Okta’s NASDAQ: OKTA fiscal Q1 2027 earnings report changed everything, as it revealed the company's strength and cash flow were driven by AI-focused demand. While AI is disrupting SaaS stocks, the disruption is favorable, contrary to expectations, with cybersecurity at the forefront. The need is simple—AI must be secure at all levels. Without security, AI is untrustworthy at best and dangerous at worst, and Okta is central to securing the global tech ecosystem.

Okta Today

$138.50 +2.40 (+1.76%) As of 07/24/2026 04:00 PM Eastern

- 52-Week Range

- $62.66

▼

$157.00 - P/E Ratio

- 100.36

- Price Target

- $121.81

Okta’s cloud-native, vendor-neutral approach to ID security means no vendor lock-ins and the largest, broadest addressable market among its peers. The system also integrates seamlessly, has nearly 100% uptime, and offers easy-to-use features that enable single sign-on for employees and instant on- and off-boarding for HR teams.

The takeaway is that organizations and enterprises that need to secure identities and access (including agentic AI) can do so with Okta, regardless of which vendor provides the technology to be secured.

Regarding agentic AI, it drives an exponential increase in access requests, which in turn drives demand for Okta’s services.

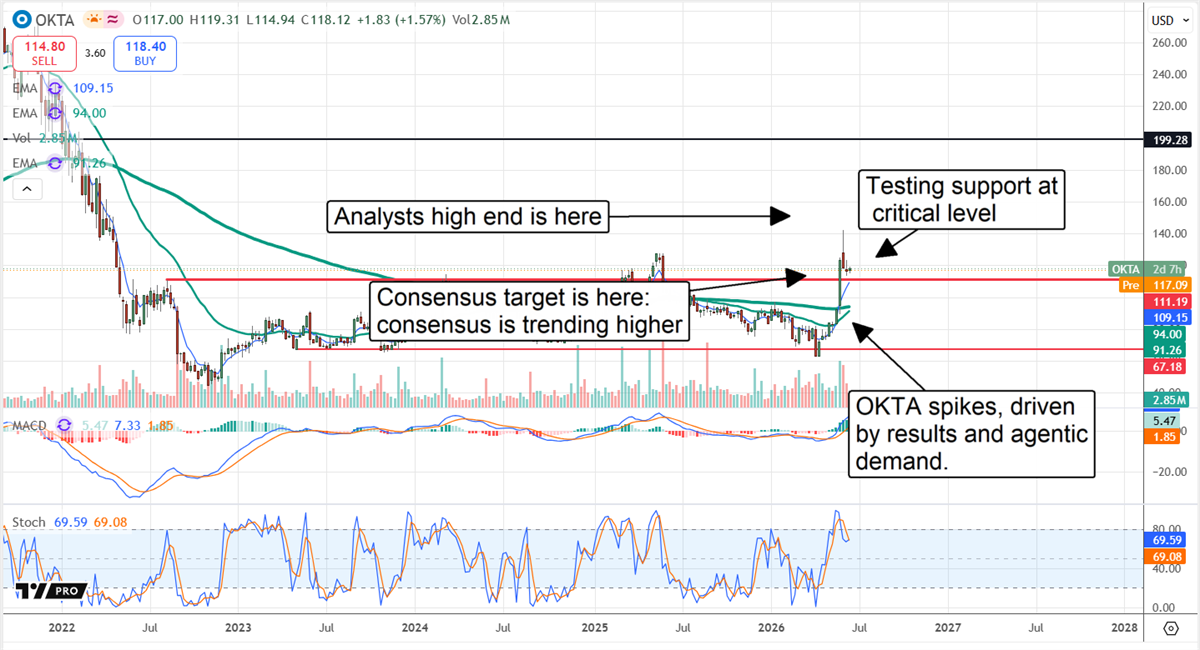

Okta’s AI-Driven Price Spike Supported by Analysts

Okta’s price spike itself is telling. The market surged by more than 30% the week of the release, indicating robust support at a cluster of moving averages. The cluster of moving averages is significant, indicating a market with forces aligned and a hard bottom in price action.

OKTA’s price has broken to a 12-month high and is now at a four-year high, indicating shifting market dynamics and a high probability of a market reversal. The story as of mid-June is that profit-taking has capped gains, but support remains at the high end of the previous range, setting the stage for another rally this summer.

Analyst trends are also central to the stock price outlook, having strengthened following the Q1 release. MarketBeat tracked 25 revisions in the first week, and all but four were price target increases. Three of the four outliers were reaffirmed targets, aligning with a forecast for consensus-or-better pricing, while the single downgrade was offset by a price target increase to an above-consensus level.

The critical takeaway from the analyst data is that the consensus of fresh targets is just over $118, an 18% increase from the pre-release level, including the new high target of $150. The $118 consensus implies a modest upside relative to the critical support target, while the $150 high suggests that another multiyear high will be set. In this scenario, the consensus trend provides support for price action, while the high end leads the market. Assuming upcoming releases extend the trends revealed in Q1, the analysts' price target forecasts will continue strengthening and leading this market higher.

Institutional data suggest downside risk is limited this summer. The group owns more than 85% of the stock, providing a solid support base, and it shifted from distribution in Q1 to accumulation in Q2. The shift aligns with the April stock price bottom, strengthening it as a support target, and plays into the May/June stock price advance. The likely outcome is that this group retains its bullish posture in 2026, potentially accelerating accumulation as subsequent reports are released.

Okta Builds Momentum in Q1: Raises Guidance, Guidance Is Cautious

Okta had a solid quarter in Q1 with revenue of $765 million, growing by 11.2% year-over-year and outpacing MarketBeat’s reported consensus by a slim margin. Strength was driven by agentic demand and compounded by forward-looking metrics, which suggest acceleration in upcoming quarters. Remaining performance obligation, a measure of contracted business, grew by 16%, suggesting the Q2 and full-year guidance updates were cautious. Management expects growth to continue and exceed consensus, but only 9% in the current quarter and 9.5% for the year.

Margin and earnings were also strong. The company managed costs and spending, resulting in adjusted earnings growth exceeding forecasts by more than 600 basis points. More importantly, strong earnings and cash flow bolster the capital return outlook, which is aggressive share buybacks. Q1 activity reduced the count by more than 2.2% on average, providing investors with significant leverage; the Q1 results and cash flow suggest the pace will be continued in upcoming quarters and may accelerate.

Okta’s balance sheet provides no red flags in 2026. The company operates without debt, has ample cash, and offers value for investors. Q1 highlights include increased cash and equivalents, reduced liabilities, and steady equity despite reinvestment and buybacks. Looking ahead, the likely outcome is that cash flow and free cash flow will continue to support growth and capital returns, while maintaining fortress-like balance metrics.

Before you consider Okta, you'll want to hear this.

MarketBeat keeps track of Wall Street's top-rated and best performing research analysts and the stocks they recommend to their clients on a daily basis. MarketBeat has identified the five stocks that top analysts are quietly whispering to their clients to buy now before the broader market catches on... and Okta wasn't on the list.

While Okta currently has a Moderate Buy rating among analysts, top-rated analysts believe these five stocks are better buys.

View The Five Stocks Here

The AI boom extends far beyond the biggest tech names. Discover 10 companies supplying the memory, storage, networking, semiconductor manufacturing, and power infrastructure that make AI possible. Learn where the next wave of AI investment opportunities may emerge—and the key risks investors should watch as the global AI buildout accelerates.

Get This Free Report

Like this article? Share it with a colleague.

Link copied to clipboard.