This Is Why You Should Buy General Mills

This Is Why You Should Buy General Mills

General Mills (NYSE:GIS) has a few things going for it that make it a Buy before it reports earnings later this week. Among them are its positioning as a safe-haven consumer staples brand, its outlook for revenue, the value, and the dividend. The recent pull-back in prices is cause for concern but, in today's environment, it should be viewed as a buying opportunity for income investors.

General Mills Will See Growth

The analysts are bullish on General Mills growth outlook for the fiscal first quarter of 2021, the calendar 3rd, but a little less so for the year. Revenue is projected to grow by 10% in the quarter but fall about -2.0% for the year. The mitigating factors are last years of explosive growth, General Mills’ tendency to beat consensus and the longer-term outlook.

Regarding last year’s growth, the company saw revenue surge by 20% in the 4th quarter, 5.0% for the year, due to the uptick in stay-at-home demand, and that is a tough comp to beat. Even so, General Mills tends to beat consensus most of the time so the question really is how much will it beat consensus by? The trends point to solid activity if not growth for this quarter and the foreseeable future so I expect to see good things in the report. Longer-term, revenue is projected to grow again from F21 to F22 and incrementally thereafter.

General Mills Is A Good Dividend Payer

General Mills is a high-quality dividend payer yielding over 3.0% with shares trading near $58. That’s about double the average S&P 500 company and more than twice as safe. The company carries some debt but not too much leaving the balance sheet in great shape. The company is well-capitalized with ample coverage and plenty of free-cash-flow. Looking at the history, General Mills hasn’t increased its distribution for the last two years but it is a dividend grower on-balance. There have been 28 periodic increases since the distribution was started in 1990 and the company is on track to continue that trend. Even if General Mills doesn’t increase the payout the yield is enough to keep me interested.

General Mills Is A Value Any Way You Look At It

Value is something I have been urging investors to buy for the second half and General Mills is a value. The company trades at roughly 16X its forward earnings which makes it a value relative to the broader S&P 500 (NYSEARCA:SPY) and the Consumer Staples sector (NYSEARCA:XLY). The S&P 500 is trading about 21.7X its forward earnings and the most highly-valued staples stocks are much higher than that. Hormel (NYSE:HRL) and Clorox (NYSE:CLX), the most highly-valued of the staples stocks, are both trading near 28X their earnings. There are other, deeper, values in the staples sector like Kraft-Heinz (NASDAQ:KHC) but it just surprise investors with some restructuring news that has shares in near free-fall.

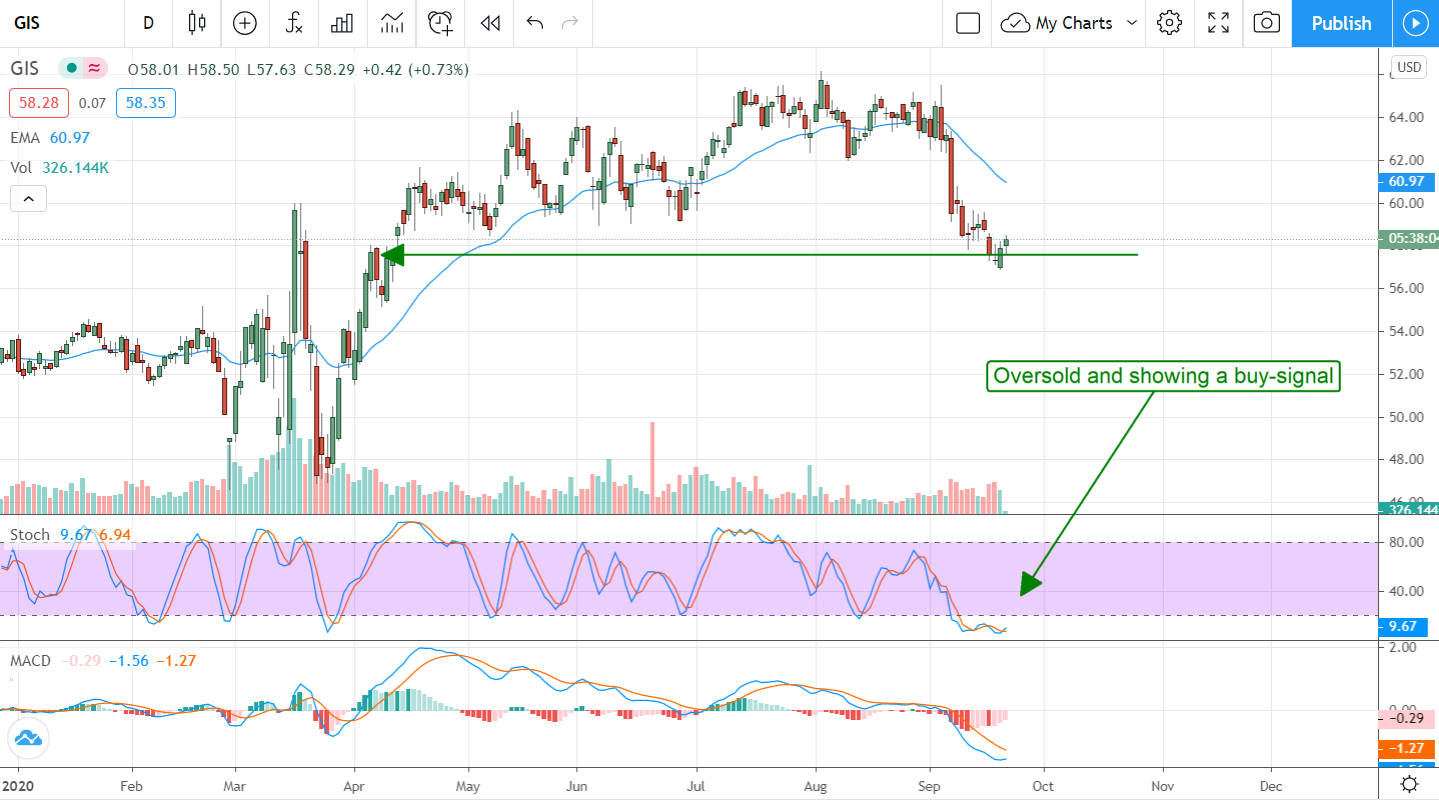

The Technical Outlook: General Mills Is Deeply Oversold

Shares of General Mills have been in correction mode along with the broader market and, like the broader market, beginning to show signs of bottoming. The stock is bouncing off of a support level that is coincident with price action in February and March so it could be a strong bottom. The indicators are still a little mixed but show a couple of noteworthy signals including 1) stochastic is oversold at support 2) stochastic is showing a strong buy signal and 3) bearish momentum has peaked and very close to reversising. A strong report on Thursday could be the trigger to get the bulls running again.

Before you consider General Mills, you'll want to hear this.

MarketBeat keeps track of Wall Street's top-rated and best performing research analysts and the stocks they recommend to their clients on a daily basis. MarketBeat has identified the five stocks that top analysts are quietly whispering to their clients to buy now before the broader market catches on... and General Mills wasn't on the list.

While General Mills currently has a Hold rating among analysts, top-rated analysts believe these five stocks are better buys.

View The Five Stocks Here

Discover the 10 Best High-Yield Dividend Stocks for 2025 and secure reliable income in uncertain markets. Download the report now to identify top dividend payers and avoid common yield traps.

Get This Free Report

Like this article? Share it with a colleague.

Link copied to clipboard.