Post (NYSE:POST - Get Free Report) is anticipated to release its Q2 2026 results after the market closes on Thursday, May 7th. Analysts expect Post to post earnings of $1.74 per share and revenue of $2.0753 billion for the quarter. Investors may review the information on the company's upcoming Q2 2026 earning report for the latest details on the call scheduled for Friday, May 8, 2026 at 9:00 AM ET.

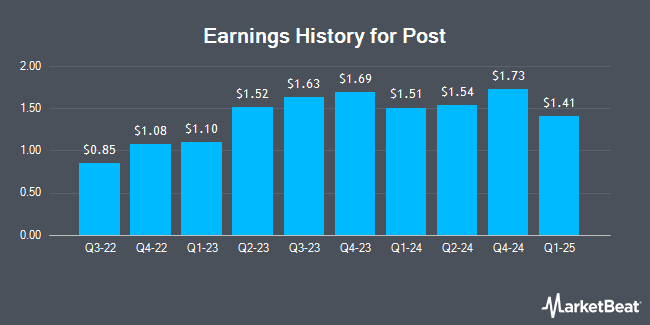

Post (NYSE:POST - Get Free Report) last posted its earnings results on Thursday, February 5th. The company reported $2.13 earnings per share for the quarter, beating the consensus estimate of $1.66 by $0.47. Post had a net margin of 3.82% and a return on equity of 12.37%. The firm had revenue of $2.17 billion during the quarter, compared to the consensus estimate of $2.18 billion. During the same quarter last year, the firm earned $1.73 EPS. The firm's revenue for the quarter was up 10.2% on a year-over-year basis. On average, analysts expect Post to post $7 EPS for the current fiscal year and $8 EPS for the next fiscal year.

Post Stock Down 0.9%

Post stock opened at $102.17 on Thursday. Post has a fifty-two week low of $94.13 and a fifty-two week high of $117.28. The company has a debt-to-equity ratio of 2.15, a quick ratio of 1.02 and a current ratio of 1.90. The firm has a 50 day moving average price of $101.59 and a 200 day moving average price of $102.34. The company has a market capitalization of $4.89 billion, a PE ratio of 18.89 and a beta of 0.44.

Post News Summary

Here are the key news stories impacting Post this week:

- Positive Sentiment: Sector peer beats suggest consumer staples resilience — Kimberly‑Clark (KMB) reported a Q1 beat, showing demand/price execution holding in household staples; that can be a modest tailwind for POST’s retail packaged‑food businesses if investors view staples as defensive. Kimberly‑Clark Q1 Earnings Beat

- Positive Sentiment: Pizza/consumer dining metrics showing strength — Domino’s (DPZ) got bullish analyst commentary after Q1, indicating pockets of consumer spending in food that could support some of POST’s categories (retail and away‑from‑home). Domino’s Analyst Updates

- Neutral Sentiment: Energy/commodity earnings with mixed implications — BP posted a strong Q1 (better operating cash), which reflects oil/energy volatility that can have mixed effects: higher input/transport costs for CPGs but also an inflation/real‑asset backdrop that sometimes supports defensive staples. BP Q1 Rebound

- Negative Sentiment: Corn futures are climbing — rising corn prices increase input costs for cereal and other grain‑based products, pressuring margins if Post can't fully pass costs through to retailers. Commodity inflation is a direct margin risk for POST’s cereal and snacks businesses. Corn Midday Gains

- Negative Sentiment: Foodservice weakness flagged by a distributor miss — Sysco (SYY) reported results that missed estimates, suggesting softening demand in the foodservice channel; any slowdown in away‑from‑home food volumes can weigh on POST’s foodservice‑oriented segments. Sysco Q3 Miss

- Negative Sentiment: Geopolitical risk is lifting energy prices — developments around the Iran war and UAE/OPEC exit increase oil/transport costs and overall market uncertainty; higher fuel and logistics costs squeeze CPG margins and can reduce discretionary food spending. That macro risk can depress POST’s stock along with peers. UAE Leaving OPEC

Analyst Ratings Changes

Several analysts recently weighed in on POST shares. BTIG Research started coverage on shares of Post in a report on Monday, April 13th. They issued a "neutral" rating for the company. Barclays dropped their target price on shares of Post from $127.00 to $119.00 and set an "overweight" rating for the company in a report on Tuesday, April 14th. Wells Fargo & Company dropped their price target on shares of Post from $120.00 to $110.00 and set an "equal weight" rating for the company in a research note on Wednesday, April 8th. Weiss Ratings upgraded shares of Post from a "sell (d+)" rating to a "hold (c-)" rating in a research note on Friday, February 6th. Finally, JPMorgan Chase & Co. dropped their price target on shares of Post from $133.00 to $119.00 and set an "overweight" rating for the company in a research note on Monday, April 20th. Five analysts have rated the stock with a Buy rating and four have issued a Hold rating to the stock. According to MarketBeat, Post presently has an average rating of "Moderate Buy" and a consensus target price of $124.50.

Check Out Our Latest Stock Report on POST

Insider Activity at Post

In other Post news, Director Gregory L. Curl sold 6,983 shares of the business's stock in a transaction on Monday, February 9th. The shares were sold at an average price of $114.31, for a total value of $798,226.73. Following the completion of the transaction, the director owned 21,293 shares in the company, valued at $2,434,002.83. The trade was a 24.70% decrease in their ownership of the stock. The transaction was disclosed in a legal filing with the SEC, which is available at the SEC website. 14.05% of the stock is currently owned by company insiders.

Hedge Funds Weigh In On Post

A number of institutional investors and hedge funds have recently modified their holdings of the company. Corient Private Wealth LLC grew its stake in shares of Post by 21.7% during the fourth quarter. Corient Private Wealth LLC now owns 27,803 shares of the company's stock worth $2,754,000 after purchasing an additional 4,963 shares in the last quarter. Mercer Global Advisors Inc. ADV grew its stake in shares of Post by 43.4% during the fourth quarter. Mercer Global Advisors Inc. ADV now owns 6,552 shares of the company's stock worth $649,000 after purchasing an additional 1,982 shares in the last quarter. Empowered Funds LLC grew its stake in shares of Post by 8.0% during the fourth quarter. Empowered Funds LLC now owns 17,493 shares of the company's stock worth $1,733,000 after purchasing an additional 1,303 shares in the last quarter. XTX Topco Ltd acquired a new position in shares of Post during the fourth quarter worth $3,219,000. Finally, SummitTX Capital L.P. acquired a new position in shares of Post during the fourth quarter worth $415,000. Institutional investors and hedge funds own 94.85% of the company's stock.

About Post

(

Get Free Report)

Post Holdings, Inc is a consumer packaged goods company that operates as a holding company for a diverse portfolio of food and beverage brands. The company's principal activities include the production, marketing and distribution of ready-to-eat cereal, refrigerated and frozen foods, and nutritional beverages. Through its operating segments—Post Consumer Brands, Foodservice, Refrigerated Side Dishes & Bakery, and Active Nutrition—Post Holdings delivers a broad array of products to retail grocers, convenience stores, foodservice operators and e-commerce channels.

The Post Consumer Brands segment features a variety of hot and cold cereals under names such as Honey Bunches of Oats, Shredded Wheat and Pebbles.

Further Reading

This instant news alert was generated by narrative science technology and financial data from MarketBeat in order to provide readers with the fastest reporting and unbiased coverage. Please send any questions or comments about this story to contact@marketbeat.com.

Before you consider Post, you'll want to hear this.

MarketBeat keeps track of Wall Street's top-rated and best performing research analysts and the stocks they recommend to their clients on a daily basis. MarketBeat has identified the five stocks that top analysts are quietly whispering to their clients to buy now before the broader market catches on... and Post wasn't on the list.

While Post currently has a Moderate Buy rating among analysts, top-rated analysts believe these five stocks are better buys.

View The Five Stocks Here

Wondering what the next stocks will be that hit it big, with solid fundamentals? Click the link to see which stocks MarketBeat analysts could become the next blockbuster growth stocks.

Get This Free Report

Like this article? Share it with a colleague.

Link copied to clipboard.