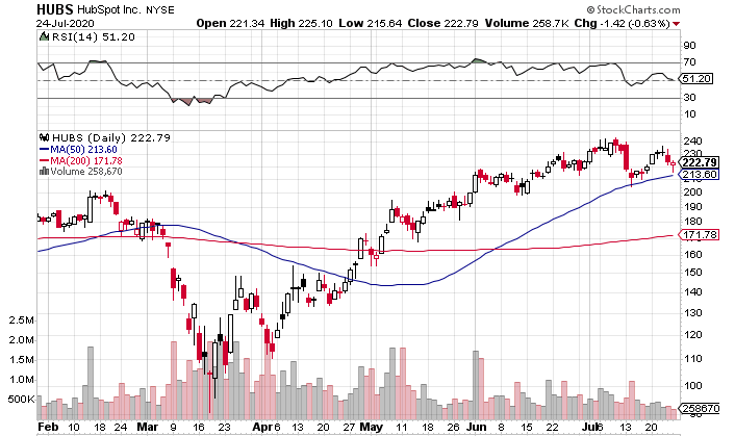

HubSpot NYSE: HUBS, which offers a cloud-based marketing, sales, and CRM platform, nearly tripled off its lows of mid-March to set all-time highs above $240 a share in early July. Since then, shares have pulled back and currently sit just above the 50-day moving average.

HubSpot has been hyper-focused on revenue growth, growing revenue at a 40% CAGR over the past five years. But that growth has come at the cost of short-term cash flow; HubSpot has had just $42 million in free cash flow over the past 12 months. Q1 2020 free cash flow came in at just $7 million.

The company is also trading at around 12x projected 2020 revenue, raising the question:

Does HubSpot have a path to grow into its valuation?

Continued Growth During the Pandemic

Q1 2020 was kind to HubSpot, as revenue grew by more than 30% yoy on the back of total customer growth of around the same percentage. Domestic revenue grew 25% in Q1, while international revenue was up 45% yoy (in constant currency).

The company expects 20% yoy revenue growth in Q2, and revenue growth of 19% yoy for the full-year 2020. Consensus estimates also call for revenue growth in the 20% range for full-year 2021.

While it appears that revenue growth will slow from the 40% level of the previous five years, ~20% is nothing to sneeze at.

Furthermore, a recent report by ResearchAndMarkets.com estimates the global market for Digital Marketing Software at $48.3 billion in 2020. It projects that number to grow to $123.1 billion by 2027, a CAGR of 14.3%. As a leader in the digital marketing software industry, it’s very possible that HubSpot will see a revenue CAGR of 15-20% over the next seven years.

Looking at HubSpot’s operations, we can see the factors responsible for the company’s success.

An All-In-One Platform With Long-Term Tailwinds

HubSpot’s platform provides companies with a vast array of benefits including search engine optimization, content management, marketing automation, sales productivity and much more.

In Q1, subscription revenue was $10,018 per customer, up slightly yoy. Net revenue retention rate actually fell to the low 90%s in March, but most of that decline came from downgrades as opposed to cancellations. HubSpot offered cash-strapped clients discounts and downgrades to keep them in the HubSpot ecosystem, a savvy long-term move that will bring an increased pay off when the economy recovers.

The company reduced the price of its starter growth suite by over 50% late in Q1, resulting in a five-fold increase in the package’s run rate at the end of Q1.

HubSpot is taking the long view here. Eventually, the company should be able to return these customers to full-priced plans. Many of them will stay with the company for several years and the short-term dip in revenue would be well worth it.

Looking at the big picture, the pandemic is causing a lot of companies to shift their operations online. HubSpot’s tools are designed to help companies make that shift. And this is an acceleration of an existing trend; companies have been shifting their operations online for several years leading up to the pandemic. The pandemic just provided yet another push. This means that it’s unlikely the trend will reverse, and a lot of these moves will stick.

Is The Chart Too Extended?

As stated earlier, HubSpot has had quite a move over the past 4+ months. While shares have taken a breather during the month of July, the stock hasn’t put in a proper base recently.

You could look to get in now as shares seem to be getting support at the 50-day moving average. A couple of weeks ago, shares touched the 50-day and quickly bounced off of it, closing near the highs of the day. And in Friday’s session, shares got close to the 50-day before moving higher and again closing near the day’s highs. The good thing about buying here would be the logical place for a stop-order just below the 50-day, which would give you a defined downside of less than 5%.

Alternatively, you could wait for the stock to put in a solid base, preferably of at least two months. This way, shares could fully digest the large gains off the lows and have a good foundation for another leg-up.

The Verdict

It’s always risky to buy stocks with valuations that price in a lot of growth. In the case of HubSpot, there is good reason to believe it will experience 15-20% growth over the next seven years – perhaps longer.

But there’s a lot of guesswork in projecting earnings for 5-10 years down the road, and nobody can say if those earnings will be high enough to justify its current $9 billion + valuation.

Bottom line, there is a good argument to buy HubSpot, but if you do, be sure to place a stop-order within 5-10% of your purchase price. This way, you can expose yourself to the long-term upside without giving yourself a big downside in the case that earnings don’t materialize.

Before you make your next trade, you'll want to hear this.

MarketBeat keeps track of Wall Street's top-rated and best performing research analysts and the stocks they recommend to their clients on a daily basis.

Our team has identified the five stocks that top analysts are quietly whispering to their clients to buy now before the broader market catches on... and none of the big name stocks were on the list.

They believe these five stocks are the five best companies for investors to buy now...

See The Five Stocks Here

With the proliferation of data centers and electric vehicles, the electric grid will only get more strained. Download this report to learn how energy stocks can play a role in your portfolio as the global demand for energy continues to grow.

Get This Free Report