Shares of eBay Inc. NASDAQ: EBAY are about 3.8% the day after the company delivered a strong Q4 2025 earnings report. On one level, the report makes sense. The company is a pure-play on consumer spending, which has remained resilient despite conflicting macroeconomic data. Plus, eBay fits into that “discount” category of retail stocks that has performed solidly in a volatile market.

eBay Today

$107.13 -6.88 (-6.03%) As of 08/3/2026 04:00 PM Eastern

- 52-Week Range

- $78.03

▼

$119.31 - Dividend Yield

- 1.16%

- P/E Ratio

- 24.29

- Price Target

- $110.58

As for the report itself, there was a lot for investors to like. Revenue of $2.97 billion exceeded expectations of $2.87 billion. A key metric, gross merchandise volume (GMV), climbed to $21.2 billion. That was up almost 6% globally and nearly 10% in the United States. This suggests the platform is expanding and attracting more customers.

Another highlight of the report was the announcement that eBay will acquire Depop, the secondhand clothing marketplace owned by Etsy Inc. NASDAQ: ETSY, for $1.2 billion in cash. The move is a strategic attempt to capture more of the Gen Z and Millennial customer base.

Like many stocks with even minimal exposure to artificial intelligence (AI), EBAY stock was trading lower in 2026 ahead of the report. One solid report won’t change that, but there are several reasons to believe in eBay’s comeback.

Ads, Fashion, and the Recommerce Angle

The Q4 report showed three specific engines are doing the heavy lifting. The first is advertising. On an annualized basis, eBay is approaching $2 billion in ad revenue. This was a revenue avenue that was almost non-existent just five years ago.

Total advertising revenue was $544 million in Q4, representing GMV penetration of nearly 2.6%, with first-party ads growing over 17% to $517 million. And about 4.8 million sellers adopted at least one promoted listing product during the quarter. The takeaway for investors is that advertising is becoming an embedded behavior on the platform, not just an optional feature for power sellers.

The second growth engine comes from the company’s focus on recommerce (i.e., pre-owned and refurbished merchandise). This category accounted for over 40% of the company’s GMV in 2025 and grew at about 10% during the year. This is a category where eBay is distinct from Amazon.com Inc. NASDAQ: AMZN, and an area that the latter will be hard-pressed to replicate at any meaningful scale.

The third growth engine has more potential for now, and that’s the Depop acquisition. In 2025, the platform generated approximately $1 billion in gross merchandise sales for Etsy. But the appeal of eBay is that nearly 90% of Depop’s 7 million active buyers are under the age of 34, a demographic eBay has struggled to attract.

Plus, Depop specializes in private-label fashion, a segment that is the fastest-growing in retail. Assuming that these shoppers follow Depop to eBay, the company’s platform has a chance to gain a credible foothold that could drive revenue growth.

A Marketplace Revamp With Real Teeth—or Temporary Tailwinds?

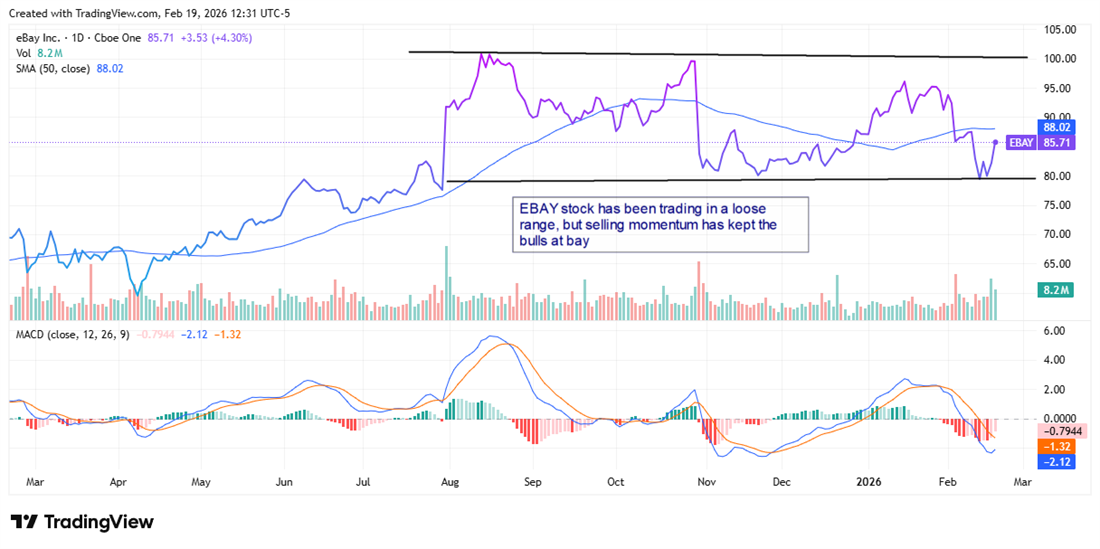

Institutional sentiment in EBAY stock has been bearish in the last three quarters, with selling outpacing buying by about $2 billion. Some of that selling may have been due to the stock's performance, which hit an all-time high in August 2025. Since that time, EBAY stock has traded in a loosely defined range with support around $80 and resistance at $100.

However, the eBay analyst forecasts on MarketBeat show that analysts have been quick to raise their price targets on EBAY stock. Several of the new price targets are above the consensus price of $96.52, a 12% increase from the stock price as of this writing. The highest comes from Needham & Company, which raised its target price to $122 from $115.

Investors should also consider the company’s dividend. A dividend is never the right reason to buy a stock like EBAY. Investors would want to see the company investing in growth, as eBay is with the Depop deal.

Still, the dividend yield of1.35% is above the S&P 500 average, and the company has increased the dividend payout, which is now $1.16, at an average of over 14% in the last three years. Plus, the payout ratio of just over 25% is sustainable and not eating away at the company’s cash.

Risks That Investors Shouldn’t Ignore

eBay MarketRank™ Stock Analysis

- Overall MarketRank™

- 87th Percentile

- Analyst Rating

- Hold

- Upside/Downside

- 3.2% Upside

- Short Interest Level

- Healthy

- Dividend Strength

- Strong

- News Sentiment

- 0.45

- Insider Trading

- Selling Shares

- Proj. Earnings Growth

- 10.63%

See Full AnalysisWhile the bull case is compelling, there are some factors that investors should keep in mind. First, some of Q4's GMV growth was commodity-driven. Management acknowledged on the earnings call that bullion, collectible coins, and Pokémon trading cards provided meaningful tailwinds in late 2025. These are categories that are inherently cyclical and unlikely to repeat at the same rate.

Second, the Depop deal, while strategically sound, comes with near-term costs. eBay expects the acquisition to represent a low single-digit headwind to non-GAAP operating income growth and dilution to EPS growth, with accretion not expected until 2028.

Third, non-GAAP gross margin slipped nearly 80 basis points year over year. Sustainable margin expansion in the face of Amazon's logistics network and Shopify's NASDAQ: SHOP seller ecosystem remains the central question that has held EBAY stock down. It’s true that the dip in gross margin was primarily due to the scaling of managed shipping and Authenticity Guarantee programs. However, these are necessary investments and a reminder that protecting trust on a peer-to-peer marketplace carries real costs.

Before you consider eBay, you'll want to hear this.

MarketBeat keeps track of Wall Street's top-rated and best performing research analysts and the stocks they recommend to their clients on a daily basis. MarketBeat has identified the five stocks that top analysts are quietly whispering to their clients to buy now before the broader market catches on... and eBay wasn't on the list.

While eBay currently has a Hold rating among analysts, top-rated analysts believe these five stocks are better buys.

View The Five Stocks Here

The AI boom is creating opportunities across semiconductors, cloud computing, enterprise software, infrastructure, cybersecurity, and automation.

Inside this report, you’ll find 10 companies positioned to benefit as artificial intelligence moves from hype to real-world deployment and becomes a core growth driver for corporate America.

Get This Free Report