However, both accounts are subject to contribution limits that you must follow to avoid penalties. So what is the penalty for excess contributions to an IRA?

You guessed it — taxes!

Understanding IRA contribution limits

For 2024, the IRS has set the contribution limit for traditional and Roth IRAs at $7,000 per person. You can split this amount across both Roth and traditional accounts, but total contributions across all IRAs cannot exceed $7,000. If you're 50 or older, the annual contribution limit rises to $8,000 — the additional $1,000 is a "catch-up contribution."

All traditional and Roth IRAs are counted under the same contribution limit, meaning you can split the $7,000 across accounts in any manner you choose but the total contribution cannot exceed $7,000 in a single year.

(Note: SEP IRAs and SIMPLE IRAs have different contribution limits, but these are employer-sponsored plans designed for small businesses or self-employed persons.)

Unfortunately, no one guards the gates of IRAs, monitoring for excess contributions. You must keep track of your contributions across all your accounts yourself, which can cause headaches if you don't keep good records. Going over the limit will result in a penalty for overcontribution to IRA.

What are excess penalties to an IRA?

Traditional and Roth IRAs limit the amount participants can contribute each year. If you're older than 50, catch-up contributions are available, but you must stay within limits or get hit with an IRA excess contribution penalty. Participants can use both types of IRA to save for retirement, but the limit applies to all accounts in aggregate. So even if you opened three different IRAs at three various brokers, they would function as a combined entity for purposes of contribution limit rules.

What's the penalty on excess IRA contributions?

You'll pay 6% tax per year on the total excess contributions. For example, if you contribute $9,000 to your IRA, that extra $2,000 will be hit with a 6% tax each year that remains in the account. If you contribute $8,500 to your IRA, that extra $2,000 will be hit with a 6% tax each year that remains in the account.

How to know you’ve made excess contributions to an IRA

What's the best way to avoid the excess IRA contribution penalty? First, keep track of your contributions! Your IRA account provider will receive monthly statements about your assets, balances and contributions. If you have IRAs with multiple brokers, you'll need to add your total contributions, which can create headaches but is less problematic than the alternative.

Keeping track of your IRA contributions is essential because the IRS has an all-seeing eye and will know exactly how much you've put into each account. In addition, every broker must file IRS Form 5498 for every account holder with an IRA under their firm. So even if you don't report your IRA contributions, your broker will, and the IRS will access penalties based on this information. Keep good records of your contributions because the IRS will know precisely how much you've put in each account come tax time.

You don't need to go it alone when tracking your retirement savings and contributions, either! Even if you don't use an advisor, you can find many useful tools online for keeping records and plotting investment projections. MarketBeat's Retirement Calculator is one example where you can input personal data and market conditions to create contribution guidelines.

Impact of excess contributions on your IRA

Impact of excess contributions on your IRA

Excess contributions can have negative consequences on your retirement savings. Contributing too much to an IRA is an inefficient use of capital and has opportunity costs. For example, if you miscalculate your IRA contributions and put in too much, that capital doesn’t flow into a more efficient account like a 401(k) or standard brokerage account. You’ll need to remove the excess money from the account by the deadline and pay harsh taxes on any investment profits. And if you have a fixed or limited income, these types of mistakes can create major headaches.

Penalties for excess contributions

Here’s an example of how IRA contribution penalties can affect your retirement plans. Let’s say you’ve misinterpreted the rules and contributed $7,000 to a Roth IRA and then another $7,000 to a traditional IRA. You notice it after filing your taxes, so you’re forced to take the penalty. You’ll lose the tax deduction on the $7,000 in the traditional IRA, plus receive a 6% tax bill, which takes $420.

But you also purchased Microsoft Corp (NASDAQ: MSFT) shares and have gains of 10%. You’ll have to sell the shares to remove the excess contribution, which means the profit is taxed as income, hit with the 6% excess penalty AND hit with an additional 10% for early withdrawal. Sounds like a mess, doesn’t it? Had you bought $7,000 in a taxable brokerage account, you wouldn’t have been forced to sell or have paid capital gains rates on your investment profits (as long as you held the shares for a year).

How to correct excess contributions

If you discover your excess contributions before submitting your federal tax returns, you should avoid the penalty if you remove the excess in time. But it's not just the excess contributions you should account for. In addition, you must remove the excess contributions from your account.

Here's the kicker: If removed before the correction deadline (which is October 15), the excess contributions won't be taxed. But any profits on that contribution will be taxed as income and hit with the 10% early withdrawal penalty if you're under age 59.5. The IRS refers to this as "net income attributable (NIA)," and you'll likely need assistance from the bank or institution hosting your account to calculate it.

NIA works both ways. For example, suppose you make an excess contribution and invest in stocks that lose money. In that case, that loss will factor into the NIA calculation, and the amount you must remove will be less than the original excess contribution.

What to do if you discover excess contributions after taxes

After filing your tax returns, things get trickier if you discover an excess contribution. However, if you have time to file for an amendment before the extension deadline, you can avoid the 6% excise tax. Amended tax returns can be tedious and time-consuming, but the deadline for corrections is October 15, and avoiding the tax is usually worth the trouble.

You have options if you can't file an amended return in time. First, you can leave the funds in the account and use the excess as a carry-forward contribution. For example, if you have an excess contribution of $1,500, you can count that toward the following year's contribution and only pay the 6% tax this year. Just be sure to remember that you're starting the next year with $1,500 already contributed to the account.

The other option is to eat the tax and remove the excess contribution the following year. Remember, the excise tax gets levied annually, so you'll pay 6% on that amount (plus any gains) again the next year if you don't remove it before December 31.

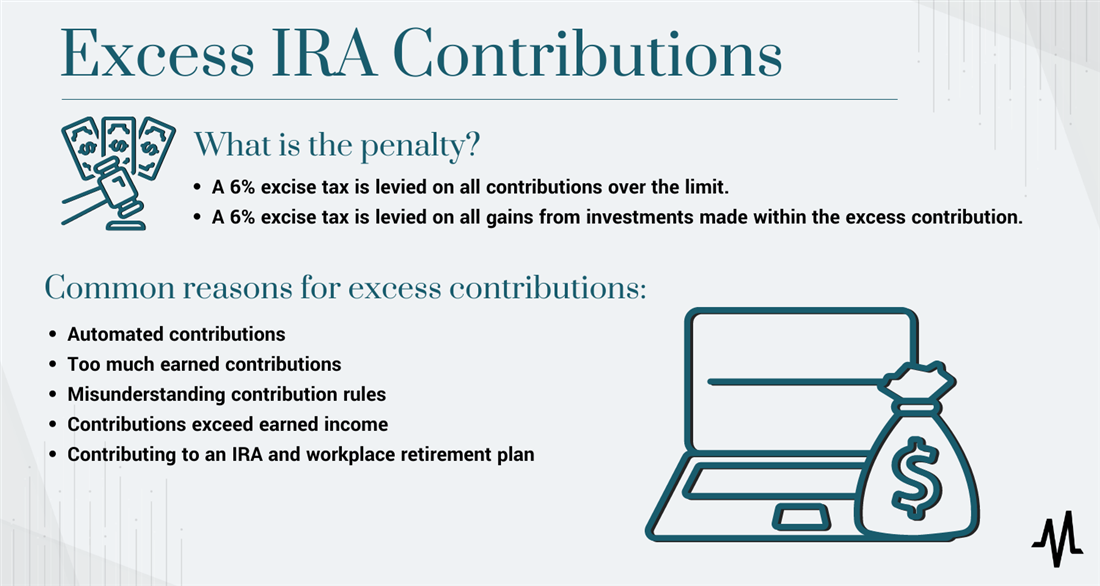

Common reasons for excess contributions

Excess contributions occur more frequently than you'd think, in all types of IRAs, from Roth IRAs to gold IRAs. Here are a few more common reasons investors find themselves with excessive funds in their IRAs.

Reason 1: Automated contributions

Automating finances is a great way to simplify things like paying bills, building an emergency fund, or calculating retirement savings. But this can occasionally backfire when it comes to vehicles like IRAs that have strict contribution limits.

For example, imagine you want to take advantage of a rebounding market and make all your IRA contributions in the first half of the year. You automate your deposit so that $500 goes in every two weeks. But then you have an extended summer vacation and forget to turn off the automatic deposits, resulting in $7,000 in total contributions. You're $500 over the limit and didn't realize it! If you want to automate your retirement savings, make sure you don't accidentally put yourself over the limit by neglecting to curtail your contributions when you reach the limit.

Reason 2: Too much earned income

IRAs aren't just subject to contribution limits — income limits also prevent high earners from contributing to Roth IRAs and getting tax-free investment growth. Roth IRA contributions begin to phase out when a single filer surpasses $146,000 in earned income ($230,000 for married couples) and get eliminated when income reaches $161,000 ($240,000 for married couples).

If you receive a steady paycheck every week, you know how your income will tally at the end of the year and can invest accordingly. But if your income fluctuates, you could find yourself in a situation where you've made Roth IRA contributions in a year where you made too much income to be eligible. High earners have a roundabout option for Roth IRAs through a backdoor Roth IRA conversion.

Reason 3: Misunderstanding contribution rules

The $7,000 annual contribution limit is an aggregate, meaning the balance of all IRA contributions cannot exceed the upper bound, even if you use multiple accounts. Unfortunately, this fact isn't always clear to retirement savers, and you can get in trouble if you aren't paying attention.

If you contribute $7,000 to a traditional IRA, that's the end of your contributions for the year. You can't contribute $7,000 to a traditional account and another $7,000 to a Roth. Now, if you do $3,500 in each account, that's fine!

The total contribution amount can be at most $7,000, regardless if you have one or 10 IRA accounts.

Reason 4: Contributions exceed earned income

Most people have an IRA contribution limit of $7,000 because they report more than $6,500 in annual income on their tax returns. But the actual contribution limit is $7,000 or the individual's MAGI for the filing year, whichever is smaller.

For example, if you only report $5,000 in income for 2024, your IRA contribution limit will be $5,000. Consider your IRA contributions if you expect very little taxable income in a particular year.

Reason 5: Contributing to an IRA and workplace retirement plan

If you have a traditional IRA, you can deduct contributions from your taxes if you meet all the prerequisites. High earners have deductions phase out at a certain level, but deductions also phase out if you (or your spouse) contribute to a workplace retirement plan like a 401(k) plan.

While contributing more than you can deduct from taxes won't trigger any overcontribution penalties, it may still create headaches at tax time if you find your contributions aren't tax-deductible and your modified adjusted gross income (MAGI) is higher than anticipated.

Summary of penalties

What is the penalty for excess contributions to an IRA? Here's a rundown:

- A 6% excise tax is levied on all contributions over the limit.

- A 6% excise tax is levied on all gains from investments made with the excess contribution.

Excess contribution taxes are administered annually, so you'll pay 6% each year on the extra funds in the account. You can remove the excess if you catch a mistake before the tax filing deadline and not be penalized. But excess funds withdrawn from a traditional IRA will be taxed as income, and any investment gains will be hit with the 10% early withdrawal penalty.

Tips for avoiding excess contributions

Here are a few practical tips for avoiding parking too much cash in your IRAs:

- Automate your contributions weekly, monthly or quarterly

- Contribute the full amount early

- Reevaluate your investment plans should your income change

- Monitor your retirement accounts and remove any excess contributions quickly

Follow certain guidelines to avoid penalties and taxes

Contributing too much to your IRA accounts can create many headaches at tax time. Excess contributions get an annual excise tax, and any gains on those particular contributions will be penalized with early withdrawal fees when removed.

The IRS will know precisely how much you contributed to your IRAs in aggregate since all brokers are required to report these statistics. So keep track of your contributions! IRAs can be significant savings vehicles to ward off inflation, but the penalties can erase many benefits if you aren't careful.

FAQs

Here are a few frequently asked questions about the penalties for contributing too much to your IRAs.

How much tax do I pay on excess IRA contributions?

The penalty for excess IRA contribution is a 6% excise tax each year the excess funds (and profits) remain in the account. If you contribute $8,000 and have a limit of $7,000, that extra $1,000 and any associated gains will be taxed at 6% annually until removed from the IRA.

How does the IRS find out about excess IRA contributions?

The IRS requires all brokers to fill out Form 5498 each year, which reports the contributions made by IRA account holders. The IRS will know exactly how much you've contributed through this form, so don't think you can overstuff your account and avoid consequences.

How much does it cost to max out an IRA?

For 2024, the IRA contribution limit is $7,000 for those under 50 and $8,000 for participants aged 50 or older. This limit is the maximum you can contribute across all your IRA accounts; you can't park $7,000 in your Roth and then another $7,000 in your traditional account.

Before you make your next trade, you'll want to hear this.

MarketBeat keeps track of Wall Street's top-rated and best performing research analysts and the stocks they recommend to their clients on a daily basis.

They believe these five stocks are the five best companies for investors to buy now...