Corning NYSE: GLW

Corning NYSE: GLW recently raised its Q3 guidance, making it clear that its innovation will spearhead outperformance – even in a tough market.

Here’s what CFO Tony Tripeny said in the release:

“I’m pleased to share that the positive momentum seen in July has continued, and we expect third-quarter sequential sales growth in the low teens, higher than the current consensus estimate of high-single digits. We’re delivering for our customers, outperforming our markets, and preserving our financial strength. Looking ahead, our underlying growth drivers are intact."

Corning’s Q2 beat expectations, but sales were down 13% yoy and net income dipped 47% yoy.

It’s not what you want to see, but once industry conditions inevitably improve, Corning will return to growth.

Here are three reasons why:

1. Gorilla Glass is Teflon

It’s been a tough year for the global smartphone market. Sales have improved after being down 50% yoy in April, but were still down 24% yoy in Q2, according to Counterpoint. That was the fastest ever rate of decline for the market.

Corning’s Gorilla Glass has been used on more than 8 billion devices worldwide, so you would expect a similar decline for its Q2 sales in the Specialty Materials segment. But that wasn’t the case, as the segment saw 13% yoy revenue growth.

Despite the impressive relative success, Corning isn’t resting on its laurels:

The company just launched Gorilla Glass Victus; according to Corning, it “features significantly better drop and scratch performance than any other Gorilla Glass or competitive glass from other manufacturers.” Samsung has already agreed to start using the new glass in its products.

The smartphone market is going to grow post-pandemic. Corning’s current outperformance and innovation indicate that it will see nice growth when that happens.

2. Gasoline Particulate Filters Drove Auto Outperformance

Global auto production saw a huge decline in Q2, dipping 45% yoy. Corning’s auto sales, on the other hand, saw a decline of 31% yoy. Not great, but again, it’s outperformance.

Corning’s gasoline particulate filters led the way, with sales growing 20% yoy. With emissions control being such a hot initiative by governments across the world, this segment can easily see double-digit growth for many years to come.

But what about new car sales? They have been low and may continue to track below pre-pandemic levels for a while. Corning doesn’t benefit from the surging used car market, after all.

It might be unrealistic to expect growth in new car sales anytime soon. But even if that 45% decline turns into a 10-20% dip, Corning would enjoy a lot of upside from where we are now. Especially considering its recent outperformance.

3. Corning is Getting into the Vaccine Game

You probably don’t think of a glass company when you think of COVID-19 vaccine efforts, but Corning’s Valor Glass innovation may play a crucial role in the administration of the eventual vaccine.

The glass helps “enable faster filling line speeds and increase patient safety.” Valor Glass vials are up to 10 times stronger than traditional vials.

The U.S. government is a believer in Valor Glass and has put its money where its mouth is, awarding Corning with $204 million to expand its Valor manufacturing capability. The government has shown little restraint in spending money to combat the virus, and now Corning becomes yet another private sector beneficiary.

And the Valor glass use cases go beyond COVID-19 vaccines, with Corning reaching an agreement with Pfizer NYSE: PFE to provide Valor Glass for other drugs.

The Verdict

I liked the valuation on Corning two months ago. With shares trading only slightly higher now, and the company’s outlook improving over the past couple of months, I like it even more now.

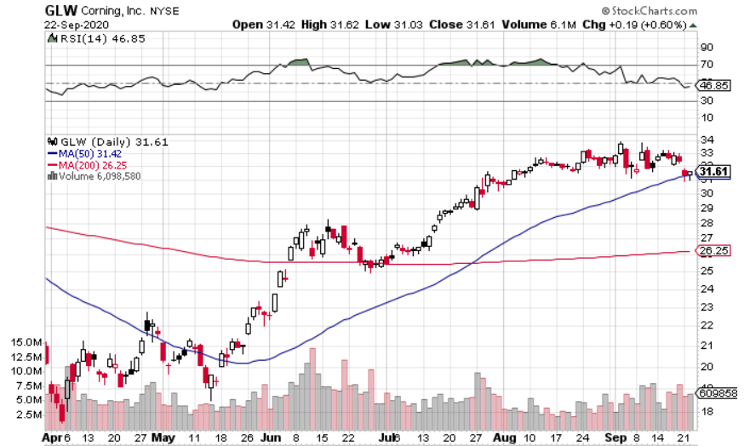

Shares are in a solid up-trend right now, so you may be able to achieve sold returns on a Corning investment in 2020.

But as I said back in July, the real upside with Corning is in 2021 and beyond. Consider a buy-and-hold play on Corning; it could pay off nicely over the next few years as industry conditions improve and Corning’s innovations are able to reach their full potential.

Before you consider Corning, you'll want to hear this.

MarketBeat keeps track of Wall Street's top-rated and best performing research analysts and the stocks they recommend to their clients on a daily basis. MarketBeat has identified the five stocks that top analysts are quietly whispering to their clients to buy now before the broader market catches on... and Corning wasn't on the list.

While Corning currently has a Moderate Buy rating among analysts, top-rated analysts believe these five stocks are better buys.

View The Five Stocks Here

Nuclear energy is entering a new growth cycle as rising power demand, expanding data centers, and renewed policy support bring the sector back into focus. After strong gains in recent years, the most impactful phase of nuclear investment may still be ahead.

This report highlights seven nuclear energy stocks positioned across the value chain—combining near-term revenue with long-term upside as next-generation technologies scale. Click the link below to unlock the full list.

Get This Free Report

Like this article? Share it with a colleague.

Link copied to clipboard.