Every time you refresh your brokerage app, it seems another semiconductor stock jumps 10%.

But it's not just chip stocks that are bubbling with bullish energy and earnings beats; the industrial sector is also getting in on the action. And with earnings season in full swing, some companies in the space are cruising past estimates, raising guidance, and giving their investors plenty of reason to celebrate.

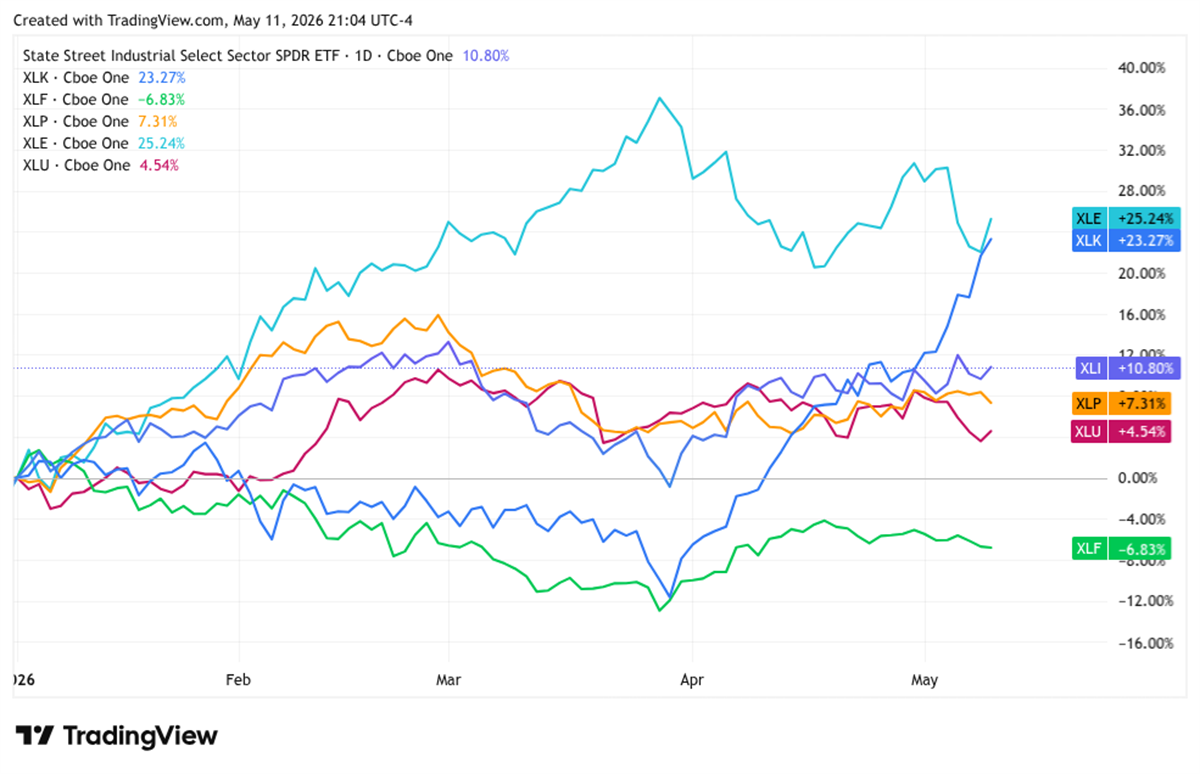

The industrial sector still trails the energy and tech sectors significantly so far in 2026. But the Industrial Select Sector SDPR Fund NYSEARCA: XLI is up more than 10% year-to-date (YTD), and several industry-specific catalysts are underway that could drive significant earnings growth.

Physical AI Buildout: One of the prevailing investment trends of 2026 has been the shift from software to hardware in the AI industry. Hyperscaler capex projections continue to reach nosebleed levels, but the constraints are no longer digital. Data centers need power generation, cooling systems, transformers, quality control equipment, and a whole host of components to ‘house’ the intelligence. These physical constraints have been a boon to industrials that manufacture the infrastructure surrounding the most sophisticated models.

Mega Cap Tech Rotation: Even without the data center buildout, industrials are likely to be the beneficiaries of more run-of-the-mill sector rotation. While semiconductors are leading the rally right now, investors have rotated out of overvalued, high-multiple tech names and into cheaper sectors like industrials. In addition to providing better value, money managers also understand that the AI revolution will be underpinned by vital physical infrastructure.

Growing Defense Backlogs: The wars in Iran and Ukraine have created a sustained tailwind as Europe and the U.S. both seek to increase defense spending and restock depleted inventories. Defense contractors' backlogs are reaching record levels, such as the nearly $200 billion order book at Lockheed Martin Corp. NYSE: LMT, which will provide steady revenue for years to come.

Three industrials reported earnings within the last week, each with its numbers rewarded by the market. But how much more upside is left? Let’s break down the reports and see which companies can sustain their momentum.

W.W. Grainger: Strong Earnings Boost Technical Momentum

W.W. Grainger Today

GWW

W.W. Grainger

$1,300.60 -70.65 (-5.15%) As of 03:59 PM Eastern

This is a fair market value price provided by Massive. Learn more. - 52-Week Range

- $906.52

▼

$1,419.91 - Dividend Yield

- 0.77%

- P/E Ratio

- 34.98

- Price Target

- $1,265.13

“For the ones who get it done” is the popular tagline of industrial supplier W.W. Grainger Inc. NYSE: GWW, but it was management that got it done in Q1 with a dazzling earnings report.

The company beat analysts' estimates on both EPS and revenue in Q1 2026, with the latter up more than 10% year-over-year (YOY).

Both the Endless Assortment and High-Touch segments grew during the quarter, and management raised full-year sales guidance and increased the dividend by 10%, marking its 55th straight year of dividend increases.

However, it wasn’t a spotless conference call. Management warned that Q2 margins could be pressured by inventory and fuel costs, and the Section 232 tariff situation remains murky at best.

GWW shares popped as much as 10% following the release, though they gave back some of those gains over the next few days.

Management was careful to temper expectations for Q2, but the technical momentum remains strong. The Relative Strength Index (RSI) is firmly in bullish territory, and the stock appears to have support along the 50-day moving average, which crossed above the 200-day moving average in February.

Rockwell Automation: AI Growth Story Outpaces Margin Headwinds

Rockwell Automation Today

ROK

Rockwell Automation

$445.66 -35.32 (-7.34%) As of 04:00 PM Eastern

- 52-Week Range

- $305.44

▼

$497.36 - Dividend Yield

- 1.24%

- P/E Ratio

- 46.33

- Price Target

- $469.33

Rockwell Automation Inc. NYSE: ROK is, in some respects, one of the original AI companies.

The $50 billion giant has been helping clients automate industrial processes for decades, and advances in AI and machine learning are accelerating its revenue.

Rockwell reported fiscal Q2 2026 results on May 5, beating EPS and revenue projections by 13% and 3.5%, respectively.

The $2.24 billion in quarterly revenue represented nearly 12% YOY growth, and management raised full-year 2026 sales guidance to a 5-9% growth range, with an EPS midpoint of $12.80.

Following the report, the stock received 11 price target boosts from analysts, including a new Street-high $525 from Morgan Stanley. Analysts now see Rockwell as a beneficiary of several growing AI trends, including factory automation and data center energy efficiency.

Technical trends point to more upside as well; shares now trade above both the 50-day and 200-day moving averages, and the Moving Average Convergence Divergence (MACD) has grown bullish since the end of March.

Powell Industries: A Crucial Cog in Data Center Infrastructure

Powell Industries Today

POWL

Powell Industries

$211.38 -8.34 (-3.80%) As of 04:00 PM Eastern

- 52-Week Range

- $69.00

▼

$328.00 - Dividend Yield

- 0.17%

- P/E Ratio

- 41.37

- Price Target

- $236.67

Markets have learned to trust Powell, but we aren’t talking about the Federal Reserve Chairman here.

Powell Industries Inc. NASDAQ: POWL is a mid-cap electrical engineering company that actually missed EPS and revenue estimates when it reported fiscal Q2 2026 results on May 5.

However, investors care more about the future than the past, and Powell’s record backlog and clean balance sheet have driven the stock to a roughly 190% YTD gain and a nearly 400% gain in the past year.

The $1.8 billion backlog is expected to provide visible revenue through fiscal 2028, and the company is currently sitting on $545 million in cash with no debt, which has management exploring capacity expansion.

If there’s one worry for POWL investors, it's that the rally appears overextended. The stock has enjoyed strong support at the 50-day moving average since the start of its rally last year, but now trades several standard deviations above trend.

The MACD is still bullish but looking increasingly unstable, with the MACD and signal lines drifting further apart. A short-term pullback might not be the worst thing following a gain of more than 30% in the past month, and would provide new investors with a better entry point on a stock that now trades at a hefty 55x forward earnings and 10x sales.

Continue following MarketBeat

Add MarketBeat as your preferred source on Google to see our latest stories in your feed.

Before you consider W.W. Grainger, you'll want to hear this.

MarketBeat keeps track of Wall Street's top-rated and best performing research analysts and the stocks they recommend to their clients on a daily basis. MarketBeat has identified the five stocks that top analysts are quietly whispering to their clients to buy now before the broader market catches on... and W.W. Grainger wasn't on the list.

While W.W. Grainger currently has a Hold rating among analysts, top-rated analysts believe these five stocks are better buys.

View The Five Stocks Here

The AI boom extends far beyond the biggest tech names. Discover 10 companies supplying the memory, storage, networking, semiconductor manufacturing, and power infrastructure that make AI possible. Learn where the next wave of AI investment opportunities may emerge—and the key risks investors should watch as the global AI buildout accelerates.

Get This Free Report