Copa Today

$152.38 -0.61 (-0.40%) As of 03:58 PM Eastern

- 52-Week Range

- $103.91

▼

$156.41 - Dividend Yield

- 4.49%

- P/E Ratio

- 8.89

- Price Target

- $168.91

is an airline stock with structural advantages, placement, and capital returns that make it a nearly perfect investment. Its positioning is as a leading Latin American service provider, offering emerging-market exposure in the critical infrastructure and services play; its structural advantage is a hub-and-spoke footprint centered on The Hub of the Americas. The Hub of the Americas is the company’s headquarters at Tocumen International Airport, a centralized location that enables ultra-efficient operations across the system.

The setup enables the region's leading service record and the #2 record globally, with an average on-time rate of about 90% and completion rates trending in the 99% range. In addition to the hub-and-spoke setup, Tocumen boasts a centralized location for quick connections, connections further enhanced by terminal placement. Passengers don’t have to worry about customs or transit when transitioning from one flight to the next. In addition, the company operates a single-type fleet, further controlling costs by limiting maintenance hassles, training needs, and parts inventory.

Copa Holdings Accelerates Growth in Q1 2026

Copa Holdings had a strong Q1, with revenue growing by 17% to just over $1 billion, evidence of its strength. The top line exceeded MarketBeat’s reported consensus by a wide margin, accelerating from the prior quarter and year due to increases in capacity and demand. The bullish detail is that passenger traffic increased by 15% on a 14% increase in capacity, helping to drive margin strength, further compounded by improved revenue per mile.

Margin news is also strong. The company managed to widen its operating and net margins despite higher costs, particularly fuel costs. GAAP earnings grew at an accelerated 20.5% pace, exceeding the consensus estimate by 73 cents or nearly 1650 basis points (bps). Looking ahead, the company issued a cautious Q2 forecast, citing fuel cost headwinds, but remained positive for the year, forecasting 17% revenue growth.

Bullish Cash Flow and Capital Return Outlook Drive CPA Price Action

Copa Dividend Payments

- Dividend Yield

- 4.49%

- Annual Dividend

- $6.84

- Dividend Increase Track Record

- 2 Years

- Annualized 5-Year Dividend Growth

- 51.76%

- Dividend Payout Ratio

- 39.88%

- Recent Dividend Payment

- Jun. 15

CPA Dividend HistoryCopa Holdings' highly efficient business enables

a healthy cash flow and capital returns, including dividends and share buybacks. Dividends are approximately 40% of earnings and reliable in 2026,

yielding approximately 4.5% with shares trading near historically high levels.

Distribution increases are expected, given the revenue and growth outlook, and will likely continue at a robust, double-digit pace in the upcoming years. Share buybacks are less aggressive but provide value, reducing the count by an average of 0.3% over the trailing 12 months (TTM).

Institutional activity is mixed, with the balance bullish but relatively flat on a trailing 12-month basis as of mid-year. However, they provide solid support, owning about 70% of the shares, and the analysts are more bullish.

MarketBeat reveals increasing coverage, firming sentiment, and rising price targets, with a consensus Buy rating and a forecast for fresh all-time highs. Short interest does not appear to be an issue. It is slightly elevated at around 4% but not alarming, more likely linked to hedging activities than outright bearish behavior.

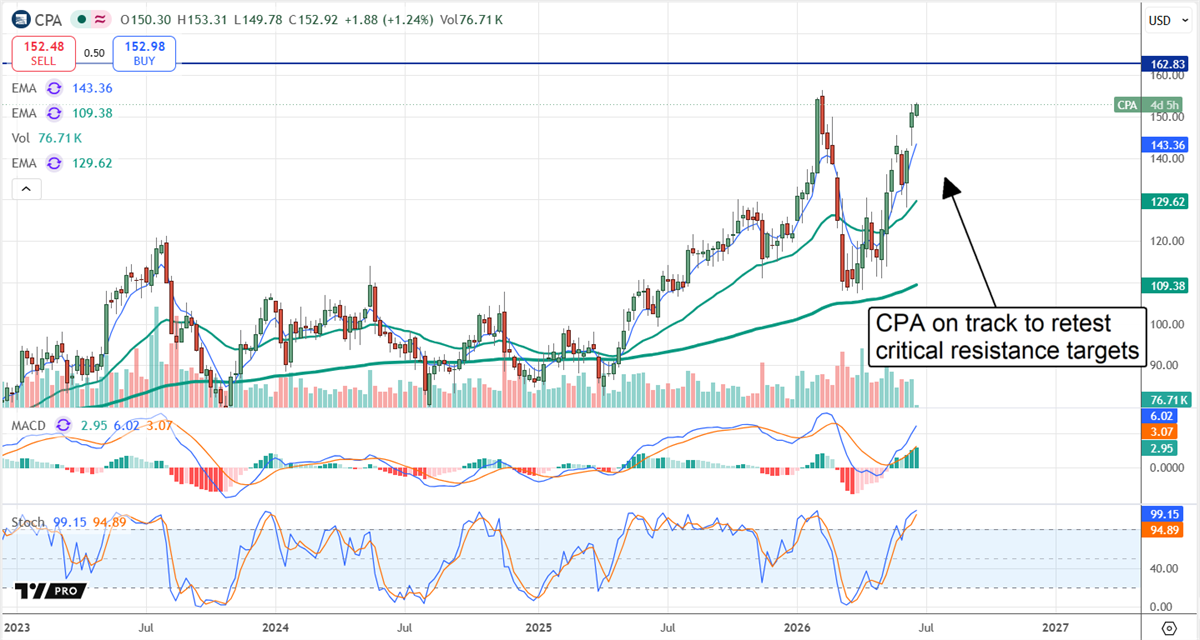

Copa Holdings Advances: Approaches Critical Threshold

Copa Holdings’ price action is bullish in Q2. The market is advancing and on track to test resistance at the existing all-time high. Bullish signals in the MACD and stochastic suggest the restest will come soon, potentially by year’s end, and new highs are possible. Setting new highs will be significant, as they will be the first fresh highs in over a decade, opening the door to a much larger movement.

In this scenario, the base case is worth the dollar value of the existing trading range, which runs from $120. A move to $280 is possible, assuming a fresh high is set. If not, CPS shares may remain range-bound indefinitely, but that is not expected, given the growth and capital return outlook.

Copa Holdings' business is supported by robust demand in a major emerging market region. Latin America is a leading growth pillar internationally, driven by industrialization and middle-class expansion, which are fueling demand for business and leisure travel. Consistent capital returns are expected over time. The biggest risk for Copa is geopolitical. Not only can conflicts outside the region impair travel demand, but internal issues could disrupt business. Numerous international agreements enable easy, free-flowing traffic among many of the nations served.

Copa Holdings’ balance sheet is not among its risks. The company maintains low leverage and ample cash, which equates to 40% of TTM revenue as of the end of Q1. The likely outcome is that Copa Holdings will continue to execute its strategy, investing in growth while returning capital to investors.

Before you consider Copa, you'll want to hear this.

MarketBeat keeps track of Wall Street's top-rated and best performing research analysts and the stocks they recommend to their clients on a daily basis. MarketBeat has identified the five stocks that top analysts are quietly whispering to their clients to buy now before the broader market catches on... and Copa wasn't on the list.

While Copa currently has a Buy rating among analysts, top-rated analysts believe these five stocks are better buys.

View The Five Stocks Here

Click the link to see MarketBeat's list of seven stocks and why their long-term outlooks are very promising.

Get This Free Report

Like this article? Share it with a colleague.

Link copied to clipboard.