High-yield stocks are attractive for easy-to-understand reasons. When they outpace the S&P 500’s average yield and inflation, they can provide substantial income. But they can also become a double-edged sword for investors. High yields can be, and often are, red flags that point to fundamental changes that have yet to be reflected in dividend payment metrics. Investors' due diligence includes determining what drives the high yield and what the rest of the market thinks of the investment. Fundamentals can be bullish, but the stock price is unlikely to perform as expected if the market isn’t buying it. In this case, high yields are compounded by bullish market sentiment and reasons for investors to buy in.

Energy Transfer: Transferring Energy Volume Into Investor Returns

Energy Transfer Today

ET

Energy Transfer

$18.86 -0.05 (-0.24%) As of 03:59 PM Eastern

This is a fair market value price provided by Massive. Learn more. - 52-Week Range

- $16.18

▼

$20.70 - Dividend Yield

- 7.16%

- P/E Ratio

- 15.72

- Price Target

- $23.45

is a master limited partnership (MLP) operating as a midstream energy company. Both factors are important to this investment, as the MLP structure enables tax-advantaged operations and a high dividend yield, while midstream operators are well-positioned in 2026. Their business is underpinned by volume; growth pillars include natural gas, and macroeconomic conditions favor North American operators.

Energy Transfer’s dividend yield is over 7% as of mid-June. The 7% yield appears unsafe at first glance due to the high payout ratio, but that metric is misleading. GAAP earnings are significantly affected by depreciation, a non-cash charge. The more pertinent factors are cash flow and free cash flow, which enable robust coverage. Running at approximately 1.8x the dividend, free cash flow also enables reinvestment to keep the pipelines running and the network expanding.

Analysts' trends are robust for Energy Transfer. MarketBeat’s data reflect improving coverage, strengthening sentiment, and an uptrend in price targets. The consensus target implies about 20% upside for the Buy-rated stock, while the high-end target points to additional upside beyond that. Either level would put ET near a fresh long-term high.

JBS N.V.: Margin Pressures Create High-Yield Opportunity

JBS Today

$12.32 +0.14 (+1.11%) As of 03:59 PM Eastern

This is a fair market value price provided by Massive. Learn more. - 52-Week Range

- $11.49

▼

$18.65 - Dividend Yield

- 8.11%

- P/E Ratio

- 7.75

- Price Target

- $19.00

faces headwinds in 2026, but they are offset by a well-diversified business with revenue streams in processed meat and animal by-products. The primary headwind is the U.S. cattle market, which affects the price spread between the cattle they receive and the products they sell. The takeaway for investors is that FQ1’s negative cash burn is seasonally impacted and also affected by one-offs, including accelerated investment. The critical detail is that

dividend coverage is reliable in 2026, supported by healthy annualized cash flow and balance sheet.

Analyst trends are bullish for JBS stock, albeit to a lesser degree than ET. Most analysts tracked by MarketBeat are bullish on JBS, giving the stock a consensus Moderate Buy rating with about 50% implied upside. Their sentiment is reflected in institutional activity, which is accumulating shares at approximately a $10-to-$1 pace.

Diversified Energy: Don’t Buy It for Growth

Diversified Energy Today

DEC

Diversified Energy

$13.26 +0.10 (+0.74%) As of 03:59 PM Eastern

This is a fair market value price provided by Massive. Learn more. - 52-Week Range

- $12.33

▼

$18.90 - Dividend Yield

- 8.75%

- P/E Ratio

- 3.77

- Price Target

- $21.83

is a U.S.-focused upstream energy operator, but it is not a traditional exploration company. Instead, it targets existing wells with predictable volumes that it can optimize over time. By focusing on mature wells and operating efficiency, the company aims to generate relatively stable cash flow to support dividends.

The dividend yields approximately 8.8% and is sustainable. The payout ratio relative to earnings suggests reliability, but, again, as with Energy Transfer, free cash flow is what matters. It provides a much lower payout ratio, enabling aggressive buybacks alongside the distribution. Analyst sentiment is bullish, with DEC carrying a consensus Buy rating and an average price target that implies about 66% upside.

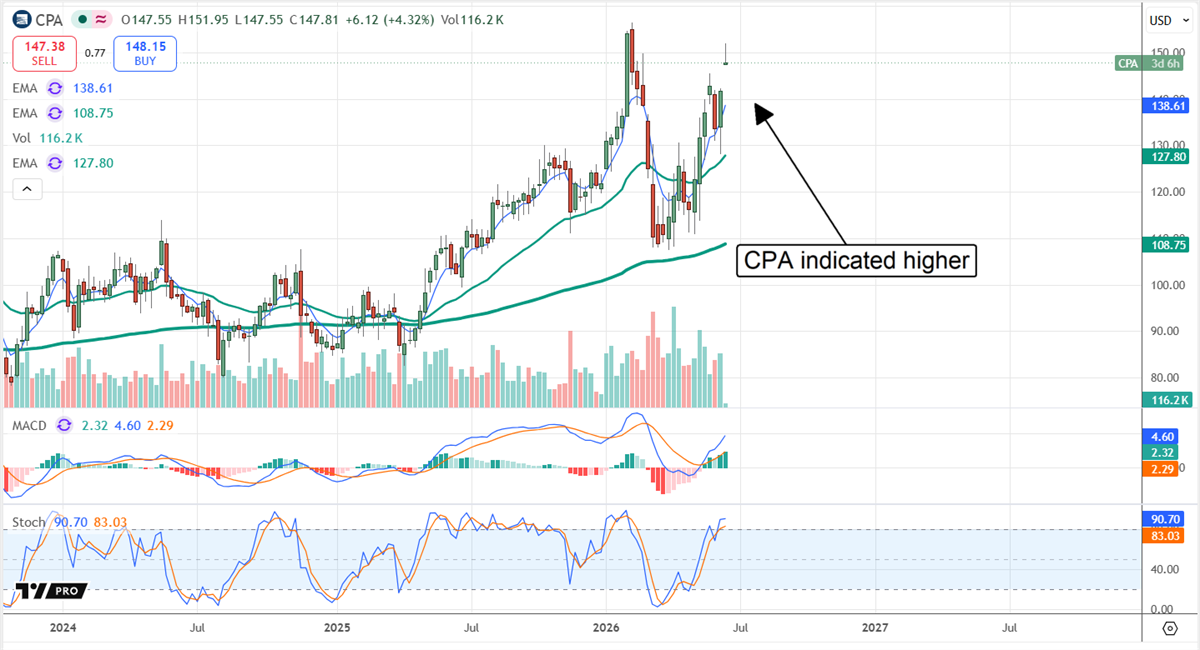

Copa Holdings Flies High in 2026 on Growth and Yield

Copa Today

$143.25 -1.15 (-0.80%) As of 03:59 PM Eastern

This is a fair market value price provided by Massive. Learn more. - 52-Week Range

- $99.32

▼

$156.41 - Dividend Yield

- 4.77%

- P/E Ratio

- 8.35

- Price Target

- $167.30

is not a newcomer to

high-yield watchlists. This Latin American-headquartered airline has been growing at an industry-leading pace for years, driven by industrialization and an expanding middle class. Results in 2026 include double-digit demand, double-digit capacity growth, double-digit revenue growth, and

a healthy dividend payment. 2026’s stock price increase has reduced the yield to about 4.8%, which remains high relative to peers and the broad market, and is reliable. The payout ratio is nearly 40% and is compounded by a solid balance sheet and growth outlook.

Analyst sentiment toward Copa remains bullish, with 12 analysts rating the stock a consensus Buy. Coverage and price targets have increased over the trailing 12 months, and the average target implies about 10% upside as of mid-June. That would be enough for a fresh all-time high, while the high-end target leaves room for another double-digit gain.

Smithfield Foods: Undervalued and High-Yielding

Smithfield Foods Today

SFD

Smithfield Foods

$25.95 +0.02 (+0.08%) As of 04:00 PM Eastern

- 52-Week Range

- $21.08

▼

$29.81 - Dividend Yield

- 4.82%

- P/E Ratio

- 10.14

- Price Target

- $29.88

is another play on U.S. meat processing, specifically pork. The company is supported by robust demand, aided by tight beef markets and their high prices, with long-term forecasts focusing on expansion plans. The

company is expanding and modernizing, which presents near-term capital headwinds and long-term opportunities. As it stands, the

dividend helps to offset near-term risks, yielding approximately 4.8% at approximately 49% of earnings, while the valuation offsets more. Trading at only 10x earnings, the stock is cheap compared to Hormel’s 16x, and you get a comparable yield.

SFD stock has a consensus rating of Moderate Buy. Analysts see Smithfield rising to an average price target of $30, which would mark a fresh high if reached. Recent revisions suggest the upper end of the range could move higher if the company continues to execute. Catalysts include resilient demand, prepared foods momentum, and progress on Smithfield’s expansion and modernization strategy.

Before you consider Energy Transfer, you'll want to hear this.

MarketBeat keeps track of Wall Street's top-rated and best performing research analysts and the stocks they recommend to their clients on a daily basis. MarketBeat has identified the five stocks that top analysts are quietly whispering to their clients to buy now before the broader market catches on... and Energy Transfer wasn't on the list.

While Energy Transfer currently has a Buy rating among analysts, top-rated analysts believe these five stocks are better buys.

View The Five Stocks Here

Looking to profit from the electric vehicle mega-trend? Click the link to see our list of which EV stocks show the most long-term potential.

Get This Free Report