Freeport-McMoRan Inc. NYSE: FCX came into 2026 riding a wave of bullish sentiment. The company is one of the world’s leading copper miners at a time when basic materials stocks, in general, and mining stocks, in particular, are considered among the safest investments.

Freeport-McMoRan Today

FCX

Freeport-McMoRan

$63.43 +3.44 (+5.73%) As of 03:59 PM Eastern

This is a fair market value price provided by Massive. Learn more. - 52-Week Range

- $35.15

▼

$72.28 - Dividend Yield

- 0.47%

- P/E Ratio

- 31.24

- Price Target

- $70.27

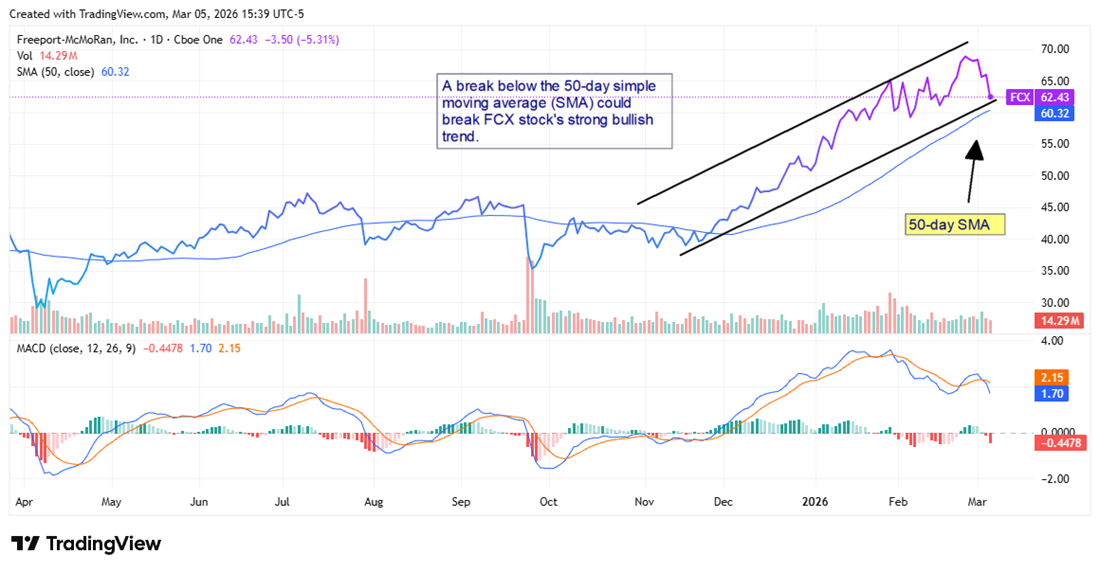

However, after surging nearly 20% since its earnings report on Jan. 22, FCX stock has given back nearly all of those gains. FCX stock recently closed near $62, hovering close to its 50-day moving average around $60.

For investors who missed the November 2025 rally, this sell-off may seem puzzling.

But dig a little deeper and a more nuanced picture emerges. That is, the long-term bull case remains largely intact. That argues for a buy-the-dip opportunity in FCX stock. But near-term valuation concerns and geopolitical complexity may send the stock lower first.

The Grasberg Factor: A Calculated Bet on Indonesia

The Grasberg mine in Papua, Indonesia, is one of the world's largest copper mines and one of its largest gold mines. It’s also central to the bull case for Freeport-McMoRan.

On Feb. 18, Freeport announced that it had restructured its relationship with the Indonesian government. Specifically, the company traded a majority stake in the Grasberg operation to state-owned PT Indonesia Asahan Aluminium (Inalum) in exchange for operational continuity and a long-term contract of work.

The arrangement locked in Freeport's right to operate through at least 2041, providing a runway long enough to matter enormously when you consider where copper demand is headed.

This was an example of pragmatic dealmaking under pressure. And shareholders sent FCX stock to its all-time high within a week of the announcement.

However, with the stock moving lower, it seems investors may be looking at the trade-off. That is, Freeport now holds a minority economic interest in the mine versus its prior majority position. That means lower per-share earnings leverage to Grasberg's output than the company once enjoyed.

That said, Grasberg's ore body is so large, and its gold and copper grades so rich, that even a minority interest generates meaningful cash flow. In other words, this is not a diminishing asset. That cash flow will become more valuable in a world increasingly electrified by technologies that require copper.

The Copper Demand Thesis Is Not Going Away

The long-term bull case for FCX ultimately rests on copper, and that story has never been stronger. In 2022, investors were focused on electric vehicles (EVs) and renewable energy infrastructure. In 2026, that story now includes grid-scale battery storage and data centers.

Freeport-McMoRan MarketRank™ Stock Analysis

- Overall MarketRank™

- 97th Percentile

- Analyst Rating

- Moderate Buy

- Upside/Downside

- 10.8% Upside

- Short Interest Level

- Healthy

- Dividend Strength

- Weak

- News Sentiment

- 1.12

- Insider Trading

- N/A

- Proj. Earnings Growth

- 34.18%

See Full AnalysisThe demand for copper is surging. Supply, meanwhile, is not keeping pace. There are three key reasons for that.

- New large copper deposits are increasingly rare.

- Many are located in geopolitically difficult regions.

- The ones that are accessible require years and billions of dollars to bring online.

Freeport, with world-class assets in Arizona, Peru, and Indonesia, is one of a small number of companies capable of meeting that demand at scale.

Analysts who track the copper market broadly agree that the structural deficit expected to emerge in the late 2020s has not been priced out of existence. However, macroeconomic noise (i.e., concerns about Chinese economic growth and the effects of higher interest rates on industrial demand) has been a noisy obstacle. Nevertheless, the electrification tailwind is generational.

Gold Adds a Second Engine

Adding to the bull case for FCX stock is the company’s exposure to gold. Grasberg is not a copper mine that produces a little gold on the side; it is a genuine dual-commodity powerhouse.

In the past, that may not have meant much. But it does today. Gold is in a multi-year bull cycle, driven by central bank accumulation, de-dollarization trends, geopolitical uncertainty, and investor demand for hard assets. With gold prices sustaining a multi-year bull cycle, the revenue contribution from Grasberg's gold output is increasingly material to Freeport's overall earnings profile.

This gold exposure acts as a partial hedge against copper price volatility and provides FCX with a revenue stream operating in a favorable pricing environment, largely independent of industrial demand concerns. For long-term investors, that dual-commodity structure is a genuine differentiator among the major mining stocks.

The Chart Is Sending a Warning Signal

The technical picture tells a cautionary tale for short-term positioning. FCX rallied strongly from roughly $38 in October 2025 to a peak just above $70 in early February 2026. A move of more than 80% in roughly four months almost always requires consolidation.

The moving average convergence/divergence (MACD) has crossed bearish, with the signal line pulling away from a declining MACD line. Combined with the stock breaking below its recent trading range, momentum favors more downside—or at best a sideways grind—before the next leg higher.

The 50-day moving average at $60.32 represents the first meaningful support level. A sustained break below that would open the door to a test of the $55 area, which was a prior consolidation zone on the way up.

Before you consider Freeport-McMoRan, you'll want to hear this.

MarketBeat keeps track of Wall Street's top-rated and best performing research analysts and the stocks they recommend to their clients on a daily basis. MarketBeat has identified the five stocks that top analysts are quietly whispering to their clients to buy now before the broader market catches on... and Freeport-McMoRan wasn't on the list.

While Freeport-McMoRan currently has a Moderate Buy rating among analysts, top-rated analysts believe these five stocks are better buys.

View The Five Stocks Here

With the proliferation of data centers and electric vehicles, the electric grid will only get more strained. Download this report to learn how energy stocks can play a role in your portfolio as the global demand for energy continues to grow.

Get This Free Report