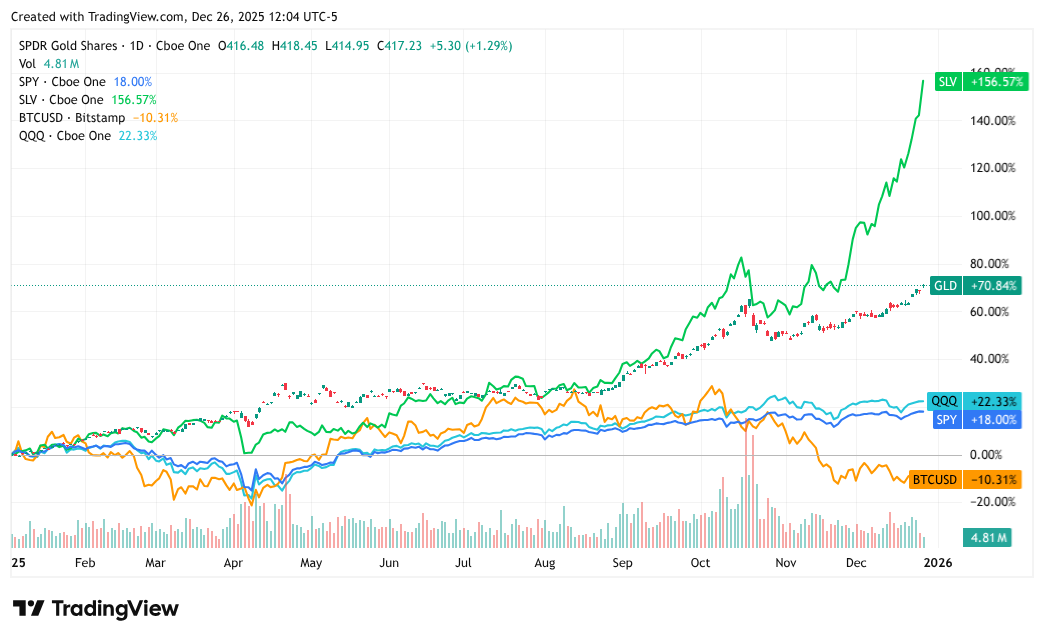

The biggest winners in your portfolio continue to be the oldest investments in existence. Gold and silver seemingly can’t be stopped, with the former up more than 70% year-to-date (YTD) and the latter posting a staggering gain of over 150% YTD. We’ve discussed the reasons why precious metals soared in 2025, and the rally still shows no signs of slowing down. Today, we’ll look at a different way to gain exposure, and it involves equities from our friends in the great white north.

Canadian Miners Could Have Currency Tailwinds in 2026

The precious metals trade has been the strongest on Wall Street this year, outpacing gains from the S&P 500, the tech-heavy Invesco QQQ ETF NASDAQ: QQQ, and Bitcoin. Investors often don’t complain about 18% gains in major stock indices, but precious metals have even beaten some of the tech sector’s most prolific AI hyperscalers in 2025. The outperformance of gold and silver highlights the uncertainty that persists in the geopolitical landscape.

Of course, investing in precious metals comes with drawbacks too. Holders of physical gold and silver face unfriendly taxation, and mining companies are often wracked with operational challenges and lengthy timelines. To invest in the mining sector, you need well-run companies with access to resources in trustworthy jurisdictions. But you also need macroeconomic tailwinds, and Canadian miners could have an additional weight removed from their sails in 2026.

Canadian miners typically perform well when gold prices rise while the CAD/USD exchange rate falls. Since Canadian miners pay their expenses in CAD but sell their gold or silver in USD, a falling Canadian dollar creates a currency tailwind for Canadian miners. However, this wasn’t the case in 2025 when a weak USD buoyed other international currencies. Despite CAD strengthening against the USD, Canadian miners still outperformed.

But now Canada’s GDP is shrinking, down 0.3% in October, and these economic red flags may prompt the Bank of Canada to cut rates faster than previously expected. In contrast, U.S. Q3 GDP was 4.3%, suggesting the Federal Reserve might take a more cautious approach to future rate cuts. If the Bank of Canada gets aggressive with cuts while the Fed holds, the CAD/USD pair should reverse course, putting the currency tailwind back in miners’ favor. If the USD strengthens against the CAD in 2026, Canadian miners should reap even larger benefits from their hauls.

3 Canadian Miners to Own as Precious Metals Continue Soaring

Currency tailwinds aren’t the only reason to own Canadian miners. Many of these companies have strong management teams and access to a wide range of “risk-free” jurisdictions. Canada is home to a wealth of mineral-rich terrain, and the government’s 2025 federal budget offers plenty of tax incentives for miners. Here are three Canadian mining stocks to add to your portfolio if you want precious metals exposure with a pinch of currency tailwinds.

Agnico Eagle Mines: Strong Growth Prospects for a Gold Pure Play

Agnico Eagle Mines Today

AEM

Agnico Eagle Mines

$143.77 -2.19 (-1.50%) As of 07/28/2026 03:59 PM Eastern

This is a fair market value price provided by Massive. Learn more. - 52-Week Range

- $122.68

▼

$255.24 - Dividend Yield

- 1.25%

- P/E Ratio

- 13.51

- Price Target

- $225.69

Gold is the primary mineral produced by Agnico Eagle Mines Ltd. NYSE: AEM, one of Canada’s most prominent mining firms with a $91 billion market cap and more than $8 billion in annual sales. The company hauled in more than 867,000 ounces of the shiny stuff in Q3 2025, helping it surpass analyst expectations for both EPS and revenue.

Agnico’s size and stability make it an attractive stock for investors; its mines are located in safe jurisdictions such as Canada, Finland, and Australia, and record gold prices have enabled the company to invest in expansion. Agnico launched 120 new drill rigs in Q3, which could add more than 1.5 million ounces to its coffers in the coming years.

Pan American Silver: Acquisitions to Stabilize Performance

Pan American Silver Today

PAAS

Pan American Silver

$43.22 -0.91 (-2.06%) As of 07/28/2026 03:59 PM Eastern

This is a fair market value price provided by Massive. Learn more. - 52-Week Range

- $26.76

▼

$69.99 - Dividend Yield

- 1.67%

- P/E Ratio

- 13.90

- Price Target

- $70.43

Pan American Silver Corp NYSE: PAAS operates out of Vancouver, but the location of its mines creates more volatility than AEM. PAAS drills in regions in countries like Peru, Argentina, Bolivia, and Mexico, which offer less geopolitical stability and therefore more risk to investors.

However, the company is attempting to address the problem with acquisition volume. Pan American previously acquired Yamana Gold to diversify operations, but the acquisition of MAG Silver’s Juanicipio mine has been a massive boon, allowing the company to boost production guidance to 22 million ounces in 2025. Pan American also reported record cash flow in Q3 2025, allowing management to raise the dividend.

Wheaton Precious Metals: High Margins and Flat Costs

Wheaton Precious Metals Today

WPM

Wheaton Precious Metals

$109.47 -2.54 (-2.27%) As of 07/28/2026 03:59 PM Eastern

This is a fair market value price provided by Massive. Learn more. - 52-Week Range

- $90.39

▼

$165.76 - Dividend Yield

- 0.71%

- P/E Ratio

- 27.64

- Price Target

- $165.55

If you want to eschew the hassle of mining, consider Wheaton Precious Metals Corp NYSE: WPM. Wheaton doesn’t actually own or operate any mines. Instead, they provide upfront capital to miners in exchange for a percentage of the mining haul, usually at a low fixed price (known as a streaming business model). While this setup means WPM is less affected by movements in the spot prices of gold or silver, it also allows for a high-margin business with very predictable expenses.

WPM has contracts with more than 40 miners worldwide, including companies operating in the U.S., Mexico, Canada, Brazil, Chile, and parts of Africa. It reported record revenue in Q3 2025, reiterating its full-year guidance of 600,000 to 670,000 Gold Equivalent Ounces (GEOs). But the real reason WPM can sustain its high valuation is thanks to its impressive margins: 55% net, the highest in the industry. And with the stock up nearly 120% YTD, investors seem to agree.

Before you consider Wheaton Precious Metals, you'll want to hear this.

MarketBeat keeps track of Wall Street's top-rated and best performing research analysts and the stocks they recommend to their clients on a daily basis. MarketBeat has identified the five stocks that top analysts are quietly whispering to their clients to buy now before the broader market catches on... and Wheaton Precious Metals wasn't on the list.

While Wheaton Precious Metals currently has a Moderate Buy rating among analysts, top-rated analysts believe these five stocks are better buys.

View The Five Stocks Here

Looking to profit from the electric vehicle mega-trend? Click the link to see our list of which EV stocks show the most long-term potential.

Get This Free Report

Like this article? Share it with a colleague.

Link copied to clipboard.