Despite soaring energy prices and geopolitical tension, travel demand remains strong as the summer kicks off. The U.S. Travel Association projects inflation-adjusted travel spending to grow 1% in 2026 and 3% in 2027, with international travel in the U.S. rebounding due to the World Cup. Earlier this month, CoStar and Tourism Economics upgraded their U.S. RevPAR (revenue per available room) forecast to 2.8% year-over-year (YOY) following a 4.0% figure in Q1 2026, the highest quarterly RevPAR number on record.

Naturally, the travel sector is booming, right? Not so fast, my friend. Hotel stocks are making new highs, but airline, cruise line, and other travel stocks are lagging both the broader market and their hotel industry peers. Why is one subsector winning big while the rest of the industry lags? The answer, of course, lies in the Strait of Hormuz.

Oil Is the Travel Sector’s Macro Sorting Mechanism

Oil prices have been elevated above $90 per barrel since early March when Iran closed the Strait of Hormuz. High energy prices have squeezed consumers, yet travel demand remains firm. However, oil has become a sorting mechanism in the travel industry, and the market is re-rating the sector based on fuel exposure in earnings, not raw demand.

Airlines: Fuel is one of the three biggest cost line items for any airline, and consistently high jet fuel prices are cutting into airline profits. The U.S. Global Jets ETF NYSE: JETS is down more than 2% year-to-date (YTD), and the best-performing airline stock, Delta Air Lines Inc. NYSE: DAL, is also the most hedged since it owns a refinery.

Online Travel Agencies (OTAs): OTAs aren’t insulated from the oil shock despite having no fuel costs. Tapped-out vacationers are eschewing international travel for cheaper domestic trips that reduce overall spend and slash OTA fee revenue. Airlines could also offset fuel cost increases by slashing commissions paid to OTAs for their listings. Booking Holdings Inc. NASDAQ: BKNG, the largest publicly-traded OTA, is down more than 25% YTD.

It’s not hard to see why hotels have outperformed. Hotels are best positioned to monetize travel demand because they don’t have to cover fuel costs. And some of the industry leaders aren’t even paying the mortgage on the real estate anymore.

2 Hotel Stocks Setting New Highs This Summer

The three hotel stocks listed here all have a common theme: a franchise business model. Under this model, a hotel franchisee bears all cyclical risks, including mortgage costs, labor, depreciation, insurance, and utilities. The brand collects a percentage of gross room revenue and other fees, and allows the operator to use their name and access their booking and loyalty engines. A capital-light system with recurring revenue is ideal for a macro shock environment, which is why these stocks have soared to new highs this year.

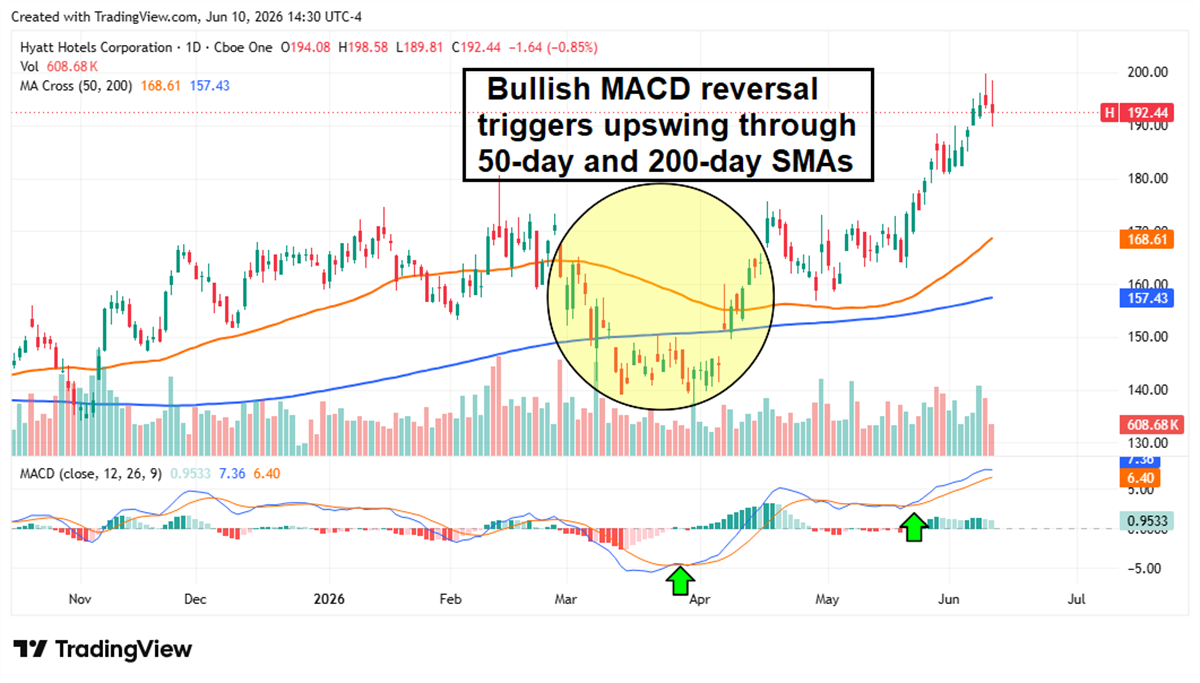

Marriott: Fee Machine Firing on All Cylinders

Marriott International Today

MAR

Marriott International

$400.70 -1.84 (-0.46%) As of 02:04 PM Eastern

This is a fair market value price provided by Massive. Learn more. - 52-Week Range

- $253.76

▼

$410.98 - Dividend Yield

- 0.73%

- P/E Ratio

- 42.06

- Price Target

- $384.73

Non-RevPAR revenue streams are what set

Marriott International Inc. NYSE: MAR apart from its peers.

Card fees were up 37% YOY in Q1 2026, and management boosted full-year gross fee guidance to a range of $5.93 billion to $5.99 billion.

The pipeline is also robust; a record 618,000 rooms, 43% of which are already under construction. Q2 RevPAR guidance was also boosted to a top range of 2.5%.

MAR shares are also enjoying strong technical momentum. The 50-day moving average has provided support for nearly a year, and the Moving Average Convergence Divergence (MACD) indicator is signaling a bullish momentum uptick. The fundamentals and technicals confirm the same story, and that’s more upside ahead.

Hilton: The Hotel Industry’s Purest Compounder

Hilton Worldwide Today

HLT

Hilton Worldwide

$346.14 +0.20 (+0.06%) As of 02:04 PM Eastern

This is a fair market value price provided by Massive. Learn more. - 52-Week Range

- $243.53

▼

$351.70 - Dividend Yield

- 0.17%

- P/E Ratio

- 52.85

- Price Target

- $349.45

Net unit growth is the catalyst for

Hilton Worldwide Holdings Inc. NYSE: HLT. The company reported 131 new hotel openings during its

Q1 2026 earnings release, with industry-leading net unit growth of 6.3%.

Hilton is targeting 6-7% unit growth over the rest of the year, and it is confident enough in this projection to raise RevPAR growth despite Middle East headwinds. System-wide RevPAR of 3.6% outperformed expectations, and a record 527,000 rooms are currently in the pipeline.

HLT shares have traded flat since the start of April, but remain up more than 15% YTD, and there’s evidence that the next leg of the rally is imminent. Support remains strong along the 50-day moving average, and the Relative Strength Index (RSI) has now pushed back into bullish territory.

The stock trades at a premium multiple of 37 times forward earnings, but the growth rate and capital returns ($3.5 billion in buybacks and dividends scheduled for 2026) command attention.

Before you consider Marriott International, you'll want to hear this.

MarketBeat keeps track of Wall Street's top-rated and best performing research analysts and the stocks they recommend to their clients on a daily basis. MarketBeat has identified the five stocks that top analysts are quietly whispering to their clients to buy now before the broader market catches on... and Marriott International wasn't on the list.

While Marriott International currently has a Moderate Buy rating among analysts, top-rated analysts believe these five stocks are better buys.

View The Five Stocks Here

Looking for the next FAANG stock before everyone has heard about it? Click the link to see which stocks MarketBeat analysts think might become the next trillion dollar tech company.

Get This Free Report

Like this article? Share it with a colleague.

Link copied to clipboard.