Integrated circuit maker Jabil Circuit NYSE: JBL shares are still trading below its pre-COVID levels and underperforming the benchmark S&P 500 index NYSEARCA: SPY. The maker of integrated circuit products has been a pandemic beneficiary with the strong demand in electronic devices stemming from the stay-at-home trends. Consumer electronics demand should continue to surge with the acceleration of the restart narrative. Upside on the shares have been capped at the $35.75 double top since the market sell-off. The wider time frames are starting to generate steam for a breakout. Prudent investors should watch for both opportunistic pullback entries and breakout opportunities ahead of the holiday shopping season.

Q4 FY 2020 Earnings Release

On Sept. 24, 2020, Jabil released its fiscal fourth-quarter 2020 results for the quarter ending August 2020. The Company reported an earnings-per-share (EPS) profit of $0.98 excluding non-recurring items versus consensus analyst estimates for a profit of $0.67, beating estimates by $0.31. Revenues rose 11.1% year-over-year (YoY) to $7.3 billion beating analyst estimates of $6.28 billion.

Conference Call Takeaways

Jabil CFO, Mike Dastoor, noted there was fewer corporate disruptions than anticipated as supply chains were robust and efficient leading to lower corporate expenses. Jabil was quick to “capitalize on the upside demand, mainly in mobility, 5G wireless and cloud-end markets.” The Company was able to benefit from the compounding effects expense optimization and improve productivity from higher the expected sales. CEO Mark Mondello presented the diverse end product segments the Company provides product for. Healthcare, Mobil and Connected Devices divisions really shined this quarter.

Growth Industries

The restart acceleration should rebound the Automotive divisions as cars get back on the road. However, they are well positioned for the seismic growth in “electronification” of automobiles and has a “nearly 10-year relationship with the leading electric automotive company.” Sounds like he’s referring to Tesla, Inc. NASDAQ: TSLA. Margin expansion and cost efficiencies will drive growth. Jabil is also one of the largest healthcare manufacturing solutions companies in the world and continues to see synergistic growth with 5G mobile bringing more momentum to connected devices. These growth levers will offset first-half 2021 weakness in digital print and retail with pandemic triggered office and store closures. Industrial demand has remained “consistent to-date” but also is expected to weakened due to construction delays of new buildings.

Asset Light Model

The silver lining is the long-term growth Jabil expects when new building construction resumes with smart metering, power conversion and energy storage spaces. The Cloud space continues to grow with the hyper-scaling trend as client are hungry for cloud infrastructure and storage solutions driven by work-at-home demand. The Company is also converting nearly $1 billion in component procuring from the purchase and resale model to consignment in fiscal year 2021 which will boost expensive optimization leading to higher margins and less cash burn bolstering an improved asset-light operating model.

Raised Guidance

Jabil raised its fiscal Q1 2021 guidance for EPS in the range of $1.15 to $1.35 compared to consensus analyst estimates of $1.03. Q1 revenues are expected the range of $6.70 billion to $7.30 billion versus consensus estimates of $7.18 billion. The performance in the quarter can’t be understated and looks to improve with the acceleration of economic restarts. The FDA approval of a Covid-19 vaccine will only accelerate the recoveries in the soft industries making it a solid catalyst. This makes Jabil a go-to play when the approval eventually occurs. In the meantime, prudent investors can get a jump on the trigger by monitoring opportunistic pullback levels as it chops near the double top resistance.

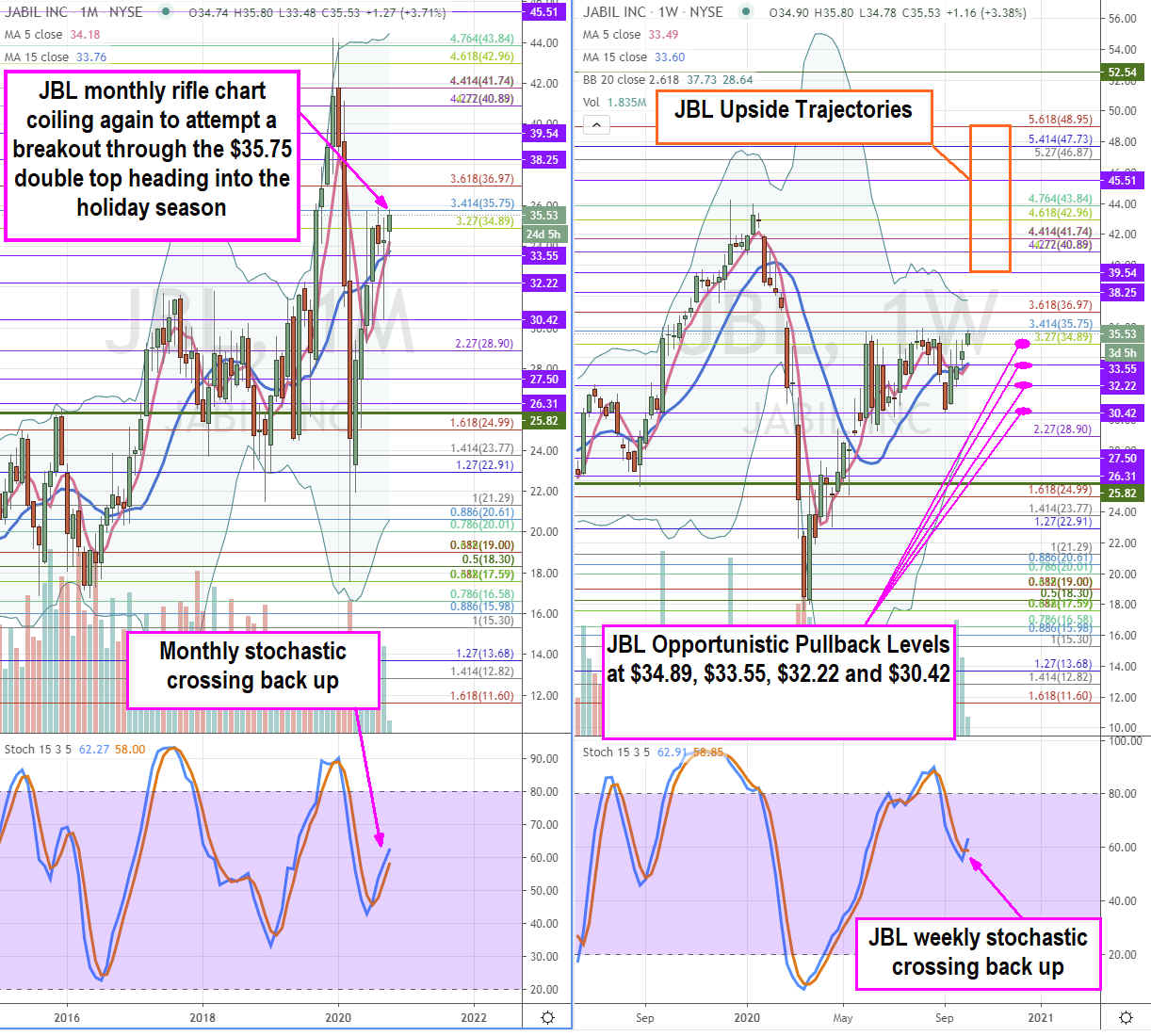

JBL Opportunistic Pullback Levels Using the rifle charts on the monthly and weekly time frames provides a broader view of the landscape for JBL stock. Shares have been chopping below the double top resistance area around the $35.75 Fibonacci (fib) level. The monthly rifle chart shows a rebounding stochastic crossed back up to resume upside momentum with the rising 5-period moving average (MA) support at $34.18. The weekly rifle chart triggered a market structure low (MSL) buy signal above $25.82. After rejecting twice off the double top, the weekly stochastic is again trying to cross back up take another stab at a breakout attempt. In the meantime, a rejection off that level can provide opportunistic pullback levels at the $34.89 fib, $33.55 fib, $32.22 fib and the $30.42 fib. The upside trajectories on a strong resistance breakout target the $39.54 to $48.95 longer-term fib. Traders can also watch peers Sanmina NASDAQ: SANM and Flextronics NASDAQ: FLEX price action as the tree tend to move together

Before you consider Jabil, you'll want to hear this.

MarketBeat keeps track of Wall Street's top-rated and best performing research analysts and the stocks they recommend to their clients on a daily basis. MarketBeat has identified the five stocks that top analysts are quietly whispering to their clients to buy now before the broader market catches on... and Jabil wasn't on the list.

While Jabil currently has a Moderate Buy rating among analysts, top-rated analysts believe these five stocks are better buys.

View The Five Stocks Here

Click the link to see MarketBeat's list of seven stocks and why their long-term outlooks are very promising.

Get This Free Report

Like this article? Share it with a colleague.

Link copied to clipboard.