Pool Corporation

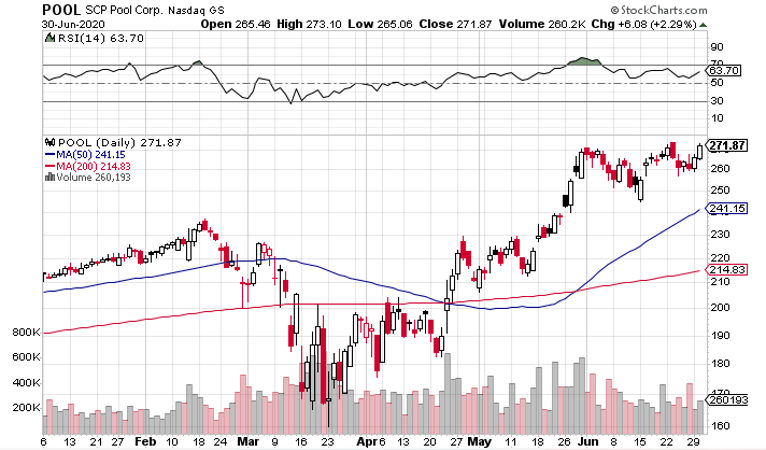

NASDAQ: POOL stock increased by more than 2% yesterday; shares are now less than 1% away from breaking out to fresh all-time highs.

POOL distributes swimming pool maintenance products, equipment, and building materials through its sales centers. Some of the company’s products are recession-proof.

Pool-owners aren’t going to skimp on chemicals, repair, and replacement products – these products aren’t too expensive, and nobody wants an ugly swamp in their backyard.

On the other hand, new pool construction is a more cyclical business. If the economy is weak, many people will delay plans to buy a pure-leisure product that costs tens of thousands of dollars.

So how has POOL fared since the pandemic hit?

Q1 2020 Results and 2020 Guidance

POOL’s Q1 2020 revenue was $677.3 million, up 13% yoy. The company’s year-round markets saw 11% growth, with California and Arizona outperforming that number. Florida and Texas underperformed a bit.

While these numbers look good, the company noticed a slowdown beginning in mid-March and sees continued weakness in Q2. It sees Q2 sales decreasing by around 5% yoy. For the second half of the year, Pool sees sales anywhere from down 7% to up 2.5% yoy. Overall, POOL sees sales growth of between down 2.5% and up 2% for full-year 2020.

POOL is taking steps to cut costs in light of the lower revenue expectations. Employee-related costs should come in $10 million lower than in 2019, due to a hiring freeze and an incentive-based compensation model (that existed pre-pandemic).

But POOL could face pricing pressure if competitors decide to lower prices in a slow market, which could push margins lower.

Segment Breakdown

As touched on earlier, certain pool products are more likely to be affected than others in a tough market.

In Q1, POOL’s chemical sales were up 16% yoy and equipment sales were up 18% yoy. While building material sales were up 14% in Q1, this number could be deceiving, as the pandemic only started to really affect demand late in Q1.

In the Q1 earnings call, POOL CEO Peter D. Arvan said, “It is worth pointing out again that we also saw slowing construction and remodel activities starting in late March in several markets that were affected by state and local orders helping to -- or curtailing Pool renovation construction and opening. Spending on maintenance and repair is continuing at normal levels across most of our markets based on April activity.”

It’s hard to see building material demand returning to pre-March levels until the pandemic is firmly behind us.

But will POOL look like a good value once coronavirus headwinds are a thing of the past?

Long-Term Valuation

POOL is trading around 45x projected 2020 earnings and around 37x projected 2021 earnings.

That valuation definitely prices in some growth, which POOL will not experience this year. But we can take a look back at POOL’s path leading up to 2020. Here are its annualized revenue and net income growth numbers, respectively, over a few intervals:

- Yoy – 8.96% and 10.22%

- 3 years – 8.02% and 18.83%

- 5 years – 7.44% and 17.72%

- 10 years – 7.90% and 29.67%

Revenue growth didn’t touch double digits over any of the intervals, which is concerning for a company that is trading at such a rich valuation. Furthermore, net income growth is far outpacing revenue growth, showing that POOL is cutting costs wherever it can, a sign of a maturing company.

Bottom line, it’s tough to see a path over the next few years to a reasonable multiple of 15-20x earnings, making POOL a pass as a value play.

That said, the chart looks appealing and makes a short-term play tempting.

Technicals

POOL has had sound price action over the past few months. In mid-February, shares touched then all-time highs of around $236. The broad market dip over the subsequent month sent shares down to $159. But POOL quickly climbed back to $229, then set up in a base between $206 and $229 for a month.

In mid-May, it had an explosive breakout above $229 and the old high of $236, quickly surging above $270. Shares have spent the past month basing between $244 and $273.

You have two potential entry points:

- A breakout above the recent all-time high (and top of the base) of $273.

- A pullback to the bottom of the base in the mid-$240s – the 50-day moving average could also meet shares around the mid-$240s in this scenario.

But with the unjustifiable valuation, is it prudent to get into POOL?

The Verdict

To reiterate, I don’t see POOL as a good value at current levels. There’s not much evidence to suggest it will grow into its valuation anytime soon.

That doesn’t change the fact that the chart looks great. So if POOL breaks out or pulls back to the mid-$240s, you should consider getting in with a tight stop-order.

Before you make your next trade, you'll want to hear this.

MarketBeat keeps track of Wall Street's top-rated and best performing research analysts and the stocks they recommend to their clients on a daily basis.

Our team has identified the five stocks that top analysts are quietly whispering to their clients to buy now before the broader market catches on... and none of the big name stocks were on the list.

They believe these five stocks are the five best companies for investors to buy now...

See The Five Stocks Here

With the proliferation of data centers and electric vehicles, the electric grid will only get more strained. Download this report to learn how energy stocks can play a role in your portfolio as the global demand for energy continues to grow.

Get This Free Report