Trex NYSE: TREX

Trex NYSE: TREX reported its fourth-quarter earnings a month ago to the day. The wood-alternative decking manufacturer indicated that its revenue growth rate could slow a bit in 2021. That was enough to send shares, which were trading at more than 50x forward earnings at the time, down 9%. An early March rally quickly fizzled out, and now shares are right around where they were the day after earnings.

Trex is still trading at a shade under 49x forward earnings, but the company’s long-term growth outlook remains strong. Let’s explore why it’s wise to look at this post-earnings dip as a buying opportunity.

2021 Guidance is Solid, All Things Considered

2020 was a record year for Trex. For the full-year, consolidated net sales rose 18% yoy to $881 million. The fourth quarter was even better, with consolidated net sales increasing 39% yoy to $228 million.

The company expects “first-quarter consolidated net sales to range from $235 million to $245 million, representing year-on-year growth of 20% at the midpoint.” That would be a quarter-over-quarter slowdown, but an acceleration from the full-year 2020 growth rate. Not bad at all.

But Trex was vague about its full-year outlook, only saying that it sees “another year of strong double-digit growth.” Does that mean 10% or 25%? Nobody can say for sure, but the ambiguity concerned investors.

But 2021 full-year revenue growth of 10-15% would still be pretty good. Here’s why:

The pandemic forced people to stay at home for most of last year. As a result, many of these people wanted to make their living arrangements more comfortable. Which includes building a new deck. But there is a lot of flexibility as to the timing of building a new deck – this isn’t like fixing your car. You can bet that a lot of people who were tentatively planning to build a new deck sometime in the future decided to do it in 2020. Combine that with low-interest rates – which apply not only to mortgages, but also to home equity loans – and you have a perform storm for a new deck boom.

So Trex’s 2020 results benefited from a pull-forward effect at the expense of 2021. When you look at it that way, the fact that Trex expects to see double-digit growth in 2021 – even if it turns out to be low double-digit growth – becomes impressive.

Trex is Set for Strong Growth Deep Into the 2020s

Trex has two tailwinds that should keep revenue growth high for years to come.

- Interest rates should stay really low for at least a couple more years.

The Fed has signaled that it plans to keep its benchmark short-term interest rate near zero until at least 2023. Though the rate on 30-year mortgages just ticked above 3% for the first time since last summer, that is still, historically speaking, an extremely low rate. Homeowners should be able to take out home equity loans at attractive rates for a while.

- There’s the switch from wood decking products to composite decking products.

On the Q4 earnings call, management said, “We estimate that composites gained approximately 200 basis points of share from the traditional wood market in 2020 and we are looking ahead to similar, if not faster conversion rates in future years.” Trex added that composite products still have just a “22% share of the decking market.”

There is clearly going to be high demand for Trex’s products going forward. Trex, for its part, is taking steps to ensure that it will be able to satisfy that demand. The company invested in new plants in Virginia and Nevada. These investments will combine to “increase production capacity by approximately 70% when compared to 2019 volume levels.”

How Should You Play Trex?

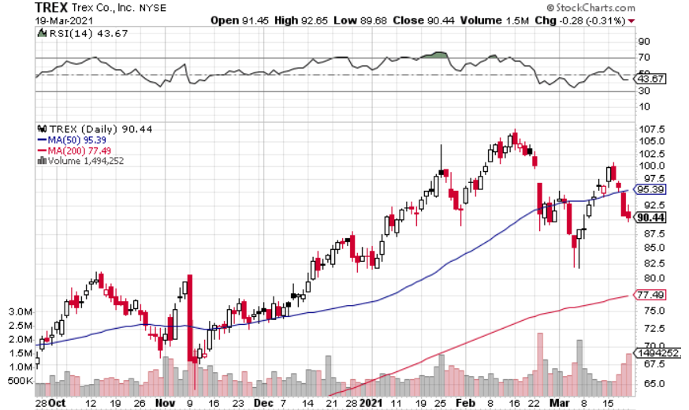

Trex shares look like an excellent value at around $90 a share. That said, shares look like they could be headed lower.

On Thursday, TREX dipped below the 50-day moving average on high volume. On Friday, shares dropped again – on even higher volume. Friday’s session marked the third consecutive session where shares closed lower on higher volume than the previous day.

There is momentum to the downside – for the time being. It may be wise to wait for a retest of the early March lows before getting in.

Before you consider Trex, you'll want to hear this.

MarketBeat keeps track of Wall Street's top-rated and best performing research analysts and the stocks they recommend to their clients on a daily basis. MarketBeat has identified the five stocks that top analysts are quietly whispering to their clients to buy now before the broader market catches on... and Trex wasn't on the list.

While Trex currently has a Hold rating among analysts, top-rated analysts believe these five stocks are better buys.

View The Five Stocks Here

The AI boom is creating opportunities across semiconductors, cloud computing, enterprise software, infrastructure, cybersecurity, and automation.

Inside this report, you’ll find 10 companies positioned to benefit as artificial intelligence moves from hype to real-world deployment and becomes a core growth driver for corporate America.

Get This Free Report

Like this article? Share it with a colleague.

Link copied to clipboard.