Shares of chip design software maker Synopsys Inc. NASDAQ: SNPS have been forming a potentially constructive consolidation since its first-quarter earnings report on February 15.

As a business-to-business vendor, Synopsys isn’t exactly a household name, but it has several attributes that suggest it could stage further price gains in the next two years.

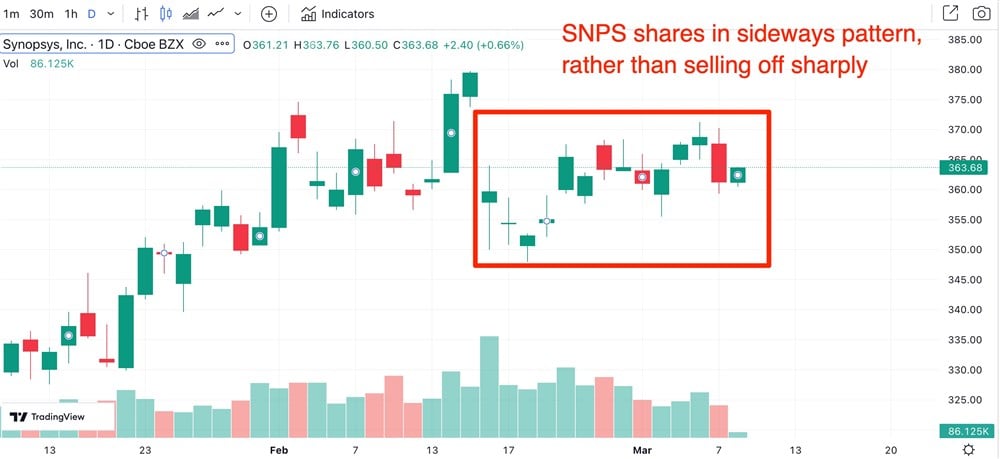

Although the stock came under selling pressure after disappointing guidance, shares are holding well above their 50-day moving average, a sign that big investors didn’t see anything devastating in the report. A glance at its chart, using a weekly view with candlesticks or bars, clearly shows a trading sideways stock, essentially treading water while investors are holding rather than selling.

Also giving shares a boost: On February 23, Synopsys initiated an accelerated $300 million share buyback program, to be completed before May 12. The stock closed higher the week ended February 24, immediately following the announcement, and the week ended March 3.

The mild selling essentially amounted to a bit of profit-taking after a one-year gain of 22.28%. With a market capitalization of $55 billion, Mountain View, California- based Synopsys is a component of the S&P 500. Its one-year performance easily outpaces the broader index, which is down 3.50% on a one-year basis.

Outperforming Tech Sector

Perhaps more importantly, Synopsys’ performance also tops the S&P tech sector, as tracked by the Technology Select Sector SPDR Fund NYSEARCA: XLK. The underlying tech-sector benchmark is down 2.67% in the past year.

Synopsis provides software, hardware, and services to help semiconductor companies make fast and efficient pivots to the cloud. Naturally, machine learning and artificial intelligence are growing in the company’s products and services.

In its fiscal first quarter, the company earned $2.62 a share on revenue of $1.361 billion, up 9% and 7%, respectively. According to data gathered by MarketBeat, the company beat earnings views and met on the revenue side.

Nowadays, it’s often not enough to meet Wall Street’s views, as investors have come to expect more. It doesn’t help that there’s likely some sandbagging by companies who issue deliberately lower guidance to beat that.

Often, unexpectedly good estimates can send a stock higher, even if the most recent quarter disappointed in some way. Synopsys, however, issued somewhat weak guidance for the current quarter and the full year.

For the fiscal second quarter, which ends on April 30, Synopsys is forecasting earnings of $2.48 per share on revenue of $1.375 billion, the midpoint of guidance. Wall Street had been looking for earnings of $2.56 per share on revenue of $1.43 billion.

For the full year, which wraps up on October 31, the company pegged earnings at $10.57 a share on revenue of $5.8 billion, above net income of $10.38 a share but slightly below sales of $5.81 billion.

Revised Estimates Higher

Wall Street recently revised its consensus earnings estimate higher by a penny for this year, for a 19% year-over-year earnings increase. Analysts expect an increase of 15% in 2024 to $12.14 a share.

MarketBeat analyst data show a consensus rating of “moderate buy,” and a price target of $424.18, an upside of 16.68%. That’s consistent with solid double-digit earnings estimates.

After the first-quarter report, Morningstar analyst Abhinav Davuluri wrote, “Despite a choppy macroenvironment involving reduced semiconductor industry growth and a looming recession, management reaffirmed its full-year guidance as increasing its adjusted EPS target range. Synopsys remains confident in long-term demand from end-markets, as the company continues to benefit from secular tailwinds toward hyperscale computing, artificial intelligence, or AI, and 5G communications.”

He added that he expects Synopsys to continue gaining “broad-based significance as demand for higher complexity and tighter integration and security in chips perpetuates throughout industries.”

Synopsys is part of the software design sub-industry, with fellow semiconductor software designers Cadence Design Systems Inc. NASDAQ: CDNS and Ansys Inc. NASDAQ: ANSS outperforming the large-cap tech sector as a whole and showing good earnings estimates for the next two years.

Before you consider Synopsys, you'll want to hear this.

MarketBeat keeps track of Wall Street's top-rated and best performing research analysts and the stocks they recommend to their clients on a daily basis. MarketBeat has identified the five stocks that top analysts are quietly whispering to their clients to buy now before the broader market catches on... and Synopsys wasn't on the list.

While Synopsys currently has a Moderate Buy rating among analysts, top-rated analysts believe these five stocks are better buys.

View The Five Stocks Here

Robotics and automation are rapidly becoming essential infrastructure across healthcare, manufacturing, logistics, and many other industries.

"Physical AI" is coming to the United States, and there are four ways that investors can gain exposure to this new robotics revolution. Plus, learn which seven companies are most positioned to benefit as intelligent robots enter the workforce.

Get This Free Report

Like this article? Share it with a colleague.

Link copied to clipboard.