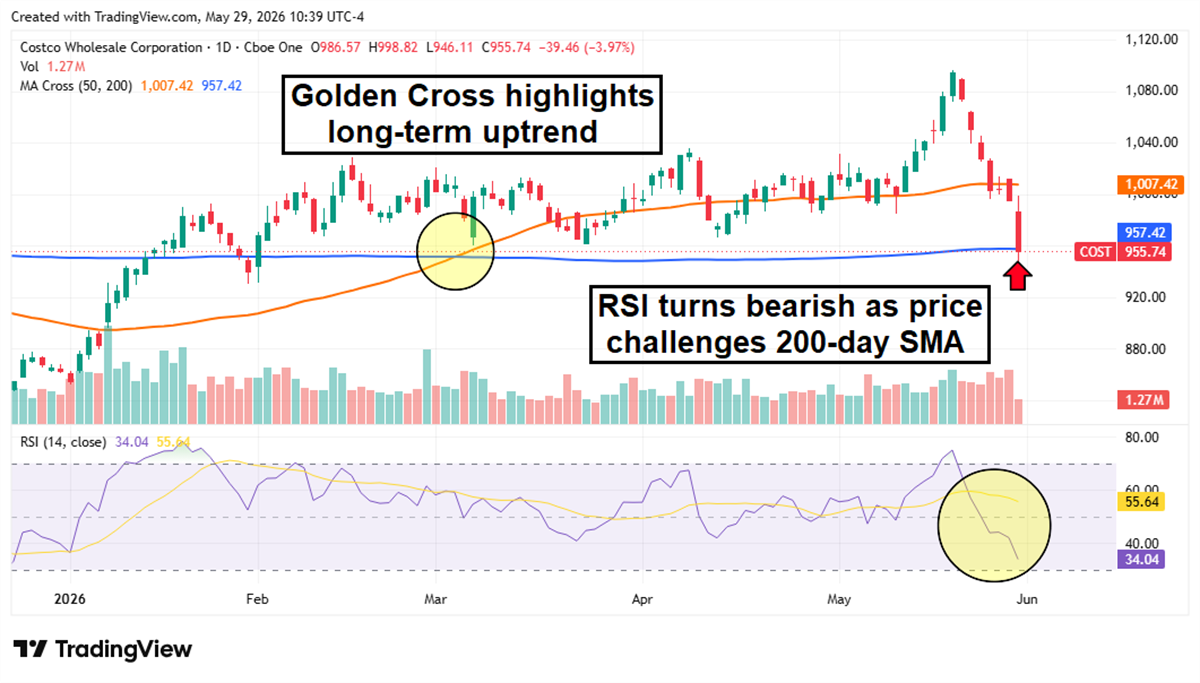

Chart Shows Fading Momentum and Potential Consolidation Period

Costco shares are still up more than 10% year-to-date (YTD), but have spent much of the last few months in a consolidation pattern that doesn’t appear ready to break. Most of the stock’s 2026 gains were accumulated within the first few weeks of the year, long before the Iran war was on any investor or analyst’s radar. But the share price has been stuck since the end of January, bouncing in a tight range between $950 and $1050.

The stock’s latest new all-time high of $1094 on May 19 was immediately followed by six red sessions in a row, and now the Relative Strength Index (RSI) has dipped into bearish territory under 50. Long-term momentum remains in place thanks to January’s Golden Cross, which has kept the 50-day moving average above the 200-day moving average. Still, investors can likely expect more volatile, range-bound trading in the short term.

Before you consider Costco Wholesale, you'll want to hear this.

MarketBeat keeps track of Wall Street's top-rated and best performing research analysts and the stocks they recommend to their clients on a daily basis. MarketBeat has identified the five stocks that top analysts are quietly whispering to their clients to buy now before the broader market catches on... and Costco Wholesale wasn't on the list.

While Costco Wholesale currently has a Moderate Buy rating among analysts, top-rated analysts believe these five stocks are better buys.

View The Five Stocks Here

Just getting into the stock market? These 10 simple stocks can help beginning investors build long-term wealth without knowing options, technicals, or other advanced strategies.

Get This Free Report

Like this article? Share it with a colleague.

Link copied to clipboard.