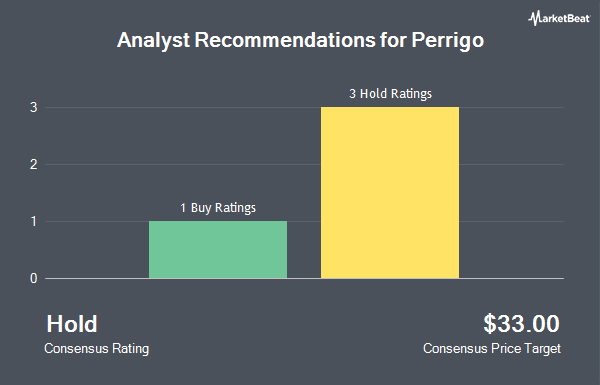

Perrigo Company plc (NYSE:PRGO - Get Free Report) has received a consensus recommendation of "Reduce" from the six ratings firms that are covering the stock, MarketBeat.com reports. Two equities research analysts have rated the stock with a sell recommendation, three have assigned a hold recommendation and one has issued a buy recommendation on the company. The average 12-month target price among brokerages that have covered the stock in the last year is $19.3333.

PRGO has been the subject of several recent analyst reports. Canaccord Genuity Group lowered their target price on shares of Perrigo from $20.00 to $17.00 and set a "buy" rating for the company in a research note on Friday, February 27th. Zacks Research downgraded shares of Perrigo from a "hold" rating to a "strong sell" rating in a research note on Friday, March 20th. Weiss Ratings reiterated a "sell (d+)" rating on shares of Perrigo in a research note on Monday, December 22nd. Argus upgraded shares of Perrigo to a "hold" rating in a research note on Wednesday, January 14th. Finally, Jefferies Financial Group reiterated a "hold" rating on shares of Perrigo in a research note on Thursday, February 26th.

View Our Latest Report on PRGO

Perrigo Price Performance

Shares of PRGO opened at $12.05 on Tuesday. The company has a market cap of $1.66 billion, a price-to-earnings ratio of -1.17, a price-to-earnings-growth ratio of 1.38 and a beta of 0.47. Perrigo has a twelve month low of $9.23 and a twelve month high of $28.43. The company has a quick ratio of 1.63, a current ratio of 2.76 and a debt-to-equity ratio of 1.23. The company has a 50 day moving average of $11.63 and a two-hundred day moving average of $14.36.

Perrigo (NYSE:PRGO - Get Free Report) last announced its earnings results on Thursday, February 26th. The company reported $0.77 earnings per share for the quarter, missing the consensus estimate of $0.80 by ($0.03). The firm had revenue of $1.11 billion during the quarter, compared to analyst estimates of $1.09 billion. Perrigo had a negative net margin of 33.51% and a positive return on equity of 9.41%. Perrigo's revenue was down 2.5% on a year-over-year basis. During the same quarter last year, the business earned $0.93 earnings per share. Perrigo has set its FY 2026 guidance at 2.250-2.550 EPS. As a group, analysts predict that Perrigo will post 2.13 earnings per share for the current fiscal year.

Perrigo Dividend Announcement

The business also recently disclosed a quarterly dividend, which was paid on Tuesday, March 24th. Stockholders of record on Monday, March 2nd were paid a dividend of $0.29 per share. This represents a $1.16 annualized dividend and a dividend yield of 9.6%. The ex-dividend date was Monday, March 2nd. Perrigo's payout ratio is presently -11.28%.

Institutional Investors Weigh In On Perrigo

Institutional investors and hedge funds have recently made changes to their positions in the stock. Bahl & Gaynor Inc. lifted its stake in shares of Perrigo by 5.4% during the third quarter. Bahl & Gaynor Inc. now owns 2,087,075 shares of the company's stock worth $46,479,000 after buying an additional 107,774 shares during the period. Cooke & Bieler LP lifted its stake in shares of Perrigo by 11.6% during the third quarter. Cooke & Bieler LP now owns 3,680,411 shares of the company's stock worth $81,963,000 after buying an additional 381,290 shares during the period. SG Americas Securities LLC lifted its position in Perrigo by 1,495.6% during the fourth quarter. SG Americas Securities LLC now owns 134,433 shares of the company's stock valued at $1,871,000 after purchasing an additional 126,008 shares during the period. Diamond Hill Capital Management Inc. lifted its position in Perrigo by 8.6% during the third quarter. Diamond Hill Capital Management Inc. now owns 1,797,746 shares of the company's stock valued at $40,036,000 after purchasing an additional 142,363 shares during the period. Finally, Nicola Wealth Management LTD. lifted its position in Perrigo by 38.4% during the third quarter. Nicola Wealth Management LTD. now owns 281,000 shares of the company's stock valued at $6,257,000 after purchasing an additional 78,000 shares during the period. 95.91% of the stock is currently owned by institutional investors and hedge funds.

About Perrigo

(

Get Free Report)

Perrigo Company plc is a global healthcare supplier specializing in over-the-counter (OTC) and self-care products, as well as generic prescription pharmaceuticals and active pharmaceutical ingredients. The company develops, manufactures and distributes a broad array of consumer health products, including analgesics, vitamins and supplements, digestive health remedies, topical treatments, and infant formulas. Perrigo's focus on private-label solutions has made it a leading partner for retailers and pharmacy chains seeking high-quality, value-oriented alternatives to branded medications and health supplements.

Organized across three principal business segments—Consumer Healthcare, Prescription Pharmaceuticals and Active Pharmaceutical Ingredients—Perrigo's operations span research and development, manufacturing, quality assurance and global distribution.

Further Reading

This instant news alert was generated by narrative science technology and financial data from MarketBeat in order to provide readers with the fastest reporting and unbiased coverage. Please send any questions or comments about this story to contact@marketbeat.com.

Before you consider Perrigo, you'll want to hear this.

MarketBeat keeps track of Wall Street's top-rated and best performing research analysts and the stocks they recommend to their clients on a daily basis. MarketBeat has identified the five stocks that top analysts are quietly whispering to their clients to buy now before the broader market catches on... and Perrigo wasn't on the list.

While Perrigo currently has a Hold rating among analysts, top-rated analysts believe these five stocks are better buys.

View The Five Stocks Here

Market downturns give many investors pause, and for good reason. Wondering how to offset this risk? Click the link to learn more about using beta to protect your portfolio.

Get This Free Report

Like this article? Share it with a colleague.

Link copied to clipboard.