For those who commute to work, driving by the first gas station of the day may now be a constant source of anxiety. The national average has quickly surged past $4.50 per gallon, a shock to consumers who had been paying less than $3 per gallon as recently as January. With no end to the Iran war in sight, $5-per-gallon gas seems inevitable, and U.S. consumers will be forced to make difficult travel choices this summer.

Investors also have to make some decisions; if gas prices continue to rise, which stocks are best prepared to benefit?

Hint: it requires a strategy more complex than just a portfolio of large-cap energy stocks.

The energy industry has been one of the best-performing market sectors in 2026, trailing only tech following the explosive semiconductor rally. But not every energy company benefits from high gasoline prices. Investors will want to diversify their holdings across different areas of the sector that have outsized exposure to gas prices.

Three types of companies span businesses that capture this edge: West Coast refiners, Permian shale producers, and shipping tanker operators.

Par Pacific Holdings: Small-Cap Refiner Benefitting From Widening Crack Spreads

Par Pacific Today

$55.46 -2.17 (-3.77%) As of 03:59 PM Eastern

This is a fair market value price provided by Massive. Learn more. - 52-Week Range

- $22.82

▼

$70.39 - P/E Ratio

- 6.19

- Price Target

- $70.00

The Pacific Coast has the highest retail gasoline prices in the United States, so that’s a great place to look for refiners that benefit from wide crack spreads. California gas prices have already breached $6 per gallon, and the region was already undersupplied before the war broke out.

One of these beneficiaries is Par Pacific Holdings Inc. NYSE: PARR, a small-cap refiner that operates several facilities across the Pacific Northwest and Hawaii.

Despite a market cap of just over $3 billion, Par Pacific generated more than $7 billion in sales in 2025, and soaring crack spreads have it in position for another strong year.

Despite a $125 million price lag headwind from Hawaiian operations, Par Pacific still reported $1.82 billion in Q1 2026 revenue in its May 5 earnings release, including $91 million in adjusted EBITDA.

Earnings per share (EPS) of 78 cents missed the $1 expectation, but the Hawaiian Renewables venture had a successful launch, and crack spreads are expected to provide tailwinds through the summer. And despite a 40% gain in the last three months, PARR shares still trade at just 4.4x forward earnings and 0.41x sales.

PARR shares could offer a quality entry point for new investors right now as the price bounces off the 50-day moving average. The 50-day and 200-day MAs remain supportive of the uptrend, and the selling momentum displayed by the Relative Strength Index (RSI) appears to be slowing. If the RSI continues to reverse course, new all-time highs are likely on the horizon.

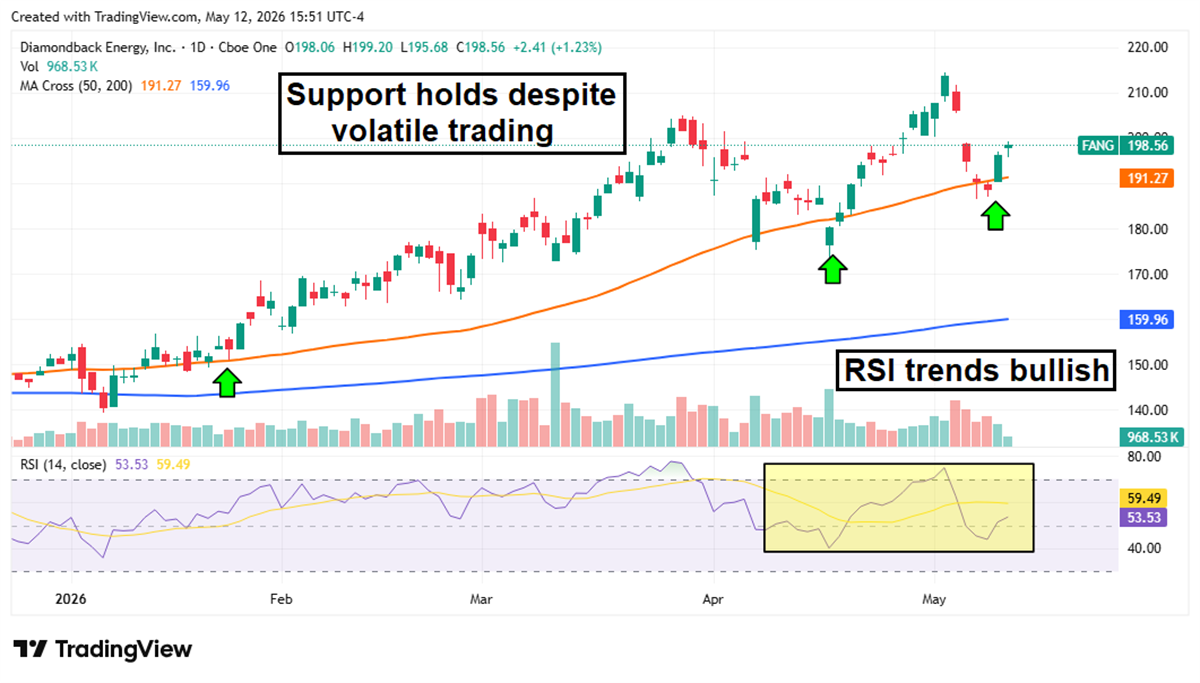

Diamondback Energy: Premium Cash Flow Generation With Oil Over $90

Diamondback Energy Today

FANG

Diamondback Energy

$191.59 -4.96 (-2.52%) As of 04:00 PM Eastern

- 52-Week Range

- $134.30

▼

$214.51 - Dividend Yield

- 2.30%

- P/E Ratio

- 222.78

- Price Target

- $223.63

Diamondback Energy Inc. NASDAQ: FANG is one of the largest drillers in the Permian Basin, extracting crude oil, natural gas, and natural gas liquids (NGLs) from wells in Texas and New Mexico.

Diamondback is a direct beneficiary of higher crude prices; in Q4 2025, management projected that the company could generate more than $5.5 billion in free cash flow if oil prices reached $70 per barrel.

Now that WTI crude prices have eclipsed $90, Diamondback is positioned to outperform even its most optimistic cash flow projections.

In its Q1 2026 earnings report, the company beat top and bottom-line expectations, upped its dividend, and raised full-year oil production guidance. It also plans to put two or three new rigs into production, and the extra cash will help the company pay down debt and increase future dividends and share buybacks.

FANG shares have been volatile over the last few months, but the stock is still up more than 30% year-to-date (YTD). Support at the 50-day MA has held whenever the rally shows signs of pulling back, and shares are once again bouncing off this level as the RSI moves back into bullish territory.

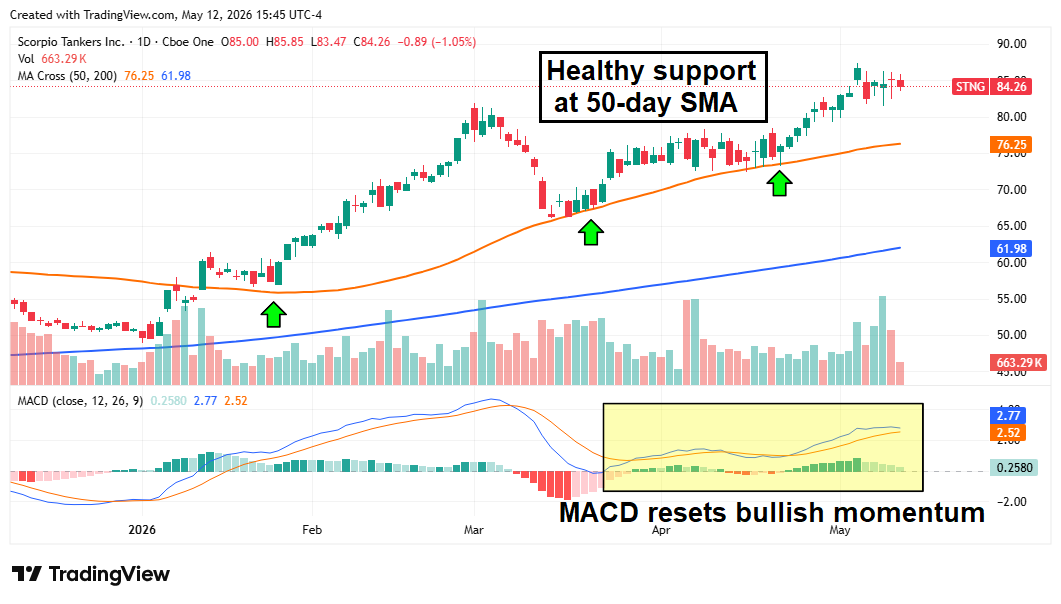

Scorpio Tankers: Hormuz Closure Causes Volatile Shipping Rate Increases

Scorpio Tankers Today

$76.28 -0.18 (-0.24%) As of 03:59 PM Eastern

This is a fair market value price provided by Massive. Learn more. - 52-Week Range

- $38.83

▼

$87.39 - Dividend Yield

- 2.36%

- P/E Ratio

- 7.50

- Price Target

- $93.50

The thesis behind Scorpio Tankers Inc. NYSE: STNG is fairly straightforward: if companies are forced to reroute away from the Strait of Hormuz, shipping day rates will surge as product is sourced from farther afield.

Supply dislocations often create outsized earnings opportunities for shippers, as oil and gas companies have no choice but to pay astronomical rates, which then trickle directly into earnings.

Investors are already seeing this scenario play out at Scorpio. The company reported Q1 2026 revenue of over $312 million in its May 6 earnings release, up more than 46% year-over-year (YOY).

Scorpio only generated $938 million in total 2025 sales, so revenue is already well ahead of last year’s performance, and the supply disruption is likely to last throughout the year.

A resumption of normal Hormuz traffic would be a headwind to STNG shares as shipping rates would quickly normalize. But until that catalyst occurs, the stock will likely remain in the uptrend that’s boosted it more than 60% YTD.

Support remains strong at the 50-day MA, and the Moving Average Convergence Divergence (MACD) indicator shows that bullish momentum is once again simmering.

Before you consider Diamondback Energy, you'll want to hear this.

MarketBeat keeps track of Wall Street's top-rated and best performing research analysts and the stocks they recommend to their clients on a daily basis. MarketBeat has identified the five stocks that top analysts are quietly whispering to their clients to buy now before the broader market catches on... and Diamondback Energy wasn't on the list.

While Diamondback Energy currently has a Moderate Buy rating among analysts, top-rated analysts believe these five stocks are better buys.

View The Five Stocks Here

The AI boom is creating opportunities across semiconductors, cloud computing, enterprise software, infrastructure, cybersecurity, and automation.

Inside this report, you’ll find 10 companies positioned to benefit as artificial intelligence moves from hype to real-world deployment and becomes a core growth driver for corporate America.

Get This Free Report